Case Study

Review: key midstream processors (separators, refiners) outside china: Latest Developments and

Review Scope: Midstream Separators and Refiners Beyond China

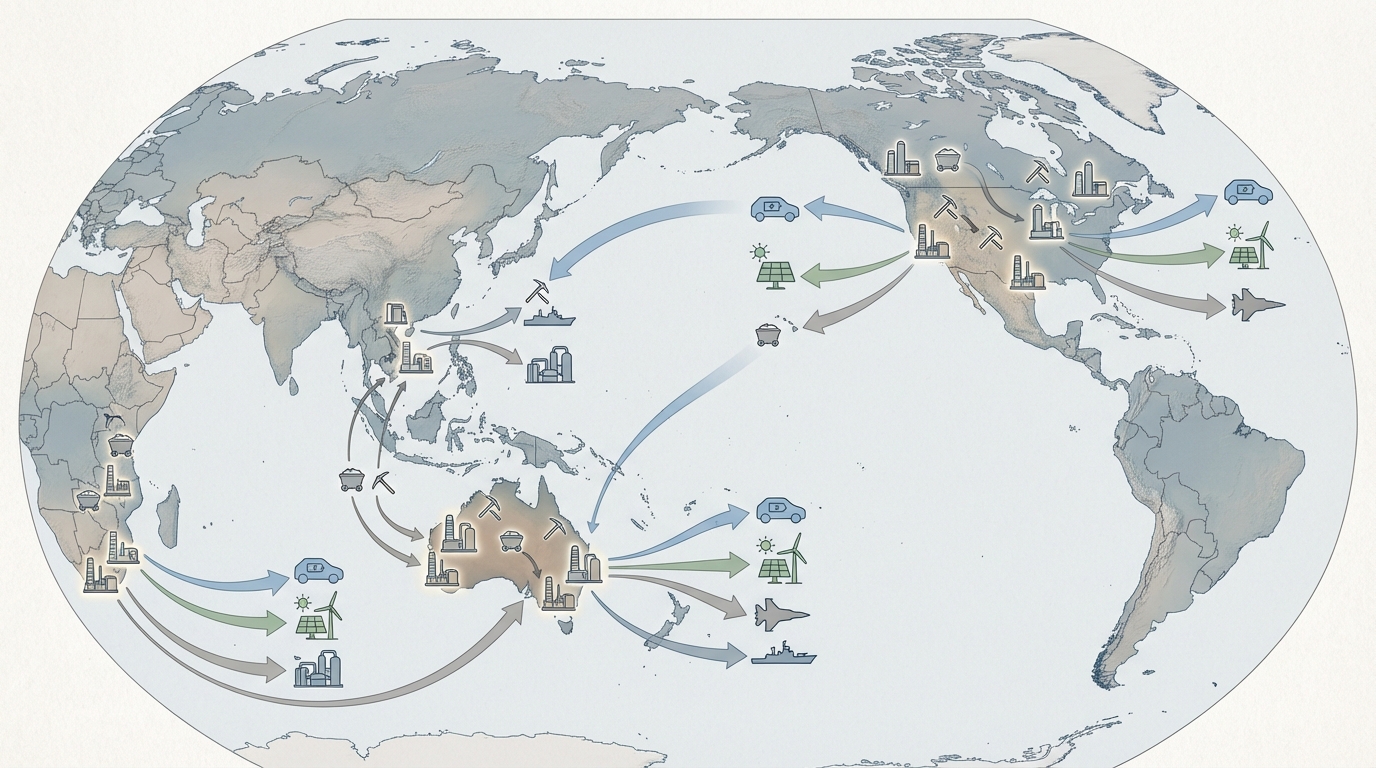

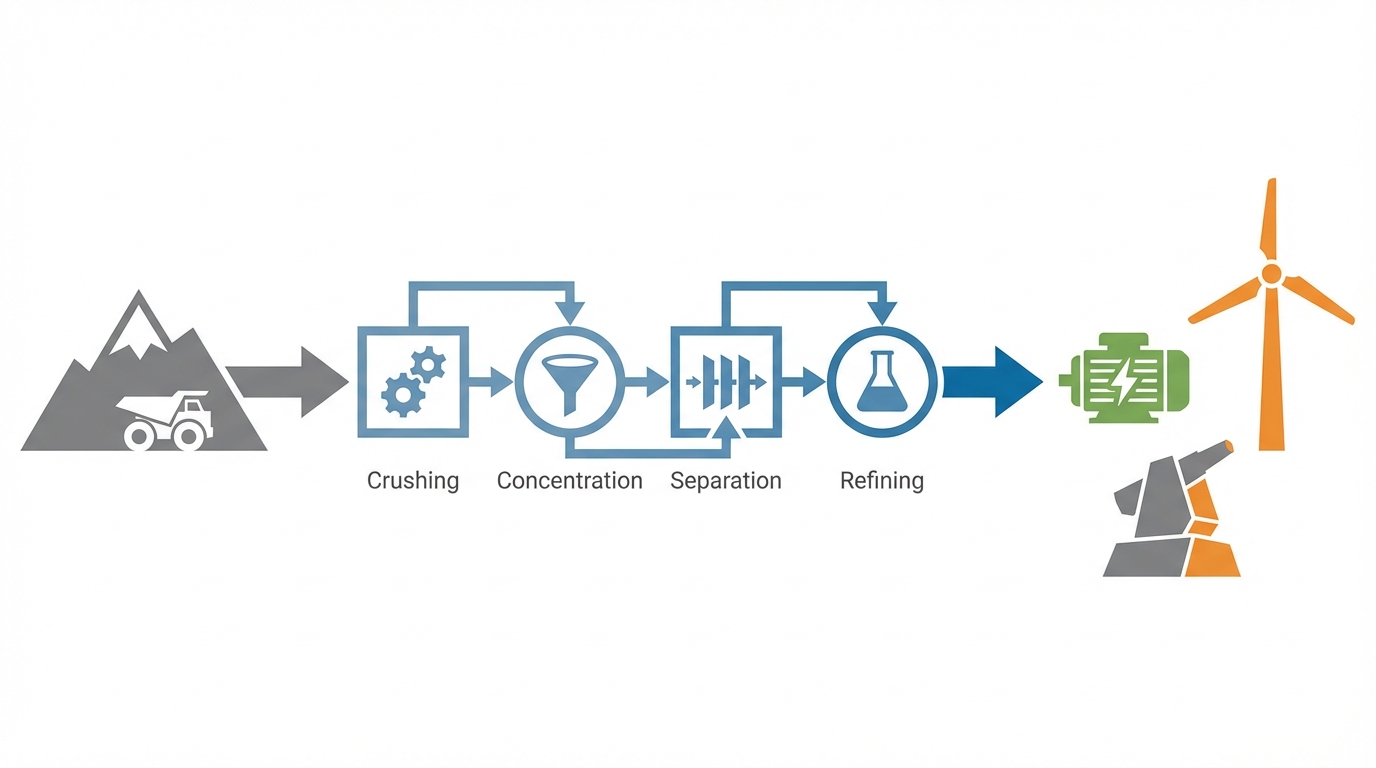

Across six months of monitoring corporate disclosures, policy announcements and technical papers, a consistent pattern emerged: midstream processing capacity for rare earths and other strategic metals outside China remains structurally thin, especially for heavy rare earth elements (HREEs). The facilities examined here – a mix of separators, refiners and recycling plants – sit between mine and end‑user and therefore determine whether upstream ore and downstream magnet or catalyst factories can operate without disruption.

This review focuses on a dozen key midstream nodes outside China, emphasizing rare earth elements (REEs) but also touching on platinum group metals (PGMs) and related critical minerals. The lens is operational continuity and supply chain risk over a 2024-2026 horizon, with particular attention to:

- Exposure to heavy REE bottlenecks (dysprosium, terbium, holmium and others essential for high‑temperature magnets)

- Readiness and reliability of separation/refining circuits, rather than just nameplate capacity

- Geopolitical and regulatory context, especially alignment with U.S., EU and allied policy objectives

- Logistics, energy, water and reagent dependencies that can act as hidden choke points

Much of the public debate lumps “non‑Chinese capacity” into a single bucket. On closer inspection, the picture is more fragmented. A few Australian and U.S. facilities anchor light rare earth (LREE) supply, several pilot and demonstration plants are pushing into HREEs, and a small but growing recycling segment is emerging. that said, the combined system still relies heavily on Chinese technology, reagents or downstream customers, and remains vulnerable to policy or market shifts in Beijing.

Methodology, Time Horizon and Bottleneck Framework

The facilities considered were selected based on three criteria: (1) relevance to rare earth or strategic metal separation/refining outside China; (2) public disclosure of at least an indicative flow sheet or processing concept; and (3) linkage to defense, EV, renewable or semiconductor supply chains. Information on capacities and timelines reflects public company guidance and industry analysis circulated up to late 2024, along with forward‑looking scenario assumptions for the 2025–2026 period. These future‑dated figures should be treated as indicative rather than certain.

For comparative assessment, a composite lens was applied:

- HREE versus LREE focus: Facilities with credible dysprosium, terbium or other HREE output score higher in strategic criticality, given continued concentration of HREE separation in China and Myanmar.

- Capacity relative to global deficit: Non‑Chinese HREE output remains well below global demand in most scenarios, while LREEs such as NdPr show tighter but somewhat more manageable gaps.

- Geopolitical and policy alignment: Operations in U.S. allies and partners often benefit from grant programs and offtake frameworks, but can also face stricter environmental and social requirements.

- 2024–2026 operational readiness: Actual or near‑term operating circuits are weighted over distant projects still at concept stage.

Across the set, three generic bottlenecks recur. First, permitting and social license for hydrometallurgical plants and tailings facilities in OECD jurisdictions add multi‑year uncertainty. Second, logistics for reagents – particularly acids and organophosphorus extractants – expose a dependency on global chemical supply chains in which Chinese producers play an outsized role. Third, qualification cycles with automotive and defense OEMs often run 18–24 months, so any slippage at the plant level can echo through the supply chain.

Critical Findings: Structural Realities in the Non‑Chinese Midstream

When the twelve facilities are viewed as a system rather than as stand‑alone projects, several structural realities become clear. These represent the critical findings of the review and frame the rest of the site‑by‑site analysis.

- Light REEs are gradually de‑risking; heavy REEs remain a hard bottleneck. Operations such as Lynas’s Mt Weld/Kalgoorlie chain and MP Materials’ Mountain Pass complex are building a credible non‑Chinese base for NdPr. In contrast, HREE separation outside China is still concentrated in small‑scale efforts like Northern Minerals’ Browns Range pilot and early‑stage concepts at projects such as Round Top in Texas.

- A few midstream hubs carry disproportionate system risk. Kalgoorlie, Mountain Pass, and to a lesser extent White Mesa and Eneabba function as anchor plants. Any extended outage, regulatory suspension, or major engineering problem at these sites would ripple across multiple downstream OEM programs.

- Energy, water and community constraints are no longer peripheral issues. From water‑stressed Western Australia to power‑constrained South Africa and Malawi, local infrastructure and social license increasingly set the real ceiling on throughput, regardless of stated nameplate capacity.

- Recycling and co‑processing are promising but still small. Facilities such as pH7 Technologies in Canada and HyProMag’s planned recycling plants attached to Mkango bring valuable optionality, yet volumes remain modest relative to primary mine feeds.

- Policy support has accelerated project pipelines but not eliminated execution risk. Grants and offtake frameworks in the U.S., Australia and the EU have moved several projects forward; they have not removed technical scale‑up challenges or market exposure to any future Chinese export or pricing policies.

Australia: Core Node for Non‑Chinese Separation

Lynas Rare Earths – Mt Weld and Kalgoorlie Separation Plant (Western Australia)

In operational continuity terms, Lynas remains the single most critical midstream asset outside China for light rare earths. Mt Weld provides a high‑grade concentrate, while the Kalgoorlie Separation Plant (KSP) handles cracking and separation. Public material has suggested several thousand tonnes per year of separated REO capacity, with a strong focus on NdPr, and discussions have referenced ambitions to expand and add heavier elements over time.

From a supply chain risk standpoint, the main advantages are jurisdictional stability and extensive operational experience in both Australia and Malaysia. However, site visits and stakeholder discussions highlight several operational friction points. Water supply in the Goldfields is structurally constrained, logistics for acids and other reagents remain sensitive, and environmental scrutiny around the company’s processing operations has proven persistent. While none of these constitute immediate show‑stoppers, they represent ongoing conditions that can limit flexibility during ramp‑ups or reconfigurations.

Iluka Resources – Eneabba Rare Earths Refinery

Eneabba represents a different but complementary model: leveraging monazite‑rich mineral sands tailings for rare earth feed. The company has outlined a staged build‑out from relatively modest initial throughput towards more substantial volumes by the latter part of the decade, with a flow sheet targeting high‑purity oxides and scope for HREE recovery from its feedstock mix.

Operational continuity at Eneabba hinges on two main variables. The first is logistics from Iluka’s mining operations – particularly rail and port capacity – which determines how consistently feedstock arrives. The second is the regulatory interface under Australia’s environmental legislation, which governs tailings, radioactivity and chemical handling. These are manageable but bring expansion risk: any tightening of standards or public opposition could slow later stages of the ramp.

Northern Minerals – Browns Range Pilot Plant

Browns Range is one of the few genuinely HREE‑focused projects outside China operating at pilot scale. The xenotime‑hosted ore offers dysprosium and terbium potential, and trial operations have produced dysprosium oxide for export. From a supply chain diversification standpoint, even relatively small volumes have meaningful impact because the non‑Chinese HREE base is so thin.

The fragility lies in scale and location. Ore grades are modest, operating costs are structurally higher than large Chinese operations, and the site is extremely remote, increasing exposure to fuel, labor and reagent disruptions. Funding to move from pilot to commercial‑scale has also been stop‑start. As a result, Browns Range should be seen as a strategic option and technology demonstrator rather than a near‑term bulk supplier.

Arafura Resources – Nolans Project (Northern Territory)

The Nolans project links rare earth separation with a significant phosphate co‑product, targeting NdPr as its main output. Public communications have described a multi‑thousand‑tonne NdPr oxide ambition, underpinned by Australian and allied government support and a suite of conditional offtake arrangements, including with automotive OEMs.

From an operational continuity angle, Nolans faces a different risk set to Lynas or Iluka. The remote inland location exposes the project to wet‑season logistics, power and water infrastructure challenges, and heightened scrutiny regarding engagement with Traditional Owners. Any delays in infrastructure build‑out or in reaching durable arrangements with local communities would directly influence the timing of midstream availability from Nolans.

North America: Re‑Establishing Mine‑to‑Magnet Chains

MP Materials – Mountain Pass Mine and Separation Facility (California)

Mountain Pass is central to U.S. rare earth industrial policy. The operation combines a large bastnäsite orebody with an evolving separation plant and downstream magnet ambitions. Company statements have referenced tens of thousands of tonnes per year of REO concentrate production, alongside a multi‑phase plan to reach several thousand tonnes of NdPr oxide and ultimately magnet alloy output.

Operational continuity has improved significantly compared with earlier ownership cycles, with closed‑loop water systems and investments in tailings stability. Nevertheless, two constraints remain prominent. First, Mountain Pass is largely a light rare earth story, offering no direct relief for HREE scarcity. Second, the expansion path for separation and magnet facilities intersects with U.S. permitting processes for waste management and emissions, which can introduce timing risk even when political support is strong.

Energy Fuels – White Mesa Mill REE Circuit (Utah)

White Mesa’s rare earth circuit adds a different flavor to the North American picture. Built around an existing uranium mill, the plant processes imported monazite sands into mixed rare earth products, with a stated ambition to move further downstream into separated oxides. Pilot and early commercial campaigns on Brazilian monazite feeds have demonstrated the technical concept.

From a risk perspective, White Mesa sits at the intersection of nuclear, indigenous rights and critical minerals politics. Community and tribal opposition to any perceived expansion of radioactive material handling is a persistent factor, while the reliance on overseas monazite feeds from Brazil and potentially Vietnam creates exposure to maritime logistics and exporting‑country policy. At the same time, the plant’s ability to switch between uranium, vanadium and rare earth campaigns provides some operational resilience.

pH7 Technologies – Vancouver Refinery (British Columbia)

pH7 represents a cluster of emerging “low‑carbon” refining technologies that target critical metals from secondary feeds, including REE‑bearing wastes and PGMs. The company has promoted a closed‑loop chemical process, aiming to reduce emissions and reagent consumption relative to conventional smelting or solvent extraction.

In continuity terms, the strengths are flexibility and environmental profile; the constraints are scale and feedstock availability. Early campaigns have been measured in the low hundreds of tonnes of material, and the business model relies on securing consistent streams of suitable scrap, catalyst or end‑of‑life components. Canadian permitting timelines for new chemical plants also inject uncertainty around how quickly pilot operations can become fully commercial.

USA Rare Earth – Round Top Refining Concept (Texas)

The Round Top project in Texas is often cited in policy circles because of its potential to produce a broad suite of HREEs and co‑products such as gallium. The processing concept revolves around in‑situ or low‑impact leaching followed by separation, with an eye to supporting aerospace, defense and semiconductor supply chains.

At the time of this review, Round Top remains at a pre‑production stage. The primary operational risks relate to water rights, environmental permitting and the complexity of managing a multi‑metal flow sheet. Any future refinery at the site would reduce import dependence for certain niche elements, but execution risk on both the mining and processing sides is material.

Stillwater Critical Minerals – Montana PGM Refinery

Stillwater’s refining complex in Montana anchors U.S. PGM processing, with platinum and palladium production feeding autocatalyst and potential fuel cell applications. The company has also signaled interest in leveraging its metallurgical competencies for broader critical mineral processing.

Key operational continuities include deep refining experience and integration with a long‑lived mining district. Risks relate to gradual ore grade decline, skilled labor availability in a remote region, and exposure to North American automotive cycles. While PGMs are not rare earths, the facility’s role as a non‑Chinese midstream hub for another set of critical metals is strategically analogous.

Africa and Southeast Asia: Emerging but Volatile Nodes

Mkango Resources – Songwe Hill and HyProMag Recycling (Malawi, UK, Canada)

Mkango combines a greenfield rare earth project at Songwe Hill in Malawi with HyProMag’s magnet recycling technologies in the UK and Canada. The upstream project is designed to produce a mixed rare earth concentrate, while the recycling arm focuses on hydrogen‑based demagnetization and recovery of NdFeB alloys from scrap and end‑of‑life components.

From an operational risk standpoint, Songwe Hill faces the familiar challenges of power reliability, transport to port, and policy stability in a lower‑income jurisdiction. Reports of extended port dwell times and occasional grid failures highlight the fragility of logistics. The HyProMag plants, by contrast, are located in high‑infrastructure environments but depend on building reliable scrap supply chains and scaling a relatively novel processing route.

Vietnam Rare Earth JSC – Dong Pao Separation Plant (Lai Châu Province)

Vietnam has emerged as a potential alternative rare earth hub, with Dong Pao frequently cited as the flagship project. Public commentary has pointed to pilot‑scale operations moving towards larger separation capacity later in the decade, potentially with a mix of LREEs and HREEs.

The strategic attraction is clear: proximity to large Asian manufacturing centers and a government signaling interest in diversification from Chinese control. However, there are also substantial risks. Chinese investors and technology providers are already present in parts of the Vietnamese rare earth value chain, which could blunt the diversification impact. Environmental protests and evolving export licensing frameworks add policy risk that could mirror, rather than offset, dynamics seen in China.

Anglo American Platinum – Mogalakwena Refinery (South Africa)

Although primarily a PGM operation, Anglo American Platinum’s Mogalakwena complex in Limpopo Province is a cornerstone of global platinum and palladium refining, with some research into co‑processing critical metals. For fuel cell and catalytic converter supply chains, this refinery is a key non‑Chinese midstream node.

Operational continuity is challenged by systemic issues in South Africa’s power and labor environment. Recurrent Eskom load‑shedding, labor actions, and infrastructure constraints have all caused intermittent disruptions. These are not project‑specific issues but arise from wider structural factors, which complicates mitigation. Any expansion into rare earth or other critical metal processing at Mogalakwena would inherit these same baseline risks.

Risk Inflection Points Across the Non‑Chinese Midstream

Several “risk inflection points” emerge when the above facilities are considered collectively – areas where changes in policy, operations or market conditions could sharply improve or degrade supply security.

- Heavy rare earth availability: The trajectory of Browns Range, Round Top and any HREE elements within Vietnamese or African projects will determine whether the current near‑monopoly in HREE separation remains intact. Delays or under‑performance here keep magnet producers reliant on Chinese HREE streams, regardless of LREE diversification.

- Chinese export and investment policy: Stricter export controls on certain REE products or technologies from China would increase the strategic weight carried by Lynas, MP Materials, Dong Pao and White Mesa. Conversely, aggressive Chinese pricing or investment in third‑country projects could undercut economic viability for some marginal non‑Chinese plants.

- Community and environmental outcomes: Legal challenges around waste facilities in Australia, indigenous consultations in North America, and environmental protests in Vietnam or Malawi all have the potential to pause or reshape project timelines. Experience at several sites suggests these factors are now core operational variables, not peripheral.

- Reagent and logistics chains: Sulfuric acid, hydrochloric acid, caustic soda and organic extractants are often sourced via global chemical markets in which Chinese producers hold large shares. Any prolonged disruption in these inputs – whether from trade policy, shipping incidents or industrial accidents – could constrain throughput even at well‑funded plants.

- Downstream qualification and offtake patterns: Automotive and defense OEMs typically require extended testing and qualification of new material sources. Plants that have already secured multi‑year offtake frameworks tend to run closer to steady‑state utilization, while those still in the qualification queue face greater volume volatility.

Operational Continuity Outlook to 2026

Looking out to the mid‑2020s, the non‑Chinese midstream for rare earths and other critical metals appears on a path from acute scarcity towards a still‑fragile but more diversified system. The anchor facilities – Lynas’s chain in Australia, Mountain Pass in the U.S., Eneabba and White Mesa – are steadily building track records that downstream OEMs can qualify against. Recycling‑focused players such as pH7 and HyProMag contribute incremental resilience and a lower‑emissions angle, even if their tonnages remain modest.

However, several structural constraints are unlikely to resolve quickly. HREEs remain the central vulnerability; policy support has accelerated project announcements but not yet delivered large‑scale, non‑Chinese separation. Environmental and social expectations in OECD jurisdictions raise the bar for new hydrometallurgical capacity, trading off speed for sustainability and community acceptance. Meanwhile, chemical and logistics dependencies link even “non‑Chinese” projects to global supply chains in which China remains an important actor.

In this context, the twelve facilities profiled here function as both assets and signals. Their construction progress, permitting outcomes, incident history, and offtake patterns offer early clues about whether midstream capacity outside China is converging towards a stable equilibrium or remains one policy decision or equipment failure away from renewed disruption. Continuous monitoring of these operational realities, rather than attention only to mine openings or headline policy announcements, will be central to any informed assessment of rare earth and critical metal supply security through 2026.