Industry Trends

From gallium to germanium: understanding china’s critical minerals export playbook

From Gallium to Germanium: How a Niche Metals Move Became a Systemic Signal

The 2023 export controls on gallium and germanium marked a turning point in how critical minerals intersect with geopolitics, technology, and industrial planning. What initially looked like a narrow response to semiconductor restrictions has evolved into a recognizable template: identify where Chinese refining or processing is systemically irreplaceable, then convert that technical dominance into regulatory leverage.

This playbook, captured in the phrase “from gallium to germanium: understanding China’s critical minerals export playbook”, is not about raw ore in the ground. It is about midstream processing, purity thresholds, and the often-overlooked by-product streams of base-metal mining where a handful of refineries and separation plants determine whether downstream factories can run at all. For operators in semiconductors, permanent magnets, EV batteries, high-performance alloys, and defense systems, the operational question is no longer just price and volume; it is time-to-disruption under an export-license shock.

China’s approach is structurally different from traditional commodity leverage. Rather than cutting off headline metals like copper or iron ore, Beijing focuses on materials where refining is highly concentrated, technically demanding, and tightly linked to end-use performance: gallium and germanium for compound semiconductors and optics, specific rare earths for magnets, graphite for anodes, and tungsten for cutting tools and armor-piercing applications. This differentiation matters, because it determines which countermeasures are realistic within industrial timescales and which are not.

The result is a new layer of systemic risk in critical-minerals supply chains. It does not manifest as immediate volume shortages alone; it emerges as licensing delays, product‑classification ambiguity, compliance uncertainty, and sudden shifts in where value capture concentrates along the chain. For jurisdictions seeking to secure semiconductor, defense, and clean‑energy capacity, understanding the technical architecture of this playbook has become part of basic industrial resilience planning.

Gallium and Germanium: From By-Products to Geopolitical Switches

Technical and Supply Profiles of Two “Small” Metals

Gallium and germanium sit in the category of “small-volume, high-leverage” metals. Global tonnages are modest compared with copper or nickel, but technical dependence is acute in specific applications. Their supply chains share a critical structural feature: both are predominantly recovered as by-products.

Gallium is mainly obtained from bauxite processing liquor in the Bayer process and, to a lesser extent, from zinc processing. The concentration of gallium in bauxite ore is low, and extraction is technically and energetically non-trivial. Recovery requires selective precipitation or solvent-extraction circuits integrated into alumina refineries, followed by further refining to high-purity gallium metal suitable for electronics. Industry and government data prior to 2024 typically estimated that China accounted for the overwhelming majority of refined gallium output, with a large share of the world’s Bayer-process refineries configured to capture gallium only within Chinese jurisdiction.

Germanium is equally dependent on host metals. It is generally recovered from zinc smelter flue dusts and, in some cases, from coal fly ash or copper residues. The refining route involves leaching, solvent extraction or ion exchange, and distillation or zone refining to reach the high purities required for optical fibers, infrared optics, and high-efficiency solar cells. Again, pre‑2024 USGS and European data pointed to Chinese refiners as controlling most of the world’s germanium production capacity, particularly for the highest purity grades.

This by-product status is not a minor detail. It structurally ties gallium and germanium availability to the economics of alumina, zinc, and other primary metals. New primary mining projects for these elements are rare. Any attempt to diversify away from Chinese supply quickly runs into the reality that alternative refineries either lack by-product recovery circuits, lack the requisite high-purity refining technology, or face ESG and permitting headwinds that extend timelines far beyond a typical export-control shock cycle.

The 2023 Export Controls: Architecture and Intent

In mid‑2023, China’s Ministry of Commerce (MOFCOM) and the General Administration of Customs introduced licensing requirements for a defined set of gallium- and germanium-related products. These measures covered specific chemical compounds, metals, and in some cases alloys and wafers above certain purity thresholds. Exporters were required to obtain case-by-case approvals, with declared end users and end uses, under a national security and dual-use framing.

Several technical aspects of the controls matter more than the headlines:

- Purity-based triggers: Control lists were defined with minimum purity levels or specific product forms, targeting semiconductor- and optics-grade materials rather than bulk low-value streams. This mirrored how advanced lithography tools or AI chips are controlled by function and performance, not just product labels.

- Integration with dual-use narratives: The measures framed gallium nitride (GaN) and germanium-based technologies as dual-use, emphasizing their roles in radar, satellite, and secure communications alongside civilian 5G and data-center hardware.

- Licensing discretion: No explicit quantitative quotas were announced. Instead, approvals could be accelerated, delayed, or withheld, providing MOFCOM with granular control over who received material, when, and at what paperwork cost.

From an operational perspective, the novelty was not that exports of a strategic material were controlled. The shift was that controls were applied to metals whose extraction and high-purity refining are dominated by a single jurisdiction, and whose immediate substitution is technically and industrially constrained. In other words, the fulcrum of leverage was midstream process dominance, not raw geological abundance.

For compound semiconductor fabs working with GaN and gallium arsenide (GaAs), the impact was not just headline scarcity. The more acute risk lay in batch-to-batch variability and qualification delays when switching suppliers. Epitaxial wafer lines are extremely sensitive to impurity profiles, trace metallics, and defect densities. Each new feedstock source requires rigorous qualification cycles, adding lead time and yield risk even when nominally equivalent gallium is available.

Germanium-dependent segments experienced a similar pattern. Infrared optics producers, fiber-optic preform manufacturers, and space-cell fabricators faced increased exposure to shipment delays or licensing uncertainty in critical high-purity grades, where Chinese refineries had been the default global suppliers. The lesson across both metals was straightforward: taking by-product materials for granted had created silent chokepoints that only became visible when licensing gates closed.

From Niche Metals to a Broader Critical-Minerals Playbook

Gallium and germanium controls did not emerge in isolation. They fit into a longer arc of Chinese critical-minerals policy that includes rare earths, graphite, tungsten, and other strategic metals. The pattern combines three elements: dominant midstream capacity, flexible use of export licensing, and a dual-use narrative that links materials to security-sensitive applications.

Rare Earths and Permanent Magnets: The Original Template

The rare earth episode with Japan in 2010 remains the canonical early use of minerals as a coercive instrument. Following a maritime incident near disputed islands, Japanese firms reported sudden disruptions and delays in rare earth oxide and metal shipments from Chinese ports. Although volumes recovered and China subsequently removed formal export quotas after World Trade Organization challenges, the episode exposed a deeper structural reality: while rare earth deposits exist globally, the bottleneck lies in separation, refining, and magnet manufacturing capacity.

China’s position is strongest in the midstream: solvent-extraction plants that separate light and heavy rare earth elements (LREEs and HREEs), metal and alloy production lines, and sintered or bonded magnet fabrication. The technical heart of this dominance is an industrial base of solvent-extraction circuits with hundreds to thousands of mixer-settler stages, tuned over decades to produce specific REE oxides and alloys at scale. The capital, environmental, and know-how barriers to replicating these plants are orders of magnitude higher than simply opening a new mine.

Permanent magnets, especially NdFeB magnets doped with dysprosium (Dy) and terbium (Tb) for high-temperature performance, illustrate how control over specific rare earths translates into leverage over entire downstream sectors. Modern EV traction motors, direct-drive wind turbines, precision actuators, and many defense systems rely on these magnets for size, efficiency, and reliability. Alternative motor designs exist, but switching architectures at scale is slow and expensive from an engineering, tooling, and qualification standpoint.

From a playbook perspective, rare earths demonstrated a principle that gallium and germanium later reaffirmed: “The strongest lever is rarely ore in the ground; it is the least replicable processing node that all high-performance applications quietly pass through.”

Graphite, Tungsten, and Other Strategic Metals

Controls on graphite exports, announced in 2023, extended this logic into the lithium-ion battery value chain. China dominates production of anode-grade graphite, both natural and synthetic. The transformation from mined graphite or petroleum coke into spherical, coated, battery-ready anode material requires high-temperature furnaces, graphitization reactors, stringent particle-size control, and carbon-coating processes. Environmental controls, energy intensity, and capex profiles for these assets have concentrated capacity in a limited number of industrial clusters, heavily in China.

Tungsten sits at another critical junction. Known for its extremely high melting point and hardness, tungsten is essential for cemented carbide cutting tools, armor-piercing munitions, and certain high-performance alloys. While tungsten ore deposits are geographically more diverse than gallium or germanium by-product streams, Chinese mines and processing plants still account for a large share of global supply. Powder metallurgy routes for tungsten carbide tools and advanced alloys involve specific sintering temperatures, cobalt binder chemistries, and grain-size control-areas where established producers retain tacit process knowledge that newcomers take time to match.

These examples show that China’s critical-minerals approach is not a single-commodity story. It is a portfolio of chokepoints: gallium and germanium in compound semiconductors and optics; rare earths in magnets; graphite in anodes; tungsten in tooling and munitions; and, potentially, other by-product or specialty metals such as indium, bismuth, and tellurium that intersect with photovoltaics, solder alloys, and display technologies.

In each case, the technical driver of leverage is the same: concentration of midstream processing steps that are capital intensive, environmentally sensitive, knowledge-intensive, and relatively invisible in public debates compared with headline mining projects.

Implementation Mechanics: How the Export Playbook Actually Operates

Licensing, Control Lists, and Dual-Use Classification

At a regulatory level, China’s export playbook for critical minerals runs primarily through MOFCOM licensing. The mechanism is straightforward in legal form but powerful in practice: selected items are added to a control list, and any export of those items requires a government-issued license. Approval decisions can factor in end user, end use, destination country, and broader diplomatic context.

The technical sophistication lies in how those control lists are defined. For gallium and germanium, thresholds tied to purity, chemical form, or product geometry (e.g., wafers) delineated which shipments triggered controls. For graphite, differentiation between battery-grade materials and non-battery industrial grades allowed regulators to focus on lithium-ion supply chains while minimizing broader industrial disruption. For rare earths, earlier quota regimes distinguished between oxides, metals, and manufactured magnets.

Dual-use framing provides the legal and political justification. By emphasizing that these materials support both civilian and military applications, Beijing aligns its export-control narrative with that of the United States, European Union, and other jurisdictions that restrict advanced chips, lithography, or satellite components. This mirroring is not cosmetic. It allows Chinese authorities to argue that controls are defensive and reciprocal rather than aggressive, even as they are applied to upstream raw materials where foreign firms have few short-term alternatives.

From a compliance perspective, the practical bottlenecks are:

- Classification uncertainty: Determining whether a specific product-such as a gallium alloy, a graphite intermediate, or a rare-earth-containing component-falls within control-list definitions can be non-trivial, especially when combined with HS code variations across jurisdictions.

- End-use scrutiny: Documentation of end users and applications introduces confidentiality and competitive sensitivities, particularly for defense-adjacent or proprietary technologies.

- Lead-time variability: Licensing approval times can vary widely, creating planning risk for just-in-time manufacturing systems that rely on steady feedstock flows.

Interaction with Western Export Controls and Compliance Overlap

China’s minerals export controls do not operate in a vacuum. They interact with, and sometimes directly respond to, Western controls on semiconductor tools, advanced chips, and other sensitive technologies. The result for industrial operators is a complex overlay: U.S. and allied jurisdictions control outbound flows of high-end equipment and know-how to China, while China controls outbound flows of critical materials to those same jurisdictions.

This dual-control environment creates several operational pinch points:

- Mirror compliance obligations: A company may need to comply simultaneously with U.S. Export Administration Regulations (EAR) when shipping equipment or software to China and with MOFCOM licensing when sourcing gallium or graphite from China for other facilities.

- Data asymmetry: Western firms typically have deeper experience with U.S. and EU compliance regimes than with Chinese export-control application processes, making MOFCOM licensing more opaque.

- Traceability requirements: As Chinese controls evolve, traceability of origin and processing histories for critical materials becomes increasingly salient, mirroring requirements already familiar from conflict-minerals or ESG reporting frameworks.

For critical-minerals flows, this means that the practical risk profile is defined less by a single, headline “ban” and more by the intersection of multiple licensing gates, each capable of delaying or reshaping material flows with relatively little public visibility.

Operational Impact Across Key Value Chains

Semiconductors and Power Electronics

Gallium and germanium controls directly intersect with advanced semiconductor and power-electronics supply chains. Gallium nitride (GaN) and gallium arsenide (GaAs) devices are central to RF front-ends, radar modules, satellite communications, data-center power management, and increasingly automotive powertrains and fast-charging systems. Germanium has applications in high-speed SiGe chips, fiber-optic systems, and multi-junction solar cells.

Technically, the key exposure is not just raw gallium metal or crude germanium oxide. It is the availability of:

- High-purity precursors: 6N+ (99.9999% and above) gallium and germanium for semiconductor-grade ingots and epitaxial wafers.

- Specialty compounds: Trimethylgallium (TMGa), triethylgallium (TEGa), and germane (GeH4) used in metal-organic chemical vapor deposition (MOCVD) and other epitaxy processes.

- Wafer substrates: Processed GaAs, InGaAs, or Ge wafers that require tight defect and impurity control.

Export controls that touch any of these nodes can propagate rapidly through fab operations. Even where alternative suppliers exist outside China, qualification cycles are lengthy. MOCVD reactors, for example, are highly sensitive to precursor purity and impurity profiles; switching from one supplier’s TMGa to another’s is not a plug-and-play change, but a process-requalification project that can span months and entail yield penalties.

For industrial resilience, the central insight is that compound semiconductor ecosystems are more brittle than bulk silicon lines with diversified precursor bases. “A few tonnes of high-purity gallium, if constrained at the wrong point in the chain, can destabilize far more downstream capacity than many times that volume of a base metal.”

EVs, Renewables, and Defense: The Magnet and Graphite Nexus

Beyond semiconductors, China’s critical-minerals leverage is most visible in the convergence of EV motors, wind turbines, industrial drives, and defense systems around rare-earth permanent magnets and graphite anodes.

On the magnet side, the exposure stack looks like this:

- Upstream: Mines and concentrates in China, the United States, Australia, and elsewhere provide mixed rare earths.

- Midstream separation: Chinese plants still dominate solvent extraction and oxide production, particularly for heavy rare earths such as dysprosium and terbium.

- Metal and alloying: Magnet-grade alloys require specific compositions and low impurity levels, with much of the capacity located in China and a smaller but growing base in Japan, Europe, and North America.

- Magnet fabrication: Powder production, pressing, sintering, and machining of NdFeB magnets are heavily concentrated in East Asia, with established Chinese producers holding significant market share.

Export restrictions at the oxide or metal stage can force magnet producers outside China to slow or halt production, while leaving Chinese magnet exports comparatively less constrained. The structural effect is a re-centralization of value-added magnet manufacturing within Chinese territory, even as raw rare-earth mining diversifies geographically.

On the graphite side, the link to EV and grid-storage batteries is direct. Anode materials typically account for a substantial share of cell mass, and high-performance graphite anodes, whether natural or synthetic, still dominate commercial lithium-ion chemistries. Restrictions on battery-grade graphite exports interact with growing global demand in a way that reinforces China’s strategic position: even if cathode chemistries diversify into LFP, high-manganese, or nickel-rich systems, virtually all current mainstream architectures still rely on graphite anodes.

Defense systems sit at the intersection of these dependencies. High-performance motors and actuators require rare-earth magnets; precision guidance, radar, and satellite payloads rely on GaN and GaAs; advanced optics draw on germanium; and secure, mobile power systems benefit from cutting-edge battery technologies. From an industrial-risk perspective, the overlap between clean-energy and defense supply chains means that shocks from critical-mineral controls propagate across both domains simultaneously.

Scenarios, Constraints, and Structural Trade-Offs

Alternative Sourcing and the Reality of Ramp-Up Timelines

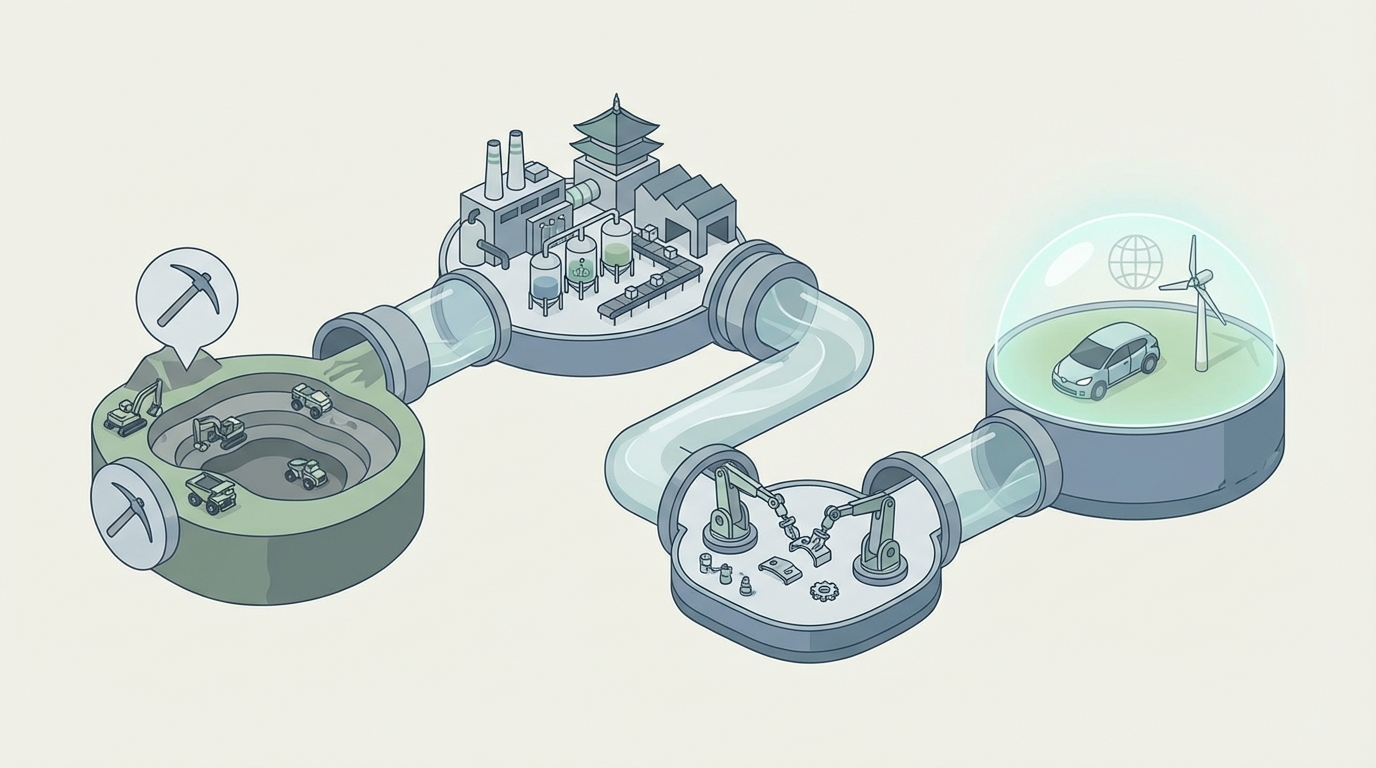

Discussions of diversification often focus on new mining projects. For gallium, germanium, rare earths, graphite, and tungsten, that is only part of the picture, and rarely the binding constraint in the short to medium term. Ore bodies and concentrates can be found or expanded in multiple jurisdictions; the bottleneck is usually the processing and refining capacity capable of meeting high-purity specifications at industrial scale under contemporary environmental standards.

Several structural constraints shape the scenario space:

- By-product dependence: Gallium and germanium supply expansions depend on the economics of alumina, zinc, copper, and coal operations. A refinery may have the geological potential to recover these elements but lack installed circuits or incentives to do so.

- Capital and permitting cycles: Building solvent-extraction plants for rare earths, high-temperature graphitization facilities, or advanced refining for by-product metals requires multi-year capital deployment and environmental permitting, particularly in OECD jurisdictions.

- Process know-how: Much midstream technology is tacit. Reproducing yield, impurity control, and product consistency takes time, even with access to basic flowsheets.

These factors explain why, even as exploration and project announcements accelerate in North America, Europe, and allied countries, actual diversification of midstream capacity progresses more slowly than political timelines often imply. The export-controls playbook is calibrated to this reality: leverage peaks during the years when alternative capacity is technically possible but not yet operational.

Substitution, Efficiency Gains, and the Technology Chessboard

One of the more subtle dimensions of China’s critical-minerals strategy is its interaction with technological substitution. Controls can accelerate R&D into alternatives—such as induction motors that avoid rare-earth magnets, silicon carbide (SiC) displacing some GaN use cases, or silicon-rich anodes reducing graphite intensity—but substitution is rarely binary.

Material-efficiency gains also matter. EV motor designers, for example, can re-optimize magnet geometries to reduce dysprosium loading, or switch to grain-boundary diffusion processes that lower heavy rare-earth consumption while maintaining performance. Graphite usage per kWh of battery capacity can decline through higher silicon content in composite anodes, although this introduces cycle-life and swelling challenges.

From a strategic perspective, Beijing’s ability to modulate export pressure over time interacts with these technology trajectories. Prolonged tight controls could accelerate structural substitution, gradually eroding Chinese leverage in specific materials. Calibrated, episodic controls—and targeted licensing that favors some end uses or partners over others—can instead shape substitution pathways to align with Chinese industrial strengths and geopolitical objectives.

In other words, the playbook is not static. It evolves as technologies, demand profiles, and allied industrial policies change. “After 2023, critical-mineral controls stopped being a blunt embargo tool and became a dynamic parameter in how technology roadmaps and industrial policies are drawn.”

Conclusion: Reading the Playbook as an Engineering and Systems Problem

The phrase “from gallium to germanium: understanding China’s critical minerals export playbook” captures a broader structural shift in global materials politics. The core move is consistent across metals: identify chokepoints where Chinese firms dominate midstream processing and high-purity refining, then integrate those nodes into a flexible export-licensing regime framed in dual-use and national-security terms.

For the critical-metals complex, the significance lies less in any single control announcement and more in the architecture that is being built. Export controls on gallium and germanium demonstrated how vulnerable compound semiconductor and optics supply chains are to by-product metals. Rare earths and magnets illustrate the power of midstream separation and alloying dominance. Graphite and tungsten show how deeply clean energy, industrial manufacturing, and defense systems are intertwined through a handful of processing technologies.

Materials Dispatch’s assessment is that critical-mineral export controls have become a permanent feature of the industrial landscape, not a transient bargaining chip. They function as a form of “process infrastructure statecraft,” where control over specific refining and separation assets translates directly into geopolitical leverage. Monitoring this terrain so requires tracking new control-list proposals, expansions of midstream capacity outside China, technology substitutions that shift materials intensity, and changes in licensing behavior over time as weak signals of strategic intent.

In this environment, the decisive variable is not whether critical-mineral controls will be used again, but how, where, and with what level of technical precision. Those patterns will be shaped by ongoing active monitoring of weak signals across policy, technology, and processing capacity build‑outs worldwide.

Note on Materials Dispatch methodology Materials Dispatch integrates regulatory texts from bodies such as MOFCOM and Western export-control authorities, technical literature on refining and separation processes, and market data on capacity and trade flows. This combined lens—legal, engineering, and volumetric—underpins the analysis above and supports continuous monitoring of weak signals that foreshadow shifts in critical-mineral leverage.