Project Vault: How a $10 Billion Stockpile Quietly Rewired Critical Minerals Policy

Materials Dispatch cares about Project Vault for a blunt reason: this is the first time since the Cold War that the United States and a broad coalition of partners have decided that rare earths, cobalt, gallium, and other strategic inputs are too important to leave to a mostly uncoordinated spot market. Clients allocate multi‑year budgets to secure these materials; suppliers and traders structure portfolios around them. Every time Chinese export controls choke gallium flows, or rare earth shipments stall in a port strike, procurement teams have to rewrite playbooks in real time. Project Vault turns those ad‑hoc stress tests into a permanent policy environment.

For Materials Dispatch, the inflection point was the sequence of shocks between 2020 and 2025: COVID‑era logistics breakdowns, the 2023 Chinese export license regime on gallium and germanium, and rolling rumors of rare earth quota tightening. Each episode forced defense primes, EV supply chains, and magnet makers to overpay for last‑minute tonnage or accept production delays. Against that backdrop, a $10 billion U.S. strategic stockpile, tied to a 55‑nation preferential trade framework with price support mechanisms, is not a marginal policy tweak; it is a structural rewrite.

Key points

- Project Vault commits $10 billion to U.S.-led critical minerals stockpiling, procurement, and allied capacity building, announced at the February 2026 Critical Minerals Ministerial in Washington.

- A 55‑nation “Minerals Security Alliance” framework layers preferential trade and price support mechanisms over Vault, effectively carving out a bloc market for non‑Chinese supply.

- Compared with the legacy U.S. National Defense Stockpile and allied reserves, Vault is larger, more targeted to REEs and battery metals, and explicitly linked to pricing floors and tender schedules.

- If implemented broadly as announced, Vault and the alliance framework could structurally reroute supply, narrow arbitrage for traders, and hard‑wire provenance and compliance expectations into contracts.

- Execution risks are significant: intra‑bloc tensions, verification challenges, and potential Chinese countermeasures could limit how far the framework actually shifts market power.

FACTS: What Project Vault and the 55‑Nation Framework Actually Do

1. Core design of Project Vault

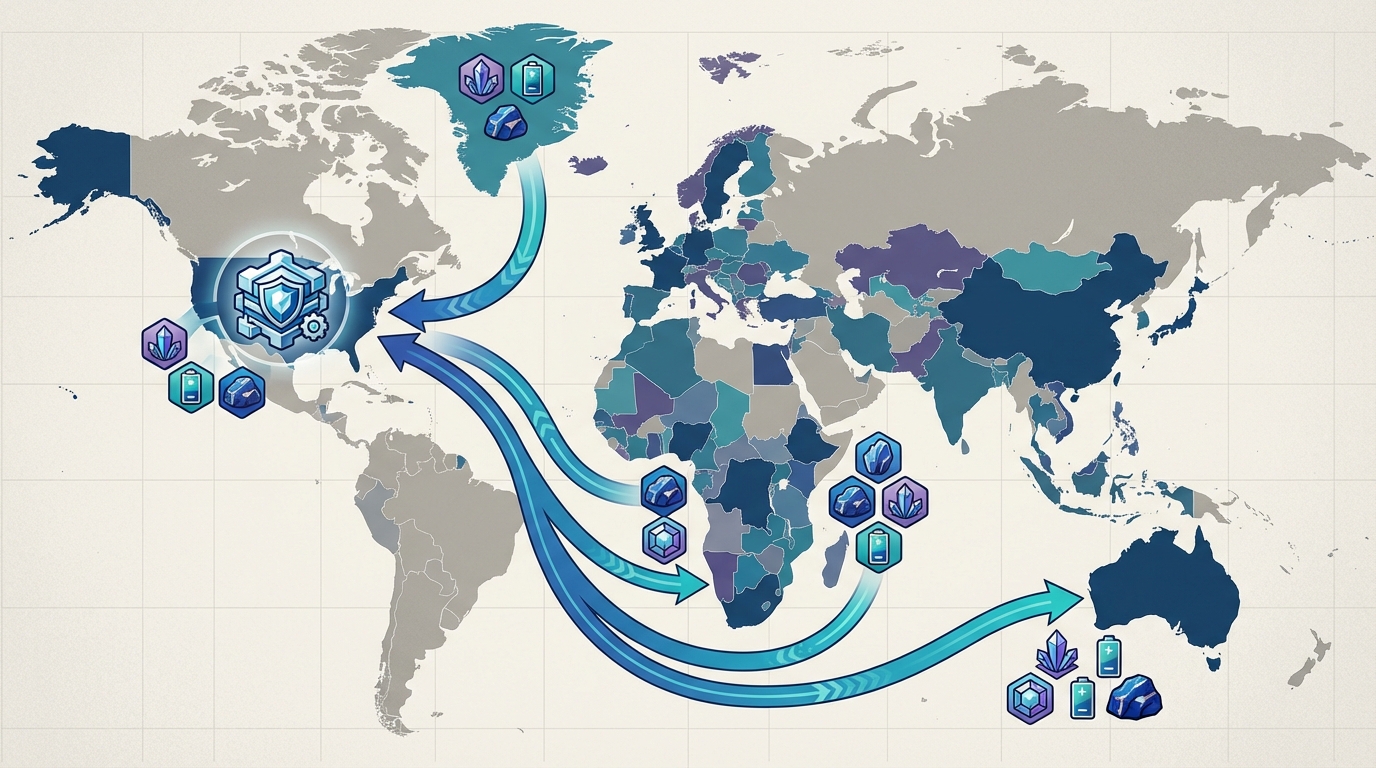

At the February 2026 Critical Minerals Ministerial in Washington, D.C., the United States announced Project Vault, a critical minerals stockpiling initiative with an initial $10 billion commitment. The program is structured around three pillars:

- Acquisition and storage: A multi‑year acquisition program for strategic minerals, including rare earth oxides (with emphasis on neodymium, praseodymium, and dysprosium), cobalt, gallium, lithium, and nickel, paired with investments in storage and handling infrastructure.

- Domestic processing incentives: Funding to expand U.S. processing and refining capacity for these materials, complementing the physical stockpile and aiming to reduce dependence on foreign refining, particularly from China.

- Allied capacity building: Support for partner countries’ mining and processing projects, tied to the broader preferential trade framework agreed at the same ministerial.

According to U.S. government statements, Vault is designed as a standing buyer through structured tenders, not a one‑off procurement. Program documents describe recurring tenders for rare earth oxides and cobalt, targeting a strategic reserve equivalent to a significant share of combined defense and electric vehicle demand over a defined multi‑year horizon. The funding draw reportedly rests partly on Defense Production Act authorities and recent industrial policy legislation.

Compared to the pre‑Vault U.S. National Defense Stockpile (NDS), which held relatively modest tonnages of rare earths and focused heavily on legacy metals such as beryllium, chromium, and titanium, Vault explicitly prioritizes materials that underpin permanent magnets, advanced electronics, and battery chemistries. NDS operations historically lacked explicit price support mechanisms; Vault’s architecture directly contemplates interacting with market price signals.

2. The 55‑nation “Minerals Security Alliance” framework

Alongside Vault, the ministerial produced a 55‑nation preferential trade and coordination framework widely referred to as a Minerals Security Alliance (MSA). Participating states reportedly include:

- The Five Eyes countries (United States, Canada, United Kingdom, Australia, New Zealand).

- Most EU member states, plus Japan and South Korea.

- Several major resource holders in Latin America and Africa, including Brazil, South Africa, and the Democratic Republic of the Congo.

- Key Indo‑Pacific partners such as India.

The framework is described as offering preferential tariff treatment for intra‑bloc trade in specified critical minerals, while establishing coordination mechanisms on export volumes, environmental and labor standards, and traceability requirements. A shared price support fund, backed in part by U.S. commitments, is intended to operate alongside Project Vault by stabilizing prices for certain minerals extracted and processed within the bloc.

Program descriptions cite the use of digital provenance tools, including blockchain‑based tracking and third‑party audits, to verify origin and compliance for shipments claiming MSA preferences. Implementation dates in the communiqués place the first wave of these requirements in the second half of 2026, with further tightening thereafter.

3. Price support mechanisms and observable market signals

Vault and the MSA framework incorporate price support mechanisms in two distinct ways:

- Direct stockpile purchasing: Vault tenders act as a buyer of last resort for allied production, creating an effective floor for certain materials when spot prices weaken.

- Dedicated support fund: Within the 55‑nation framework, a pooled fund is allocated to stabilizing prices via mechanisms such as guaranteed minimums, loan guarantees, or deficiency payments on qualifying output.

Public and industry data points give some sense of the reference levels in play. Fastmarkets assessments cited in ministerial briefings put neodymium‑praseodymium (NdPr) prices at around $212.60/kg for praseodymium at the time of the meeting, reportedly up about 47% year‑to‑date. Internal modeling referenced by officials implied that Vault’s procurement and support mechanisms could be consistent with sustained levels closer to $250/kg in tight‑supply scenarios, particularly if Chinese export quotas were tightened further.

In cobalt, basis trades between London Metal Exchange contracts and Shanghai physical premiums were reported to have widened by around 15% around the time of the announcement, reflecting shifting expectations around floor prices and bloc‑aligned demand. For dysprosium, internal government planning materials referenced Vault’s role in covering a projected 2026 U.S. deficit, where anticipated demand of roughly 1,000 metric tons was expected to exceed assured supply by around 600 metric tons in the absence of dedicated stockpiling.

4. Comparison with existing U.S. and allied stockpiling programs

Historically, the U.S. National Defense Stockpile and comparable allied programs were:

- Focused on a broader set of industrial and military metals, with less emphasis on rare earths and battery materials.

- Run largely as unilateral, nationally scoped programs, with only loose coordination through NATO or bilateral arrangements.

- Administered with limited integration into trade policy or explicit price support regimes.

By contrast, Project Vault is characterized by:

- A larger nominal budget than recent NDS authorizations, concentrated on a tighter list of critical inputs.

- Formal linkage to a multinational preferential trade framework, rather than standalone national stockpiling.

- A design that anticipates regular market interaction via tenders and support mechanisms intended to influence both availability and pricing, not just emergency readiness.

Allied initiatives, such as Australia’s critical minerals reserve programs and the European Union’s strategic raw materials initiatives, exist alongside Vault but do not, on their own, combine the same scale of U.S. funding, explicit price interaction, and bloc‑wide trade preferences. Ministerial documentation emphasizes coordination rather than replacement of these existing efforts.

INTERPRETATION: How Project Vault May Rewire Markets and Operations

5. A deliberate shift from market‑first to state‑directed security

Materials Dispatch’s reading is that Project Vault represents a conscious decision to treat key critical minerals as strategic assets analogous to munitions or energy reserves, not just as commodities managed via private contracts. To the extent that Vault tenders proceed on the announced scale, a non‑commercial buyer enters the market with objectives that are explicitly not profit‑maximizing: resilience, national security, and allied leverage sit ahead of short‑term price efficiency.

This shift did not emerge in a vacuum. The 2010 rare earth export dispute between China and Japan, the COVID‑era shipping breakdown, and the 2023 Chinese export controls on gallium and germanium all tested the assumption that global markets would always clear efficiently. In practice, procurement teams ended up scrambling to qualify new suppliers, paying up for marginal tons, or pausing production. Vault is a policy response to that operational reality.

If Vault consistently absorbs a defined slice of non‑Chinese rare earth and cobalt output on bloc‑friendly terms, the “world price” for these materials could bifurcate: a bloc‑linked corridor with implicit or explicit floors, and a residual market for non‑aligned buyers with more volatility and potentially higher embedded geopolitical risk. From a risk‑management perspective, that is a deliberate trade‑off: less exposure to sudden shocks for bloc‑aligned demand, more fragmentation and complexity for everyone else.

6. Operational implications across the chain

For upstream mining and processing projects in aligned jurisdictions, Vault and the MSA framework function as a de‑risking overlay. If tenders and support mechanisms are executed as described, long‑cycle projects in Australia, North America, and parts of Africa gain a clearer path to sustained demand for compliant tonnage. That tends to:

- Shorten decision cycles around expansions or new projects that can meet MSA environmental, labor, and provenance standards.

- Elevate the importance of independent ESG audits, blockchain‑style traceability, and export licensing disciplines in project evaluation.

- Make offtake linked to MSA eligibility more valuable than physically similar material lacking verified provenance, purely because of policy overlay.

For traders and midstream processors, the move cuts both ways. On one hand, predictable government tenders and price support mechanisms reduce downside risk for qualified flows. On the other, classic arbitrage between regions may narrow if a majority of non‑Chinese supply is directed into the bloc via preference regimes. Basis trades, particularly in cobalt, already reflect this: widening spreads between LME benchmarks and Chinese physical markets around the Vault announcement signal diverging risk and policy regimes rather than pure logistics or quality differentials.

Downstream manufacturers-especially magnet producers, EV makers, and defense primes-stand at the sharp end of provenance and compliance requirements. If MSA certification effectively adds ninety days to contract cycles, as some ministerial briefings have suggested, that is a non‑trivial alteration of procurement workflows. Legacy playbooks that prioritized cheapest compliant tonnage from anywhere are being displaced by multi‑criteria sourcing: origin, auditability, and alignment with bloc policy now sit alongside technical specifications and cost.

The dysprosium example is emblematic. Internal planning assumptions that Vault stockpiles will cover a projected 2026 gap between U.S. demand and secure supply effectively anchor defense planners’ expectations. To the extent Vault actually acquires that material on schedule, missile guidance systems and high‑temperature magnets feel less exposed to quota shocks or port disruptions. If acquisitions lag, the same projected gap could reappear with added complexity, as potential spot supply outside the bloc faces stricter compliance filters.

7. Can the 55‑nation framework hold under real pressure?

The most ambitious part of the ministerial outcome is not the $10 billion headline, but the assumption that 55 countries with very different geological profiles and political economies can sustain a coherent Minerals Security Alliance.

There are clear strengths. Concentrating a large share of non‑Chinese rare earth and cobalt reserves inside an explicit framework, with U.S. financial backing and shared standards, materially increases collective bargaining power with downstream industry. For states such as Australia or Canada, the framework validates years of work pushing critical minerals from niche topic to strategic agenda. For processing‑constrained economies like the United States, the alliance creates a structured environment to import refined material without being wholly dependent on adversarial suppliers.

However, Materials Dispatch does not see the framework as a done deal. To the extent that environmental, labor, and traceability standards are enforced rigorously, some producer states will face real domestic trade‑offs. Brazil’s niobium producers or DRC cobalt operations may find that stricter audit regimes collide with domestic political priorities. India’s desire to expand its own processing industry could create friction if alliance export coordination is perceived as constraining its autonomy.

Verification and enforcement are another pressure point. Provenance fraud has already appeared in rare earth supply chains, including documented cases where throughput from high‑profile operations did not match declared exports. Blockchain tracking and ISO‑type certifications help, but they are not a panacea. If verification lags or bad actors can launder non‑compliant material into the MSA stream, the credibility of the framework’s “trusted supply” claim erodes quickly.

Finally, there is the question of Chinese counter‑strategy. If Beijing responds with targeted quota tightening, tax incentives for allied‑country plants that continue to use Chinese‑origin intermediates, or subsidized offtake for non‑aligned producers, the bloc could face a moving target. In that scenario, Vault’s tenders and price supports would be operating not against a static benchmark, but against a rival state‑directed system with its own levers.

WHAT TO WATCH: Signals That Will Define Project Vault’s Real Impact

- Vault tender cadence and fill rates: Whether REE and cobalt tenders are fully subscribed, partially filled, or repeatedly delayed will show how quickly upstream projects are aligning to bloc requirements.

- Fastmarkets NdPr and dysprosium behavior vs. implied floors: Persistent divergence between observed prices (e.g., the $212.60/kg praseodymium reference) and implied Vault floor levels near $250/kg would signal either over‑ or under‑delivery of stockpiling commitments.

- Share of non‑Chinese supply tied to MSA contracts: Public disclosures from producers such as Australian REE miners or North American cobalt refiners will indicate how much tonnage is effectively removed from free‑floating global trade.

- Enforcement cases and provenance disputes: Early audits, shipment rejections, or fraud investigations around MSA‑certified flows will reveal how serious member states are about standards versus volume.

- Chinese policy responses: Any new export quota rounds, licensing regimes, or targeted subsidies for non‑aligned projects will define whether Vault is operating in a cooperative, competitive, or confrontational ecosystem.

- Evolution of allied national stockpiles: Adjustments to the U.S. NDS, EU strategic reserves, or allied national programs in light of Vault will show whether governments view Vault as additive or partially substitutive.

Conclusion

Project Vault is not a technocratic footnote; it is a deliberate decision to move critical minerals away from a loosely coordinated global spot system toward a bloc‑anchored, state‑directed architecture. The $10 billion commitment, coupled with a 55‑nation preferential framework and explicit price support mechanisms, signals that the United States and its partners are prepared to absorb real economic and diplomatic friction to secure supply.

Whether this ultimately reduces strategic vulnerability or simply fragments markets depends on execution: the credibility of tenders and floors, the cohesion of alliance members, and the nature of Chinese countermeasures. For now, the operational reality is already shifting. Procurement, compliance, and supply chain governance are being re‑written around Vault and the MSA, regardless of whether all long‑term goals are met. Materials Dispatch will continue active monitoring of regulatory and industrial weak signals around Project Vault and the Minerals Security Alliance, as these will define how much of the announced architecture translates into durable structural change.

Note on Materials Dispatch methodology Materials Dispatch assessments integrate continuous monitoring of U.S., EU, Chinese, and allied regulatory texts, communiqués, and agency rulemakings with observable market behavior where price and volume data are available. For Project Vault and the Minerals Security Alliance, this briefing cross‑references official ministerial documentation with reported tender structures and end‑use technical specifications in sectors such as permanent magnets, battery materials, and defense systems, without projecting unverified numerical forecasts.