Industry Trends

Eu crma 2030 targets: why 10% extraction and 40% processing are so hard to hit

EU CRMA 2030 Targets: Ambition Collides With Supply-Chain Reality

Materials Dispatch cares about the Critical Raw Materials Act (CRMA) for one simple reason: every long-term supply-chain plan for batteries, wind, defense systems, aerospace alloys, and advanced manufacturing in Europe now hangs on a set of 2030 benchmarks that are mechanically elegant and operationally brittle. The regulation speaks the language of security and resilience; the projects on the ground speak the language of permitting delays, community pushback, power prices, and Chinese processing dominance.

Over the past decade, repeated disruptions in cobalt, rare earths, magnesium, gallium, and battery-grade lithium have re-wired risk perception among the industrial actors Materials Dispatch follows. Procurement teams that once trusted China-centric supply networks now face board-level pressure to demonstrate diversification, traceability, and alignment with EU industrial policy. The CRMA is the central reference text in that conversation, but its 10% extraction and 40% processing benchmarks are widely regarded in the field as structurally misaligned with geology, timelines, and economics.

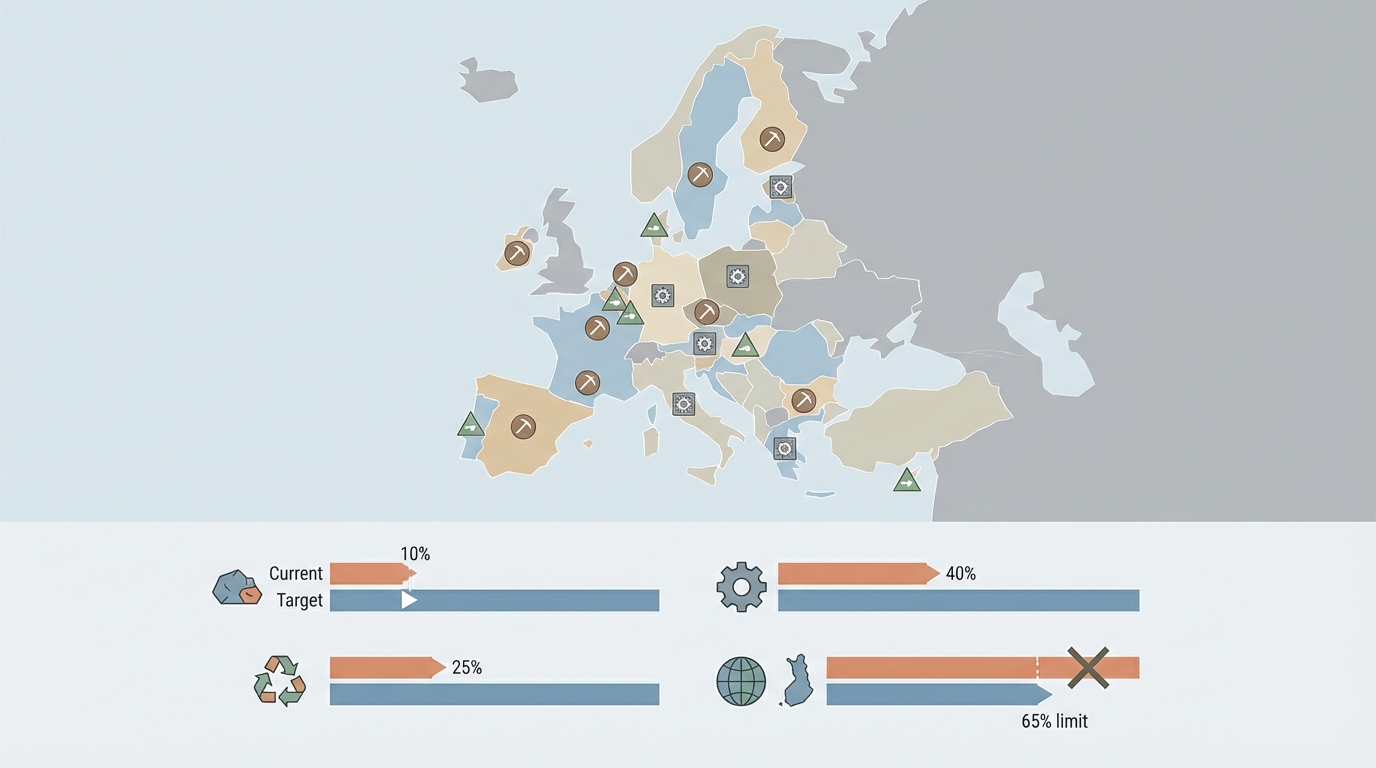

- Change: The CRMA fixes Union-wide 2030 benchmarks (10% extraction, 40% processing, 25% recycling, max 65% from any one third country) for 34 critical and 17 strategic raw materials.

- Scope: Targets are calculated as shares of EU annual consumption, linked to “strategic projects”, national exploration programmes, and diversification rules, but without automatic sanctions for non-compliance.

- Baseline: Current EU extraction of several strategic raw materials sits below 3% of consumption, with near-zero refining for some battery and magnet inputs, while China controls a dominant share of global processing.

- Operational reality: Long mine lead times, contested land use, high energy costs, and limited dedicated funding combine to make the 10% and 40% benchmarks highly challenging to reach by 2030.

- Reading limits: Market impacts, including possible price differentials for EU-bound material, remain scenario-based and highly uncertain, depending on future enforcement choices, project execution, and global geopolitics.

FACTS: CRMA Architecture, Baseline Capacity, and Implementation Status

CRMA 2030 Benchmarks and Governance Mechanics

The Critical Raw Materials Act, adopted in 2024 as Regulation (EU) 2024/1252, establishes a framework for securing supplies of 34 critical raw materials (CRMs) and a subset of 17 strategic raw materials (SRMs) deemed essential for the green and digital transition, as well as for defense and space applications.

By 2030, at Union level, the regulation sets non-binding benchmarks that:

- At least 10% of the EU’s annual consumption of each strategic raw material should be extracted within the Union.

- At least 40% of the EU’s annual consumption of each strategic raw material should be processed (refined or transformed into intermediate products) within the Union.

- At least 25% of the EU’s annual consumption of each strategic raw material should be covered by recycling from domestic waste streams.

- No more than 65% of the EU’s annual consumption of any strategic raw material should come from a single third country.

These benchmarks are calculated relative to EU consumption rather than absolute tonnage. Consumption estimates rest on demand projections across sectors such as batteries, permanent magnets, aerospace alloys, and high-performance electronics. The European Commission is tasked with compiling these projections and publishing regular assessments of dependency and progress.

To operationalise the targets, the CRMA introduces the concept of “strategic projects” in the EU or in partner countries, eligible for faster permitting timelines (in principle, 27 months for extraction projects and 15 months for processing and recycling projects) and enhanced administrative coordination. Member States are required to designate single points of contact (SPOCs) to manage these permits and to develop national exploration programmes for critical raw materials.

Importantly, the 10%/40%/25% benchmarks function as Union-wide planning signals rather than hard quotas. The regulation relies on monitoring, reporting, and coordinated action plans rather than automatic fines or trade measures in case of non-achievement.

Current Extraction and Processing Baseline in the EU

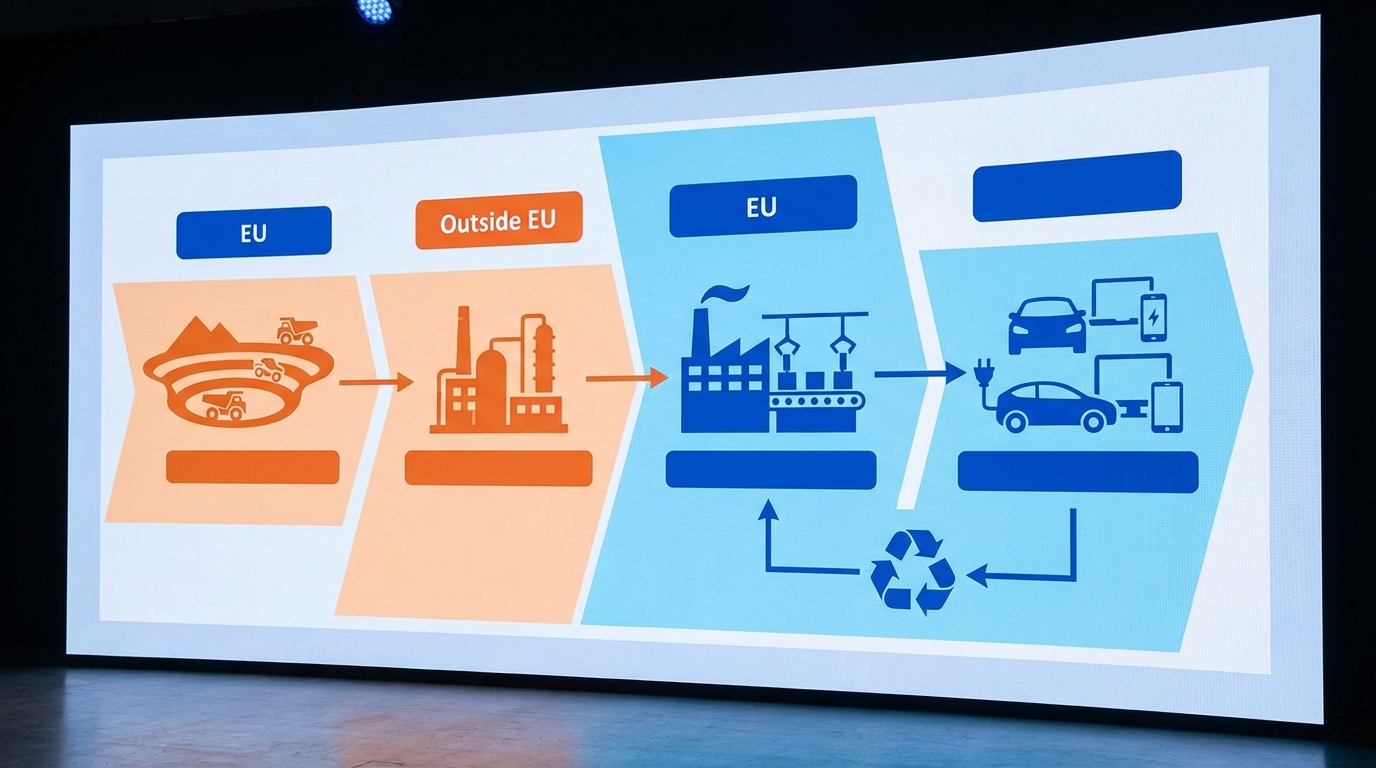

Audits by European institutions and technical agencies converge on a stark baseline: for several strategic raw materials, EU extraction covers only a low single-digit share of annual consumption, and in some cases virtually none. Lithium and rare earth elements (REEs) are prominent examples where domestic mine production is negligible, while cobalt extraction within the EU accounts for a small fraction of total use.

On the processing side-the conversion of concentrates or intermediates into battery-grade chemicals, alloys, or magnet materials-the EU position is even more constrained. For a number of key SRMs (including many light and heavy rare earths, battery-grade lithium chemicals, and gallium), refining is overwhelmingly concentrated outside the EU, with China holding a dominant share of global capacity that often exceeds well over half of world processing.

Existing EU processing facilities in areas such as nickel, cobalt, and certain rare earths operate under structural headwinds:

- Electricity prices in many Member States are significantly higher than in competing jurisdictions that host large hydrometallurgical and pyrometallurgical complexes.

- Plants frequently rely on imported feedstock, exposing operations to the same external supply risks the CRMA aims to mitigate.

- Some legacy facilities run below nameplate capacity or intermittently, reflecting both feedstock uncertainty and margin pressure.

Against this baseline, the 40% processing benchmark implies a steep ramp-up of domestic refining and intermediate manufacturing capacity from a low starting point, at a moment when several existing facilities are struggling to remain competitive.

Implementation: SPOCs, Exploration Programmes, and Strategic Projects

The CRMA requires each Member State to establish a competent authority and a single point of contact to coordinate permitting for strategic projects. It also mandates national programmes for the exploration and mapping of critical raw materials within their territory, aiming to improve geological knowledge and identify potential new projects.

Early implementation reports and Commission communications indicate an uneven start:

- In some Member States, SPOCs are already in place, with clear procedural timelines and dedicated staff; in others, institutional designation and resourcing are still in progress.

- Exploration programmes vary widely in scope and ambition, from relatively comprehensive updates of national geological surveys to limited pilot mapping efforts focused on a few regions.

- Only a modest number of projects have so far been flagged as candidates for “strategic” status, and several of them were already under development before the CRMA.

Permitting data from high-profile projects illustrates the challenge. A number of flagship mining and processing initiatives in Sweden, Finland, Portugal, Czechia, and elsewhere have spent many years in environmental impact assessment and public consultation phases, often facing litigation and strong local opposition. Even where the CRMA’s fast-track principles apply, they interact with existing environmental, water, and land-use legislation that can extend timelines well beyond the theoretical maximums stated in the regulation.

Illustrative Projects Shaping the Baseline

A non-exhaustive set of projects helps anchor the discussion:

- LKAB’s rare earth and phosphate discovery at Kiruna (Sweden) is widely cited as Europe’s largest known REE resource. It has the potential to underpin magnet supply for defense and electric vehicles but still faces extended permitting and complex social and environmental questions, including Indigenous rights concerns.

- Lithium projects in Portugal and the Czech Republic, such as the Barroso and Cinovec projects, illustrate both geological potential and strong community resistance, particularly around open-pit operations, water use, and landscape impact.

- Keliber in Finland represents a more advanced lithium project with integrated mining and conversion plans in a jurisdiction traditionally more supportive of mining, yet still dealing with grid, power, and permitting constraints.

- Umicore’s cathode material facilities in Finland and other battery precursor plants in the EU highlight that some midstream capacity exists, but current utilisation relies heavily on imported feedstock.

- Rare earth processing and magnet recycling initiatives such as Neo Performance’s Silmet plant in Estonia and HyProMag-linked pilots in continental Europe show early attempts to rebuild magnet value chains and recycling, often running at modest scale and facing feedstock insecurity.

These projects are central to any realistic path toward the 10% extraction and 40% processing benchmarks, yet most of them are either still in development or constrained by factors outside the CRMA’s immediate remit, such as national land-use plans, legal challenges, and energy system bottlenecks.

INTERPRETATION: Why 10% Extraction and 40% Processing Look Structurally Implausible

The 10% Extraction Benchmark: Geology, Timelines, and Social Friction

From a supply-chain viewpoint, the 10% extraction benchmark is less a gentle stretch target and more a structural cliff. Across interviews with miners, commodity traders, and downstream manufacturers, one phrase recurs with increasing frequency: “10% is fantasy.” That is not a claim that new mines are impossible in Europe; it is a recognition that geology, timelines, and social context do not align with a rapid, broad-based surge in domestic extraction.

Several structural constraints stand out:

- Lead times: For greenfield mines in complex jurisdictions, combined exploration, feasibility, permitting, financing, construction, and ramp-up phases frequently stretch into the decade-plus range. The CRMA fast-track provisions can shave administrative time but do not remove technical or legal complexities.

- Geology versus land-use: Some of the most promising lithium and rare earth occurrences in the EU sit under or next to protected landscapes, valuable agricultural areas, or culturally sensitive sites, making large-scale open-pit or tailings-intensive operations socially and politically contested.

- Permitting risk perception: Capital providers and boards have a clear memory of stalled or cancelled EU mining projects over the past 10-15 years. Even when geology is attractive, perceived permitting and litigation risk can redirect capital to lower-friction jurisdictions.

- Interaction with environmental policy: Parallel EU initiatives, including taxonomy rules and biodiversity strategies, introduce additional layers of scrutiny. In some cases, mining is treated as a necessary evil rather than a strategic industry, creating mixed signals for both national authorities and project sponsors.

Under these conditions, the 10% extraction benchmark appears structurally out of reach by 2030 unless a substantial share of the volume is delivered by brownfield expansions and a very small number of exceptionally large, fast-tracked projects in geologically favourable and socially more accepting regions. So far, the pipeline of such projects remains thin.

The 40% Processing Benchmark: Energy Economics and Feedstock Dependence

If 10% extraction is hard, 40% processing is harder. Here, the industrial feedback is even harsher. In off-record discussions, some processing executives describe the target in blunt terms as “40% is sabotage” – a shorthand for the perception that the benchmark ignores basic energy cost arithmetic and feedstock realities.

Key factors undermining the 40% processing goal include:

- Power prices and volatility: Energy-intensive refining steps such as roasting, leaching, solvent extraction, electrolysis, and high-temperature furnacing compete globally on a cost base that is heavily driven by electricity price and stability. Many EU jurisdictions sit at a clear disadvantage versus processing hubs with abundant low-cost power.

- Lack of local feedstock: Processing capacity is economically fragile when it depends almost entirely on imported concentrates. Without a credible ramp-up in domestic or closely allied raw material supply, standalone EU refining projects face both volume and margin risk.

- Technological lock-in elsewhere: China and a small set of other jurisdictions control not only capacity but also key process know-how, especially for complex separation flowsheets such as rare earth solvent extraction and advanced precursor manufacturing. Rebuilding this knowledge base in Europe is feasible but takes time, talent, and sustained commissioning cycles.

- Regulatory stacking: Processing plants must navigate industrial emissions rules, water and waste directives, and local planning and community processes, in addition to CRMA designation. These frameworks are individually justified but collectively slow and complex.

The result is a paradox: the CRMA seeks to incentivise EU processing, but the absence of sufficient domestic feedstock and the relative energy cost disadvantage push some existing and prospective projects toward underutilisation or relocation. Without parallel changes in power system design, raw material availability, or direct financial support, it is difficult to see how aggregate EU processing could credibly approach 40% of consumption for the most strategic materials within the 2030 horizon.

Benchmarks Without Teeth: Policy Signalling vs. Enforceable Commitments

A further structural weakness lies in the enforcement architecture. The CRMA benchmarks are framed as Union-wide objectives. The Commission will publish scorecards and may coordinate actions with Member States, but there is no automatic mechanism that forces additional extraction or processing if targets are missed.

Within industry circles, this has led to a sceptical reading of the regulation as, at least in part, “policy theatre” – strong ambition statements without the fiscal and administrative infrastructure required to deliver them. The absence, so far, of a large dedicated EU fund for critical raw materials, and the cautious stance of public lenders toward high-risk mining projects, reinforces this perception.

This does not mean the CRMA is irrelevant. It provides:

- A common language for discussing supply risk and dependencies at board and ministry level.

- A procedural framework for fast-tracking genuinely strategic projects.

- A legal basis for structured partnerships with third countries on critical raw materials.

But as long as the benchmarks are not underpinned by binding national allocations, substantial shared financing, or direct demand-side measures, they function more as directional beacons than as enforceable constraints on market behaviour.

System-Level Implications: Chronic Tightness and Fragmented Responses

If the 10% extraction and 40% processing benchmarks are not met-and on current trajectories that is the most realistic scenario—the practical consequence is not a sudden collapse of supply but a structurally tight and politically exposed system.

Several conditional outcomes follow:

- Higher supply risk for EU-based manufacturing: Battery plants, magnet producers, and aerospace alloy makers in the EU remain heavily dependent on external supply chains, particularly Chinese processing. That makes them more vulnerable to export restrictions, quota shifts, diplomatic tension, and logistical disruptions.

- Potential regional price differentials: In stress scenarios where EU import diversification is limited, a premium for EU-delivered material relative to other regions is plausible, particularly for SRMs with high concentration of supply and processing. Estimates of how large such differentials might be vary widely and depend on assumptions about demand growth, Chinese policy, and the pace of new non-EU projects.

- Acceleration of non-EU partnerships: In practice, many EU industrial actors are already deepening relationships with producers in countries such as Australia, Canada, Norway, the United States, and selected African and Latin American jurisdictions. The CRMA’s partnership provisions formalise part of this trend but do not originate it.

- Uneven geography of resilience: Nordic countries with hydropower, active mining traditions, and nascent battery clusters (e.g., Sweden and Finland) are better placed to host integrated value chains. Other Member States may lean more heavily on imports and high-value downstream activities.

- Growth of stockpiling and long-term contracting: In defense and certain civil sectors, there is already movement toward building physical buffers and securing long-horizon supply agreements for the most critical SRMs, even before CRMA benchmarks bite.

Across all these dimensions, the CRMA acts less as a driver and more as a codifier of a trend that supply-chain professionals had already internalised after the rare earth, cobalt, and magnesium episodes of the past decade: dependence on a single dominant processing hub is a structural risk that boards can no longer ignore.

WHAT TO WATCH: Regulatory and Industrial Weak Signals

Several classes of indicators will determine whether the gap between CRMA ambition and reality narrows or widens over the rest of this decade:

- Permitting timelines for flagship projects: Actual time-to-decision for high-profile mining and processing projects in Sweden, Finland, Portugal, Czechia, and other Member States will show whether the fast-track mechanisms meaningfully compress lead times or remain largely theoretical.

- Activation and resourcing of national SPOCs: The staffing levels, legal authority, and cross-ministry coordination capacity of single points of contact will indicate whether Member States treat CRMA permitting as an industrial priority or as another administrative obligation.

- Concrete EU and national funding vehicles: The emergence (or absence) of a sizeable EU-level fund, targeted state aid schemes, or dedicated mandates for public banks toward critical raw materials will shape how many projects reach final investment decision.

- Chinese export controls and quota changes: Adjustments in China’s quotas or licensing regimes for rare earths, graphite, gallium, germanium, and other SRMs will directly test the resilience of EU supply chains and the credibility of diversification efforts.

- Utilisation rates and closures in EU processing: Operating data from existing refineries, cathode material plants, and magnet facilities—particularly those exposed to high power prices—will act as a barometer for the feasibility of sustaining and expanding processing capacity in the EU.

- Recycling performance against the 25% target: Real recovery rates for cobalt, nickel, lithium, and rare earths from end-of-life batteries, magnets, and industrial scrap will show whether recycling can materially offset extraction and processing shortfalls.

- Defense and EV-sector procurement behaviour: Moves toward strategic stockpiles, long-term sourcing alliances, and tighter supplier qualification standards in defense, automotive, and high-tech sectors will reveal how seriously industrial actors internalise CRMA-related supply risk.

- Taxonomy and environmental rule adjustments: Any changes to the EU sustainable finance taxonomy or environmental permitting guidance that explicitly treat certain mining and processing projects as enabling activities for the transition would signal a recalibration of the policy balance between protection and extraction.

Conclusion

The CRMA has put numbers—10% extraction, 40% processing, 25% recycling, and a 65% dependency ceiling—on concerns that supply-chain teams had already started to price in after a decade of raw material shocks. On the evidence currently available, those extraction and processing benchmarks look structurally implausible for 2030 in most strategic raw materials, given the interaction of geology, permitting, energy costs, and global competition.

That does not make the regulation irrelevant; it forces uncomfortable conversations inside companies and ministries about where and how to accept the impacts of mining and refining, and what level of dependence on external processing hubs remains tolerable. Over the coming years, the story will be written less by headline benchmarks and more by permitting files, power contracts, community hearings, and quiet changes in sourcing patterns. Materials Dispatch will continue active monitoring of regulatory and industrial weak signals that will determine whether CRMA evolves into a genuine resilience framework or remains largely symbolic.

Note on Materials Dispatch methodology Materials Dispatch cross-references official regulatory texts and communications from EU institutions with project-level reporting, technical literature, and operational disclosures from mining, processing, and manufacturing firms. This is complemented by continuous monitoring of end-use specifications in sectors such as batteries, wind, aerospace, and defense, to assess how regulatory targets intersect with real-world material performance requirements and supply-chain configurations.