Market Forecast

Top 12 strategic materials most exposed to chinese export controls in 2026: Latest Developments and

Top 12 Strategic Materials Most Exposed to Chinese Export Controls in 2026

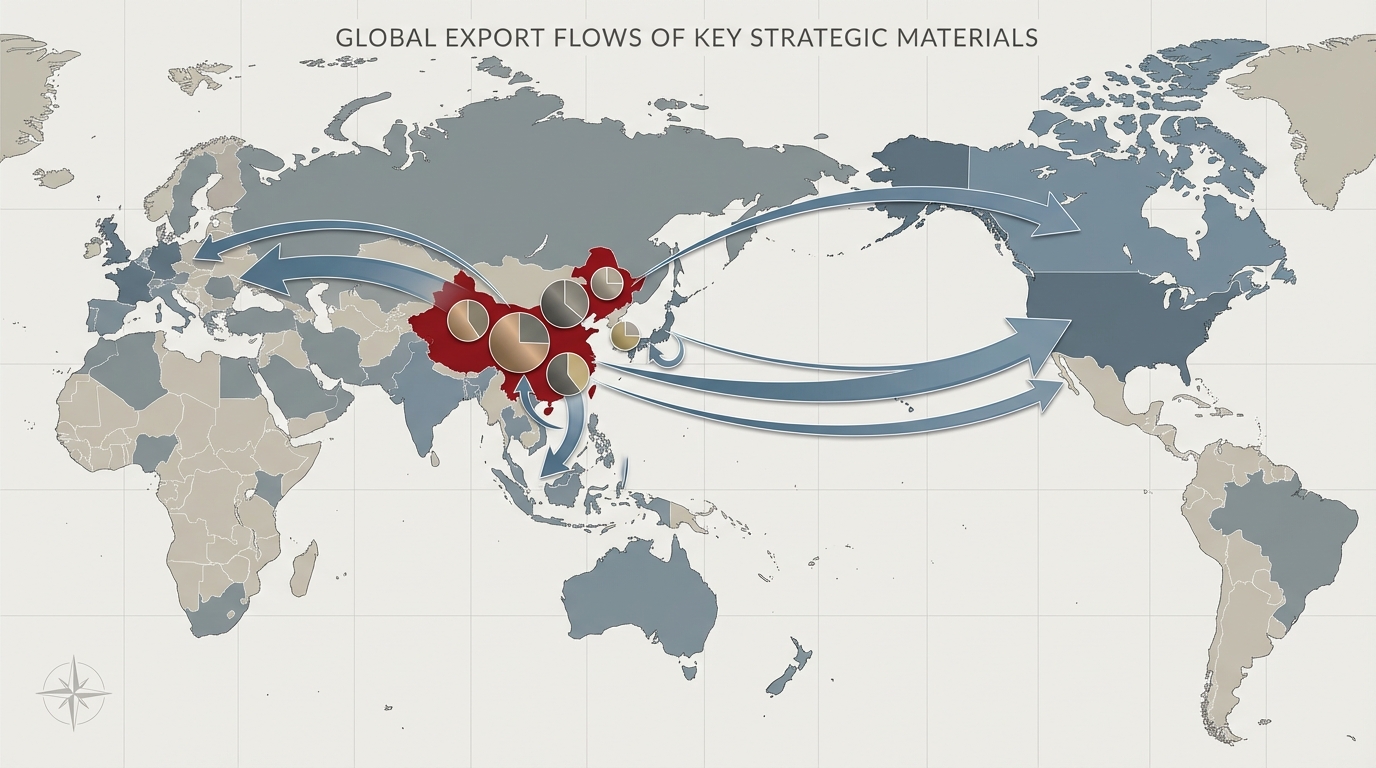

China’s export control regime for strategic metals enters a harder phase in 2026. Fixed exporter lists for tungsten, antimony and silver sit alongside ongoing licensing for rare earth elements (REEs), gallium, germanium, graphite and others. The result isn’t a theoretical policy risk; it’s a live constraint that’s already reshaping procurement in defense, semiconductors, EVs and grid-scale renewables.

Materials Dispatch ranks the Top 12 strategic materials most exposed to Chinese export controls in 2026 by one metric that matters operationally: control risk. That means not just how dominant China is, but how tight the current rules are, how long the November 2026 rare-earth “pause” can realistically last, and how fast non-Chinese capacity can credibly scale.

Across these 12 materials, China typically accounts for more than 70% of global production or processing. For some, like antimony and heavy rare earths, the figure is over 80-90%. Fixed exporter slots for 2026-2027 effectively cap many metals at around 80-90% of 2025 export volumes. In parallel, rare-earth and semiconductor-material licensing will resume after the current truce window that runs to 10 November 2026, with no binding commitment to relax volumes.

On the factory floor, this translates into very concrete problems: battery plants redesigning chemistries, defense primes pulling forward orders, and semiconductor fabs quietly lengthening lead times for GaAs and GaN devices. One European procurement head told Materials Dispatch that 2026 is “less about price and more about whether material shows up at all.” This briefing is built for that reality: which materials break first, what that does to production schedules, and which alternatives are actually bankable within an 18‑month horizon.

Ranking Methodology

Control risk scores (1–10, higher = greater exposure) integrate five dimensions:

- Dominance factor: China’s share of global production and especially processing (USGS and industry data). Many entries exceed 80%.

- Policy stringency: Quotas, non-automatic licenses, exporter lists and outright bans as reflected in MOFCOM and related announcements through 2025.

- Geopolitical friction: Use of controls as leverage in response to tariffs, chip restrictions and defense-tech sanctions.

- Supply impact: Documented export declines (e.g., tungsten exports down 13.75% Jan–Sep 2025; gallium exports down roughly 30% in 2025).

- Strategic multiplier: Degree of dependence in defense, semiconductors, critical energy and systems with few or no substitutes.

We also differentiate by time frame. Some controls, like the REE and semiconductor-material licensing pause, are formally relaxed until November 2026 but remain structurally in place. Others, such as fixed exporter lists, are already constraining 2025 shipments and are effectively hard ceilings for 2026–2027. In most cases, we model 2026 export volume reductions versus 2025 in the 10–30% range, absent aggressive diversification.

The ranking prioritizes materials where a 2026 disruption translates directly into missed defense-readiness milestones, idled semiconductor lines or EV and solar buildout delays. Each entry sets out the asset and risk, the strategic context, the bottleneck, and a verdict on criticality and signals to track.

1. Antimony (Control Risk: 10/10)

The asset and risk. Antimony is the most exposed material in 2026 because it combines extreme Chinese dominance with fresh, tight controls. China supplies around 84% of global antimony, and for 2026–2027 has confirmed a small, fixed roster of exporters, unchanged from 2025. Antimony is not just a minor alloying metal: it’s central to flame-retardant formulations, lead-acid and some advanced batteries, and specialty military applications. For defense users in particular, antimony concentrates and trioxide are already treated as “go/no-go” inputs for munitions production.

Strategic context and bottleneck. Antimony was pulled into China’s export-control net in late 2024 under non-automatic licensing. Licensing reviews have historically produced 2–4 month pauses, and since early 2025, export statistics show sharp declines in shipments. For 2026, fixed exporter lists and a security framing around munitions-grade materials mean Beijing can prioritize domestic demand — including a rapid ramp in ammunition output, widely estimated to be running at several times U.S. throughput. Non-Chinese supply is thin: Mandalay Resources’ Hillgrove restart in Australia and small volumes from Russia-linked assets cannot offset even a low double-digit percentage shock.

Verdict and signals. Materials Dispatch assigns antimony a 10/10 control risk. For many NATO-aligned defense supply chains, existing stocks likely cover 6–12 months at current burn rates. After that, unless Hillgrove and other projects clear permitting and ramp smoothly, munitions and specialty flame-retardant capacity is exposed to outright curtailment. Key signals to watch in 2026: changes in China’s exporter list, any security-designation language in MOFCOM circulars, and restart timelines or offtake announcements from Hillgrove and other non-Chinese assets. Antimony is the material that defense ministries and ammunition makers are already triaging first.

2. Tungsten (Control Risk: 9.5/10)

The asset and risk. Tungsten’s combination of ultra-high melting point, hardness and density makes it indispensable in armor-piercing munitions, cutting tools, aerospace turbine components and some semiconductor processes. China controls over 80% of global tungsten production and an even higher share of downstream processing. For 2026–2027, Beijing has locked in a finite number of approved exporters, while maintaining licensing on powders and many dual-use products.

Strategic context and bottleneck. Since China tightened tungsten export administration in early 2025, exports have fallen by around 13.75% (Jan–Sep 2025 year-on-year). Fixed exporter slots, combined with conservative licensing, are expected to cap 2026 export volumes at roughly 80–90% of 2025 levels. For Western buyers, the shortfall is magnified because domestic Chinese demand for tools and defense applications continues to climb. Non-Chinese supply exists but is fragmented: Spain’s Barruecopardo mine and Portugal’s operations add thousands of tonnes per year, while Almonty Industries’ Sangdong project in South Korea is targeting >5,000 t/year WO3 equivalent from 2026. Each comes with its own risks — Iberian logistics bottlenecks, Korean labor action, and ramp-up uncertainties.

Verdict and signals. With limited substitutability (alternatives often add 20–30% cost or degrade performance), tungsten earns a 9.5/10 control risk. Tooling, aerospace and ammunition lines are already shifting to multi-year offtake contracts with non-Chinese producers, sometimes at significant premia. The critical watchpoints in 2026: Sangdong’s actual ramp profile versus nameplate, any further tightening of export licenses on tungsten powders and carbides, and evidence of Chinese material being laundered through third-country processors. If Sangdong or key European mines slip, expect a second round of price spikes and, more importantly, allocation-based selling favoring strategic sectors over general industry.

3. Dysprosium (Control Risk: 9/10)

The asset and risk. Dysprosium is a heavy rare earth (HREE) used in small quantities to transform the performance of NdFeB permanent magnets, especially at high temperatures. It improves coercivity, allowing magnets to operate reliably in EV traction motors and precision-guided munitions. China dominates dysprosium not just in mining but in separation and processing, with >99% of separated supply effectively under Chinese control.

Strategic context and bottleneck. In April 2025, China extended export licensing to seven key rare earths, including dysprosium. A subsequent diplomatic “truce” led to a licensing pause for some U.S.-bound flows, currently scheduled to run to 10 November 2026. But the legal architecture of the controls remains intact. Defense and EV manufacturers report that dysprosium-containing magnet purchases already come with origin and compliance caveats, and some lots have been delayed during licensing reviews. Outside China, true heavy-REE capacity is minimal. Lynas’ Mt Weld provides limited dysprosium oxide via Malaysia, but heavy-REE separation in North America has slipped to at least 2026–2027, and early volumes will be small.

Verdict and signals. Dysprosium is rated 9/10 control risk because once the pause ends, licensing can be tightened very quickly without passing new laws. A 20–40% reduction in dysprosium exports would translate into a sharp squeeze in high-performance NdFeB magnet availability and potentially a 40–50% jump in magnet prices. Signals to monitor: any guidance from Beijing that frames dysprosium as national-security sensitive, Lynas’ progress on heavy-REE circuits in the U.S., and OEM design decisions moving toward dysprosium-lean or dysprosium-free motor architectures. For 2026–2027, missile programs and premium EV platforms remain the most exposed.

4. Terbium (Control Risk: 9/10)

The asset and risk. Terbium is another heavy rare earth, crucial in two very different domains: high-efficiency green phosphors for displays and lighting, and as a dopant in high-end magnets where it can roughly double coercivity. Its role in advanced sensors and some F-35 avionics gives it outsized strategic weight relative to tonnage. China processes roughly 98% of the world’s terbium, and there are virtually no independent non-Chinese separation streams at scale.

Strategic context and bottleneck. Terbium is bundled with dysprosium, samarium, gadolinium, scandium, lutetium and yttrium in the April 2025 export-control package. Since then, export data suggests terbium shipments have fallen sharply, in some estimates by up to half relative to pre-control baselines. The 2026 licensing pause temporarily eases pressure for certain destinations, but the underlying message remains clear: terbium is classified as a dual-use and defense-relevant asset. Japanese and European recyclers, including magnet and phosphor recovery facilities, are scaling, yet volumes remain in the low hundreds of tonnes per year with purity and consistency challenges.

Verdict and signals. Terbium scores 9/10 on control risk given the near-total concentration and demonstrated willingness to tighten exports. For display makers and specialty magnet producers, the realistic options in 2026 are early offtake agreements from new separation facilities (for example in Canada and Europe), aggressive recycling, and product redesign to reduce terbium intensity. Signals to track: ramp schedules at Neo Performance Materials’ facilities, technical performance of recycled terbium in high-spec magnets, and any extension or re-scoping of the November 2026 licensing pause. Terbium is likely to remain a persistent constraint, with defense and aerospace end-uses strongly favored in allocation.

5. Gallium (Control Risk: 8.5/10)

The asset and risk. Gallium underpins compound semiconductors such as GaAs and GaN, which are central to 5G/6G infrastructure, radar, satellite communications and high-frequency power electronics. China accounts for roughly 98% of primary gallium production, largely as a by-product of alumina refining. In 2023, Beijing imposed export licensing on gallium metal and key compounds, specifically linking controls to national security and advanced semiconductor use.

Strategic context and bottleneck. Following the introduction of controls, gallium exports dropped by about 30% in 2025, with some buyers reporting multi-month delays in securing export licenses. In mid-2025, a partial pause for shipments to the United States and some allies was introduced, again running to November 2026. However, the formal control regime remains in force. Alternative supply is emerging: producers in Europe, Japan and the U.S. can collectively offer tens of tonnes per year, but cost structures are higher due to energy prices and smaller scale. AXT Inc. in the U.S. and Freiberger Compound Materials in Germany are among the key non-Chinese players, yet current capacity covers only a fraction of global demand growth.

Verdict and signals. Gallium earns an 8.5/10 control risk. For radar manufacturers and RF semiconductor foundries, a 6–12 month stock horizon is already being treated as a minimum. Fabs have been quietly diversifying to non-Chinese gallium where specifications allow, accepting higher costs as insurance. Signals to watch in 2026: whether MOFCOM narrows the scope of the licensing pause, the pace of secondary gallium recovery from bauxite residue outside China, and long-term offtake contracts signed by Western fabs with non-Chinese refiners. Any renewed escalation in U.S.–China tech tensions would likely show up first in gallium license denials.

6. Germanium (Control Risk: 8.5/10)

The asset and risk. Germanium is a critical input in infrared optics, fiber-optic systems, certain high-efficiency solar cells and specialized semiconductor devices. It is typically produced as a by-product of zinc and coal operations. China controls about 60% of refined germanium and an even larger share of high-purity germanium used in defense and telecom applications. Like gallium, germanium was brought under Chinese export controls in 2023 via a licensing regime.

Strategic context and bottleneck. Export licensing has already reduced Chinese germanium exports and elongated lead times, particularly for high-purity products. A similar pause for some destinations applies up to November 2026, but again the legal structure persists. Outside China, refining capacity is concentrated at facilities such as Umicore’s Olen plant in Belgium, which can produce on the order of 10 tonnes per year. Even at full stretch, current non-Chinese capacity cannot fully replace Chinese exports without aggressive recycling and substitution. Because germanium is a co-product, ramping supply requires either new primary mine investment or adjustments in existing zinc and coal flows, both of which have long lead times.

Verdict and signals. Germanium is assessed at 8.5/10 control risk. Infrared optics for drones, missile seekers, and some satellite payloads are particularly exposed, as are telecoms operators relying on specialty fiber products. Signals to track: published Chinese export data post-2026, utilization rates at European and North American refining facilities, and any policy moves to classify germanium-bearing waste as strategic for recycling. Defense programs with heavy IR requirements are already working to pre-book multi-year germanium supply; the gap between those that do and those that don’t will become very visible if licensing tightens again after the pause.

7. Silver (Control Risk: 8/10)

The asset and risk. Silver is often framed as a precious metal, but industrial demand — especially from solar, electronics and EVs — now dominates. China accounts for only about 10–15% of global mine production, yet plays an outsized role in refining and processing. In 2025, Beijing introduced for the first time a designated exporter list for silver, expanding slightly for 2026–2027 but still capping the number of firms permitted to ship abroad.

Strategic context and bottleneck. Silver’s control risk is less about immediate scarcity and more about systemic exposure. Chinese solar manufacturers and electronics assemblers are enormous consumers, and any tightening of export permissions or redirection of refined silver to domestic users could quickly squeeze global availability. Exporter caps function as a de facto quota: if demand rises, the approved firms can’t necessarily scale exports in line. At the same time, global silver demand for photovoltaics alone is expected to rise strongly as higher-efficiency cell designs use more silver per watt.

Verdict and signals. Silver receives an 8/10 control risk in this ranking because it sits at the intersection of energy transition scale and emerging Chinese control tools. Non-Chinese producers like Hecla’s Lucky Friday mine in the U.S., Mexico’s large base-metal-silver operations, and Peru’s polymetallic mines are viable supply anchors, but much of this silver is produced as a by-product, limiting rapid increases. Signals to watch in 2026: any tightening of China’s exporter list, domestic Chinese solar deployment targets, and changes in refining charge terms. Solar-module producers and electronics OEMs heavily reliant on Chinese silver feedstock have the greatest near-term exposure.

8. Yttrium (Control Risk: 7.5/10)

The asset and risk. Yttrium is used in radar components (notably yttrium iron garnet filters), advanced ceramics, phosphors and some superconducting materials. It is another heavy rare earth where China dominates: estimates put Chinese control at around 95% of global processed yttrium. Volumes are modest, but the applications are acute in defense and high-frequency electronics.

Strategic context and bottleneck. Yttrium was pulled into the April 2025 package of controlled REEs, with export licensing extended to metals, oxides and many compounds. Although the 2026 pause has dampened immediate friction for some buyers, compounds essential for ceramics and garnet-based components have already shown reduced availability and longer lead times. Outside China, yttrium output is limited and often occurs as a co-product of broader REE streams. Projects in the U.S. and Australia, including Energy Fuels’ planned HREE circuit at White Mesa, are targeting limited yttrium and related HREE recovery around 2026–2027.

Verdict and signals. Materials Dispatch scores yttrium at 7.5/10 control risk. For electronics and defense primes, the key concern is not overall tonnage but the high specificity of supply: components qualified years ago to particular yttrium sources and chemistries can’t readily switch. Signals to monitor in 2026 include commissioning status at North American HREE separation plants, any MOFCOM guidance specifically naming yttrium in the context of radar or EW systems, and stockpiling behavior by radar-system integrators. If heavy-REE projects outside China slip timelines, yttrium could move quickly from a “background” issue to a frontline bottleneck.

9. Samarium (Control Risk: 7.5/10)

The asset and risk. Samarium is best known for its role in samarium–cobalt (SmCo) permanent magnets, which offer exceptional performance at high temperatures. These magnets are crucial in jet engines, some missile systems and space applications where NdFeB magnets can’t tolerate the thermal environment. China mines and processes the overwhelming majority of global samarium-bearing ores and concentrates, and as with other HREEs, dominates separation.

Strategic context and bottleneck. As part of the April 2025 REE controls, samarium now falls squarely under export licensing for metal and selected compounds. While volumes are smaller than for NdFeB-related REEs, SmCo magnet supply chains are tightly concentrated, with much of the global production dependent on Chinese feedstock or processing steps. There are technically alternative magnet chemistries, but switching involves significant design, qualification and performance compromises, particularly for aerospace and defense programs already in production.

Verdict and signals. Samarium is assessed at 7.5/10 control risk. It doesn’t yet present the same macroeconomic risk as antimony or tungsten, but for niche applications it’s effectively single-sourced. Signals to watch through 2026 include investments in Western SmCo magnet capacity, any moves by China to explicitly tie samarium exports to aerospace or defense policy, and the extent to which heavy-REE projects outside China can yield samarium streams at meaningful scale. For high-temperature motor and generator programs, risk mitigation will hinge on requalifying magnets from more diversified supply chains rather than expecting Chinese controls to loosen.

10. Gadolinium (Control Risk: 7/10)

The asset and risk. Gadolinium has two critical, though very different, uses: as an MRI contrast agent in medical imaging, and as a neutron absorber in nuclear reactors and some naval propulsion systems. In both cases, safety and performance requirements are strict. China dominates gadolinium production and separation along with other heavy REEs, controlling most of the high-purity oxides and compounds used globally.

Strategic context and bottleneck. Gadolinium is covered by the same April 2025 REE export licensing framework. Unlike dysprosium or terbium, it has not yet been the focus of prominent diplomatic disputes, but the administrative tools are identical. Medical systems and nuclear-technology suppliers typically run lean inventories and are accustomed to relatively predictable deliveries, making them sensitive to even moderate licensing delays. Outside China, gadolinium supply is limited to a handful of REE streams from projects in Australia, Russia and minor by-product producers, many of which are not yet configured for high-volume, medical-grade output.

Verdict and signals. Gadolinium scores 7/10 on control risk. The probability of deliberate, targeted restriction may currently be lower than for high-profile REEs, but the impact of any disruption would be immediate in healthcare and nuclear operations. Key signals to watch are regulatory changes around medical-grade gadolinium in China, commissioning of new separation facilities in Europe and North America, and early signs of stock-building by reactor operators. In a broader geopolitical crisis, gadolinium could move from a low-visibility controlled material to a flashpoint as governments move to secure nuclear and medical supply chains.

11. Graphite (Control Risk: 6.5/10)

The asset and risk. Graphite is the dominant anode material in lithium-ion batteries, accounting for the bulk of EV and stationary-storage demand. China produces about 65% of natural flake graphite and an even higher share of processed anode material, after adding synthetic graphite and purification steps. In 2023–2024, Beijing introduced licensing for several graphite categories linked to “super-hard” materials and battery use.

Strategic context and bottleneck. While some of these graphite controls were temporarily softened or paused for certain destinations through 2026, the direction of travel is clear: graphite is now framed as a strategic export. China has both the ore and the midstream refining capacity, which gives it leverage over global EV production. Non-Chinese alternatives such as Syrah Resources’ Balama mine in Mozambique, combined with processing in the U.S. and Europe, are ramping, but capacity remains well below projected EV demand. Synthetic graphite can offset some deficits, but at a cost premium and with higher energy intensity.

Verdict and signals. Graphite is assigned a 6.5/10 control risk. It sits slightly lower in this ranking because there’s a broader base of geological resources and several credible projects under construction or expansion outside China. However, any renewed tightening of graphite export licenses would quickly pressure EV and battery makers still heavily reliant on Chinese anode material. Signals to monitor in 2026 include commissioning of new active-anode-material plants in North America and Europe, Chinese policy statements about “overcapacity” in batteries, and shifts in OEM battery-chemistry roadmaps (for example, faster adoption of silicon-dominant or alternative-anode chemistries).

12. Scandium (Control Risk: 6/10)

The asset and risk. Scandium is a niche but strategically potent element. When added in very small amounts to aluminum, it produces Al–Sc alloys with significantly higher strength, weldability and fatigue resistance. These alloys are attractive for aerospace structures, some high-performance EV applications and advanced additive manufacturing. Global scandium supply is extremely small, measured in tens of tonnes per year, with China one of the key sources of both primary and by-product scandium.

Strategic context and bottleneck. Scandium is explicitly listed in China’s April 2025 REE-related export-controls cohort. Even though current demand is modest, aerospace primes and advanced-manufacturing firms are actively developing Al–Sc components for next-generation platforms. Most accessible scandium today comes from Chinese output, Russian by-product streams, and a limited number of projects in Australia and North America working to extract scandium from laterites or tailings. Commercializing these streams at consistent quality is non-trivial and can be delayed by permitting, financing and metallurgy challenges.

Verdict and signals. Scandium is rated at 6/10 control risk. It ranks below the high-volume or already-constrained metals, but for programs that have baked Al–Sc into designs, dependence on Chinese material is a real vulnerability. Signals to watch in 2026: qualification of non-Chinese scandium sources by major aerospace OEMs, technical performance of scandium extracted from waste streams, and any moves by China to explicitly position scandium as a defense-critical material. The key strategic choice for industry is whether to commit to Al–Sc at scale without a robust, diversified scandium supply base.

Strategic Implications for 2026 Supply Chains

Across these 12 materials, a consistent pattern emerges: China has built both mining and processing dominance and is now actively using export controls as a policy lever. Fixed exporter lists constrain tungsten, antimony and silver to roughly 80–90% of 2025 export volumes. Licensing regimes for REEs, gallium, germanium and graphite are in place for the long term, even if tactical pauses run to November 2026. In practice, this creates a two-stage risk for 2026–2027: initial supply friction followed by the potential for sharper, targeted restrictions if geopolitical tensions escalate.

Defense and semiconductor supply chains are already treating the top six materials in this ranking as requiring immediate triage. For antimony, tungsten, dysprosium, terbium, gallium and germanium, it’s less about marginal price increases and more about whether offtake contracts and licenses will secure physical material. A senior procurement manager at a European missile manufacturer summed it up to Materials Dispatch: “We’ve shifted from quarterly sourcing to multi-year locking of anything that touches Chinese controls.” That shift cascades downstream, tightening availability for smaller buyers.

Meanwhile, mid-tier risks such as silver, yttrium, samarium, gadolinium, graphite and scandium offer a short window of relative flexibility. Controls are in place, but non-Chinese projects and recycling can realistically cover a portion of incremental demand if planning starts now. The main operational failure mode here isn’t that alternatives don’t exist — it’s that permitting, qualification and logistics delays push real volumes into the late 2020s. The practical implication for 2026 is that supply security improves only where companies have already moved from talk to signed contracts and funded projects.

Non‑Chinese Supply Diversification Targets

Mitigating these risks doesn’t mean overnight independence from Chinese supply. It means building a portfolio of credible non-Chinese sources and understanding their timelines and bottlenecks. For antimony, Mandalay Resources’ Hillgrove project in Australia is one of the few near-term options. Its restart, targeted around 2026, could add roughly 1,500 tonnes per year of contained antimony, but is still navigating permitting and community-relations hurdles. Any slippage there directly prolongs global dependence on Chinese and Russia-adjacent material.

On tungsten, Almonty Industries’ Sangdong mine in South Korea is the pivotal non-Chinese asset. If it achieves its planned >5,000 t/year WO3 output and avoids extended labor or energy disruptions, Sangdong can meaningfully offset Chinese export tightening and provide secure feedstock for allied defense and tooling industries. In rare earths, Lynas’ Mt Weld remains the cornerstone non-Chinese source for light and some heavy REEs, while Neo Performance Materials and emerging North American separation plants aim to add dysprosium, terbium, yttrium and samarium streams in the second half of the decade.

For semiconductor inputs, AXT Inc. in the U.S. and European gallium and germanium refiners such as Umicore are the early anchors, although their combined capacities still cover only a fraction of current global demand. In battery materials, Syrah Resources’ Balama graphite operation in Mozambique, backed by downstream processing in the U.S. and Europe, is the main non-Chinese natural-graphite play with scale. Across these and similar projects, the pattern is consistent: if financing, permitting and infrastructure fall into place, they can collectively cover perhaps 20–30% of the projected deficits for the top six controlled materials by the late 2020s. For 2026, however, the realistic outcome is more modest: targeted risk reduction for the most exposed supply chains, not full insulation from Chinese policy decisions.