Industry Trends

Why ‘friend‑shoring’ is harder than it looks in critical minerals

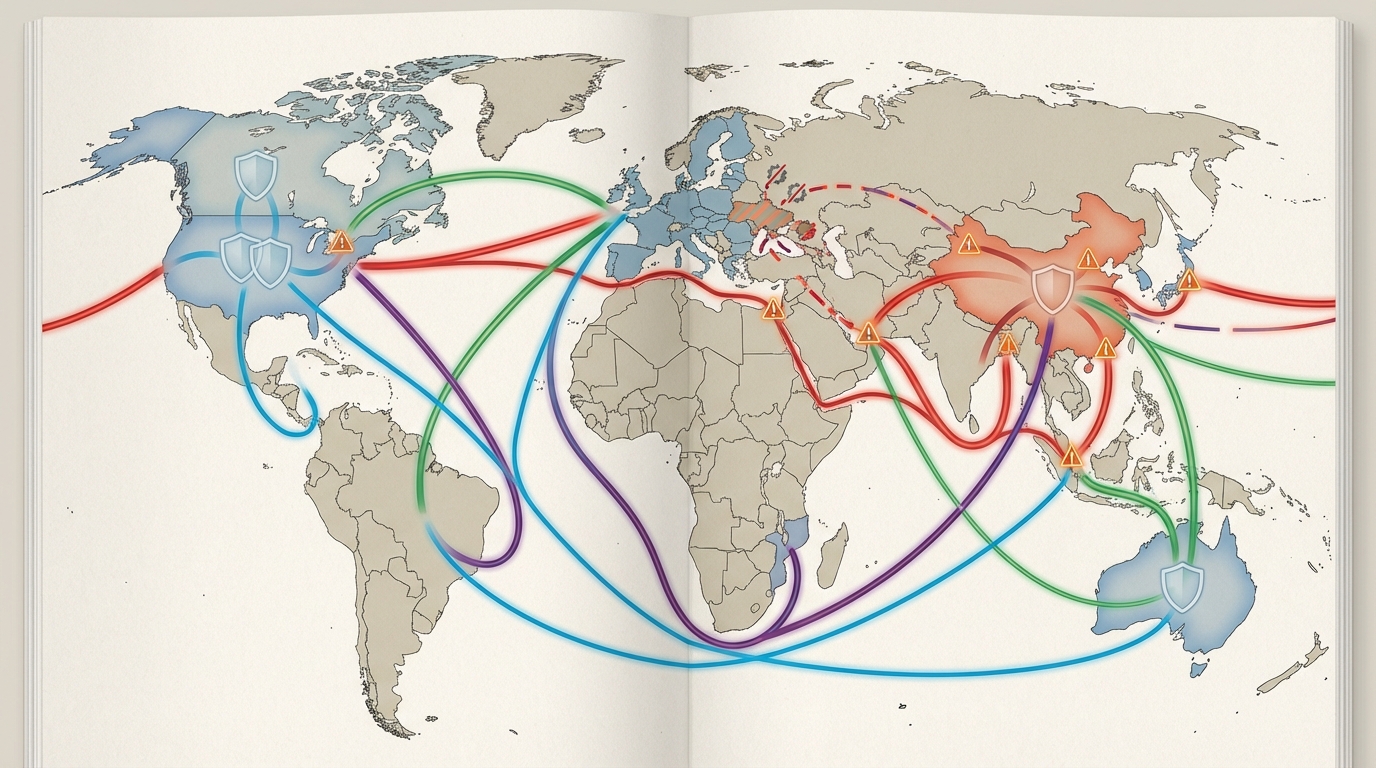

Materials Dispatch cares about friend‑shoring in critical minerals for very practical reasons: procurement teams are trying to secure long‑life supply for defense, energy and electronics programs while navigating sanctions lists, origin rules, and fast‑moving trade measures. Over the past three years, rare earth and battery‑metal sourcing reviews have been repeatedly blown off course by new tariffs between allies, carbon border rules, export controls, and project delays. Each of these episodes has underlined the same blunt reality: the political story about “friends” does not match the physical and regulatory structure of critical‑mineral supply.

When neodymium‑praseodymium (NdPr) prices swing roughly 25% in a single quarter on the back of Chinese export‑control briefings, when a supposedly friendly supplier suddenly falls under a new tariff regime, or when a flagship refinery overruns capital expenditure by 40%, the elegant speeches about allied resilience give way to crisis calls between procurement, compliance, and program managers. This briefing unpacks why friend‑shoring in critical minerals is structurally harder than it looks, and how recent rules, timelines, and capacity data point to a high‑friction decade ahead.

Key Points

- Friend‑shoring strategies run into China’s entrenched dominance in refining and magnet production, where processing shares of roughly 70-95% and separation capacity above 200,000 tonnes per year collide with much smaller allied projects.

- Recent measures by allies themselves-US Section 301 tariffs on Canadian and Mexican critical minerals, EU CBAM implementation, proposed Canadian export levies, and Japanese stockpile mandates-fragment what is supposed to be a unified “friends” bloc.

- Regulatory timelines (tariffs, tax credits, export controls) are out of sync with multi‑year project build‑outs, typical capital expenditure overruns of 30-40%, and permitting delays, creating a persistent gap between policy ambition and physical supply.

- Defense and clean‑energy supply chains face different cost and risk tolerances; early evidence points toward an emerging segmentation, with defense willing to pay security premia and civilian energy chains remaining deeply exposed to Chinese flows.

- Interpretation of these dynamics remains conditional: actual outcomes will hinge on how specific measures are implemented in 2025-2028, how quickly allied refining projects overcome execution risks, and how far China pushes export‑control leverage.

FACTS: Structures, Rules, Dates and Capacities

China’s structural position in critical‑mineral processing

Across multiple critical materials, China holds a dominant share of mid‑stream processing and refining rather than just upstream mining. Public data from geological surveys and industry bodies describe approximate Chinese shares of:

- Roughly 70–95% of global refining and processing in key rare earth elements (REEs) and permanent magnet materials.

- A very large majority of oxide separation capacity, with Chinese rare‑earth separation estimated above 200,000 tonnes per year, compared with targeted capacities in the low thousands of tonnes per year for leading allied projects.

- High shares in graphite anode materials and intermediate magnet production, even where some mining occurs in allied jurisdictions.

US minerals data indicate that the United States remains fully import‑reliant for more than a dozen critical minerals, including several heavy rare earths such as dysprosium (Dy) and terbium (Tb). Non‑Chinese capacity for heavy rare earth separation is currently limited and highly concentrated.

Key allied projects and capacities

A series of allied projects has been announced or advanced with explicit friend‑shoring goals:

- Lynas Rare Earths and Iluka Resources are developing the Eneabba refinery in Australia, targeting around 1,500 tonnes per year of separated rare earths by the mid‑2020s. Industry coverage in early 2026 highlighted delays and cost pressures.

- Arafura Resources’ Nolans project in Australia is designed to produce approximately 4,200 tonnes per year of NdPr‑equivalent, with legal challenges and environmental litigation reported in 2026.

- MP Materials is expanding integrated rare‑earth separation and magnet capacity in North America, including a magnet facility in Fort Worth that is reported to target around 1,000 tonnes per year of NdFeB magnets from late 2026.

- Neo Performance Materials and Vital Metals are developing rare‑earth downstream capacity in Canada, including oxide and potential magnet‑grade material production.

- Mountain Pass in the United States continues to operate as a major rare‑earth concentrate producer, with reported output around 45,000 tonnes per year of rare‑earth oxide equivalent.

- On the battery‑metal side, BHP’s Nickel West operations in Australia produce on the order of tens of thousands of tonnes per year of nickel, and are often cited in discussions about low‑carbon nickel supply to allies.

Taken together, these projects do not yet approach the processing scale that China has built over several decades. Many remain in ramp‑up or development phases, with commissioning dates extending into the second half of the 2020s.

Major allied policy measures affecting friend‑shoring (2024–2027)

Alongside project announcements, a dense layer of trade, industrial and security policy has emerged among “friendly” jurisdictions. Several measures are directly relevant to critical‑mineral friend‑shoring:

- US Section 301 tariffs on Canadian and Mexican critical minerals (effective 2025). In early 2025, US authorities announced that certain critical‑mineral imports from Canada and Mexico would face 25% tariffs under Section 301, with implementation from 1 January 2025. Public justification framed the move as a national‑security and domestic‑processing measure, even though both partners are parties to the US‑Mexico‑Canada Agreement (USMCA).

- EU Carbon Border Adjustment Mechanism (CBAM) rollout (2026–2027). The European Union’s CBAM entered a transitional reporting phase mid‑decade, with full financial adjustment scheduled to start in 2027. While initial sectors were limited, policy and market analysis in 2025–2026 described significant implications for high‑carbon nickel and stainless‑steel supply into Europe, with estimates of substantial cost uplifts (often cited in the 20–30% range) for higher‑emission routes.

- Chinese export‑control signalling on rare earths and magnets (post‑2026). State‑linked commentary in early 2026 indicated that previously relaxed controls on dual‑use rare‑earth products and magnets could be tightened again after November 2026. Earlier export‑control moves had already triggered price and availability volatility in NdPr and related materials.

- Australia’s Critical Minerals Strategy 2023–2030. Australia’s strategy sets explicit targets for increasing domestic processing, with public statements describing objectives for a majority share (for example, 60%) of critical‑mineral processing to occur onshore by the middle of the decade. A Critical Minerals Accelerator stream was introduced to fast‑track approvals, though projects such as Nolans still encountered legal and community challenges.

- 2026 Critical Minerals Ministerial and FORGE forum. A ministerial meeting in February 2026, involving the United States and several allied resource holders, launched the FORGE forum, oriented around joint stockpiling, co‑financing of strategic projects, and information‑sharing on critical‑mineral security.

- “Project Vault” US–Australia stockpiling initiative. Also in early 2026, reporting described a bilateral stockpiling program, Project Vault, intended to secure rare earths and related materials for defense uses. Financing and construction were reportedly affected by a capital‑expenditure overrun on the order of 40% relative to initial estimates.

- US Inflation Reduction Act (IRA) Section 45X implementation. Treasury guidance in early 2026 clarified that advanced manufacturing production credits for critical‑mineral processing (often referred to as Section 45X credits) would expand from 2026, with a 10% credit level cited for eligible critical‑mineral processing. Eligibility was tied to domestic or free‑trade‑agreement (FTA) partners, leaving some “friendly” but non‑FTA states-such as Ukraine—outside the regime pending review.

- Japan’s rare‑earth stockpile requirements (effective April 2026). Japan moved to formalise minimum stockpile days for heavy rare earths used in defense magnets, such as Dy and Tb, with a 60‑day target referenced. Sourcing plans highlighted reliance on non‑Chinese supply from entities such as Lynas’ Malaysian operations and Australian projects.

- Canada’s proposed export levy on rare‑earth concentrates (2026). In response in part to upstream‑only extraction patterns, Canadian policymakers discussed a proposed 5% levy on unprocessed rare‑earth concentrate exports in 2026, with indications that defense‑related offtake could receive exemptions. This would coexist with, and potentially interact awkwardly with, US tariff policy.

Documented supply disruptions and legal constraints

Several concrete disruptions shaped allied thinking on friend‑shoring:

- Russian aggression against Ukraine disrupted titanium feedstock and graphite projects in that country, including deposits identified in US‑Ukraine critical‑minerals cooperation documents. Energy infrastructure attacks and logistics constraints led to repeated interruptions in ore and concentrate shipments.

- Australian operations in multiple commodities, including nickel and gold‑PGMs, experienced weather‑related shutdowns and transport interruptions from floods and cyclones in 2025–2026.

- Legal challenges from Indigenous and local communities in Australia, including litigation targeting the Nolans rare‑earth project, resulted in permitting delays measured in many months.

- NdPr and broader rare‑earth spot markets saw marked volatility; one widely cited example was a roughly 25% swing in NdPr spot prices during the first quarter of 2026 associated with renewed Chinese export‑control commentary.

Industry and project‑finance case studies across critical‑mineral projects repeatedly reference capital‑expenditure overruns in the range of 30–40%, particularly for first‑of‑a‑kind separation or refining facilities. Project Vault’s reported 40% overrun is one recent illustration.

INTERPRETATION: Why Friend‑Shoring Is Harder Than It Looks

Materials Dispatch’s reading of this evidence is blunt: the policy story about moving critical‑mineral supply chains to “friends” crumbles under scrutiny of real‑world capacities, trust deficits, and mismatched incentives among those same friends. The rhetoric of seamless allied collaboration collides with three frictions: structural dependence on Chinese processing, fragmentation of policy among allies, and divergent priorities between defense and clean‑energy applications.

Capacity constraints: one China versus many small allies

China’s processing advantage rests on decades of cumulative investment, technology learning and integrated ecosystems clustered around magnets, batteries and specialty alloys. Allied friend‑shoring initiatives are, at present, a patchwork of discrete projects that often depend on Chinese equipment, engineering experience, or market demand even as they seek to “diversify away.”

To the extent that China controls 70–95% of processing and more than 200,000 tonnes per year of rare‑earth separation capacity, while leading allied projects target capacities in the low thousands of tonnes per year, any assumption of near‑term parity looks ungrounded. Even if every highlighted allied project (Lynas–Iluka, Nolans, MP’s expansions, Canadian refineries) were to deliver on time and on budget—conditions which past experience suggests are optimistic—the combined non‑Chinese separation capacity would still leave many supply chains structurally reliant on China for a large share of processed material.

Operational reality is harsher. Over the last procurement cycle, Materials Dispatch has observed repeated two‑ to three‑year slippages from initial commissioning dates, 30–40% capital‑expenditure overruns, and slower‑than‑planned ramp‑ups in metallurgy‑heavy projects. Under those conditions, friend‑shoring appears less like a quick hedge and more like a long‑duration transition with persistent single‑point‑failure risks. A handful of non‑Chinese refineries and magnet plants become the new choke points, rather than true redundancy to China’s ecosystem.

Policy fragmentation and trust deficits among allies

Friend‑shoring assumes that allies behave as a coherent bloc. The tariff, CBAM and export‑levy landscape suggests otherwise. US imposition of 25% Section 301 tariffs on critical‑mineral imports from Canada and Mexico—two formal FTA partners—sends a clear message that even close allies can be reclassified as targets if domestic politics favour visible “tough on trade” moves. European CBAM rules, meanwhile, put emissions‑intensive Australian and other allied metals at a disadvantage relative to lower‑carbon suppliers, regardless of security considerations.

Canada’s proposed levy on rare‑earth concentrate exports, designed to push value‑added processing onshore, introduces another layer of friction with US ambitions to pull concentrates into its own refineries. Japan’s stockpile mandates increase demand pressure in a relatively illiquid heavy‑REE segment, potentially crowding out other allied needs. And Ukraine, held up rhetorically as a future critical‑mineral partner, remains excluded from certain IRA tax‑credit benefits until at least a scheduled review.

Policy analysis from strategic‑studies institutions has been explicit about the resulting trust deficit, describing some of these reversals as “agreements torn up.” In practice, this forces procurement and risk teams to treat allied policy as a moving target rather than a stable foundation. Every new levy, tariff or exemption‑carve‑out increases the legal and compliance load just to maintain existing flows, let alone build new ones.

Defense versus energy: incompatible tolerances for cost and fragility

Defense supply chains and energy‑transition supply chains do not value the same things. High‑end defense platforms—fighter aircraft, submarines, precision‑guided munitions—require small volumes of very high‑purity materials (for example, NdPr, Dy, Tb for permanent magnets; titanium sponge for airframes) with extreme reliability and traceability. Defense ministries and prime contractors can and often do tolerate security premia and stockpiling overheads, because materials costs are a small fraction of program budgets.

By contrast, clean‑energy and mass‑market electronics supply chains require very large volumes at lowest‑possible unit cost: lithium, nickel, graphite, copper, and REEs for millions of EVs and turbines. Here, a 20–30% cost uplift linked to CBAM, friend‑shoring, or non‑Chinese processing can meaningfully slow deployment or shift manufacturing elsewhere. Evidence to date suggests that where friend‑shoring raises unit costs, defense applications are more likely to absorb those costs, while commercial and green‑energy applications remain exposed to cheaper, higher‑carbon or higher‑risk Chinese flows.

The likely outcome is de facto segmentation: a “defense track” of ring‑fenced, partly stockpiled, non‑Chinese material flows at a significant implicit security premium; and a “commercial/energy track” that continues to rely heavily on Chinese or mixed‑origin supply for cost reasons. That segmentation would complicate plant economics for allied refineries, which depend on blending defense‑grade and commercial volumes, and could entrench China’s dominance in cost‑sensitive segments even as allies secure narrow defense corridors.

Operational frictions: permitting, overruns, and disruptions

Permitting, legal challenges, and physical disruption have already undercut multiple high‑profile friend‑shoring projects. Litigation over Indigenous land rights and environmental impacts at the Nolans project, regulatory controversies around processing plants in Malaysia, and weather‑related downtime at Australian nickel and gold‑PGM mines illustrate how easily a single site can be taken offline or delayed for months.

From an operational‑risk perspective, allied friend‑shoring is currently built on an extremely narrow physical base: a few mines, a handful of separation plants, and even fewer magnet facilities. Materials Dispatch has seen sourcing strategies that assumed two‑ to three‑year ramp‑ups to full design capacity; experience shows that metallurgical tuning and community issues can stretch those timelines beyond five years. Against that backdrop, multi‑decade Chinese plants with fully depreciated infrastructure and deep local supply bases look even more entrenched.

When Chinese export‑control discussions alone can move NdPr prices by roughly 25% in a quarter, while allied capacity remains in construction or commissioning, the near‑term net effect of friend‑shoring is not necessarily lower volatility. Until alternative capacity is both large and diversified enough, the system remains highly sensitive to Beijing’s regulatory choices.

Mineral‑by‑mineral friction: where friend‑shoring is most strained

The frictions above do not apply evenly across all materials. Some segments are structurally more challenging for friend‑shoring:

- Heavy rare earths (Dy, Tb). With China holding around 95% of processing for heavy REEs, and non‑Chinese projects only targeting on the order of a few thousand tonnes per year by the late 2020s, this is the highest‑friction segment. Japanese stockpile mandates add further tightness.

- Graphite. China dominates graphite anode materials. Ukraine and Canada feature in diversification plans, but war‑related disruptions in Ukraine and potential tariff/levy frictions in North America complicate scaling.

- Nickel. EU CBAM pressures higher‑emission nickel routes while allies such as Australia wrestle with their own environmental and community constraints. Lower‑carbon deposits in Canada or other regions require substantial capital and time to build out.

- Titanium. Ukraine and Australia are both important titanium feedstock suppliers. War risks in Ukraine have already demonstrated how quickly a “friendly” source can become logistically constrained.

In each case, friend‑shoring is technically possible, but it collides with some combination of Chinese incumbency, allied policy friction, and local operational risk. The aggregate effect is a slower, more expensive and more politically fragile pathway than headline speeches imply.

WHAT TO WATCH: Regulatory and Industrial Weak Signals

Several developments will determine whether friend‑shoring in critical minerals remains mostly rhetorical or begins to reshape real flows:

- Final scope, product codes and enforcement posture for US Section 301 tariffs on Canadian and Mexican critical minerals, including any exemptions or suspensions negotiated under USMCA channels.

- How the European Commission implements CBAM for metals and whether nickel‑bearing intermediates central to batteries and stainless steel are pulled into the effective coverage through implementing acts.

- The exact form and timing of any renewed Chinese export controls on rare earths and magnets after November 2026, including licence requirements, product lists, and informal implementation signals from customs.

- Progress milestones at key allied projects (Lynas–Iluka Eneabba, Nolans, Canadian rare‑earth refineries, MP Materials’ magnet plant), including commissioning dates, reported throughput, and environmental/community challenge status.

- Formalisation of Japan’s stockpile mandates and any move by other allies to adopt similar minimum‑days‑of‑supply rules for Dy, Tb and other highly strategic inputs.

- Implementation guidance and audits around IRA Section 45X credits, particularly origin‑verification rules and any early evidence of non‑compliance or reclassification of partner countries.

- Decisions in Canada on the proposed export levy for rare‑earth concentrates and how these interact with US defense‑related offtake agreements and future US tariff policy.

- Whether the FORGE forum and Project Vault translate into binding offtake, joint‑financing vehicles and transparent stockpiling rules, or remain high‑level declarations with limited operational footprint.

- Evidence of de facto segmentation between defense‑oriented and commercial supply chains—for example, dedicated defense‑only processing lines, separate compliance regimes, or differentiated stockpile standards.

- Patterns of capital‑expenditure overruns, delays and cancellations across allied critical‑mineral projects, which will indicate whether financiers and policymakers are adjusting assumptions after early overruns.

Note on Materials Dispatch methodology Materials Dispatch integrates systematic monitoring of regulatory texts and official communications from key jurisdictions with project‑level reporting and trade‑flow data, then cross‑checks those signals against end‑use technical requirements in defense, automotive, power, and electronics supply chains. This combined view helps distinguish between headline policy announcements and measures that genuinely alter feasible material flows and qualification pathways.

Conclusion

The emerging evidence base points to friend‑shoring in critical minerals as a slow, conflict‑ridden realignment rather than a clean break from China. Capacity constraints, allied policy fragmentation, and diverging priorities between defense and clean‑energy users combine to create a landscape where rhetoric about friends often outpaces what rules, plants, and ports can actually deliver.

None of this implies that friend‑shoring will fail outright; it suggests instead that its outcomes will be uneven, mineral‑specific and politically contingent. For critical‑material stakeholders, the central task is not to accept or reject the friend‑shoring narrative, but to track how concrete regulatory measures, project execution and demand segmentation interact in practice. Materials Dispatch will continue active monitoring of regulatory and industrial weak signals that will define how friend‑shoring in critical minerals evolves from slogan to operational reality.