Case Study

Lynas, MP Materials and the Rare Earth Suppliers Outside China

As of mid-2026, the rare earth supply chain outside China rests on two anchors: Lynas Rare Earths and MP Materials. Together they cover roughly a quarter to a third of global demand, backed by a thin second tier of emerging projects in Australia, North America, the Middle East and Brazil. The system is structured but brittle: concentrated in a few strategic assets and exposed to a persistent neodymium-praseodymium (NdPr) and heavy rare earth (HRE) deficit.

Key Findings on 2026 Rare Earth Supply Resilience

- Lynas and MP Materials form the backbone of non‑Chinese rare earth supply, but both rely on complex multi‑jurisdictional processing chains that introduce logistical and regulatory single points of failure.

- The non‑Chinese NdPr deficit and even tighter HRE balance create a structurally “brittle” system: modest delays at one or two facilities can cascade into multi‑sector constraints for EVs, wind, and defense.

- US Department of Defense (DoD) funding and Australian policy support underpin several projects, but tie long‑term availability to political and budget cycles as much as to geology.

- Emerging projects (Arafura Nolans, Maaden-MP JV, Browns Range, Eneabba and others) are strategically important as diversification levers, yet most remain exposed to schedule risk, permitting friction, and infrastructure constraints.

- Shipping routes, water availability, and radioactive waste rules are not side issues; they are central to uptime and ramp‑up reliability for nearly every major non‑Chinese supplier.

Analytical Framework: How Operational Continuity Was Evaluated

This review draws on public disclosures, technical reporting, and specialist analysis from 2025-2026 to assess each supplier on four operational axes: (1) ability to sustain or grow production through 2026-2030, (2) vulnerability to logistical and infrastructure disruptions, (3) exposure to regulatory and ESG constraints, and (4) geopolitical insulation from coercive trade dynamics. Instead of focusing solely on nominal tonnes of rare earth oxide (REO), the emphasis is on NdPr and HRE flows, since those underpin permanent magnets for EV traction motors, offshore wind turbines, precision‑guided munitions, and advanced aerospace systems.

Within this framework, Lynas’ integrated Mt Weld–Kalgoorlie–Malaysia–Texas system and MP Materials’ Mountain Pass–US magnet strategy emerge as the primary pillars of non‑Chinese supply. Other projects are assessed relative to these anchors, with particular attention to how they alleviate – or replicate – existing bottlenecks.

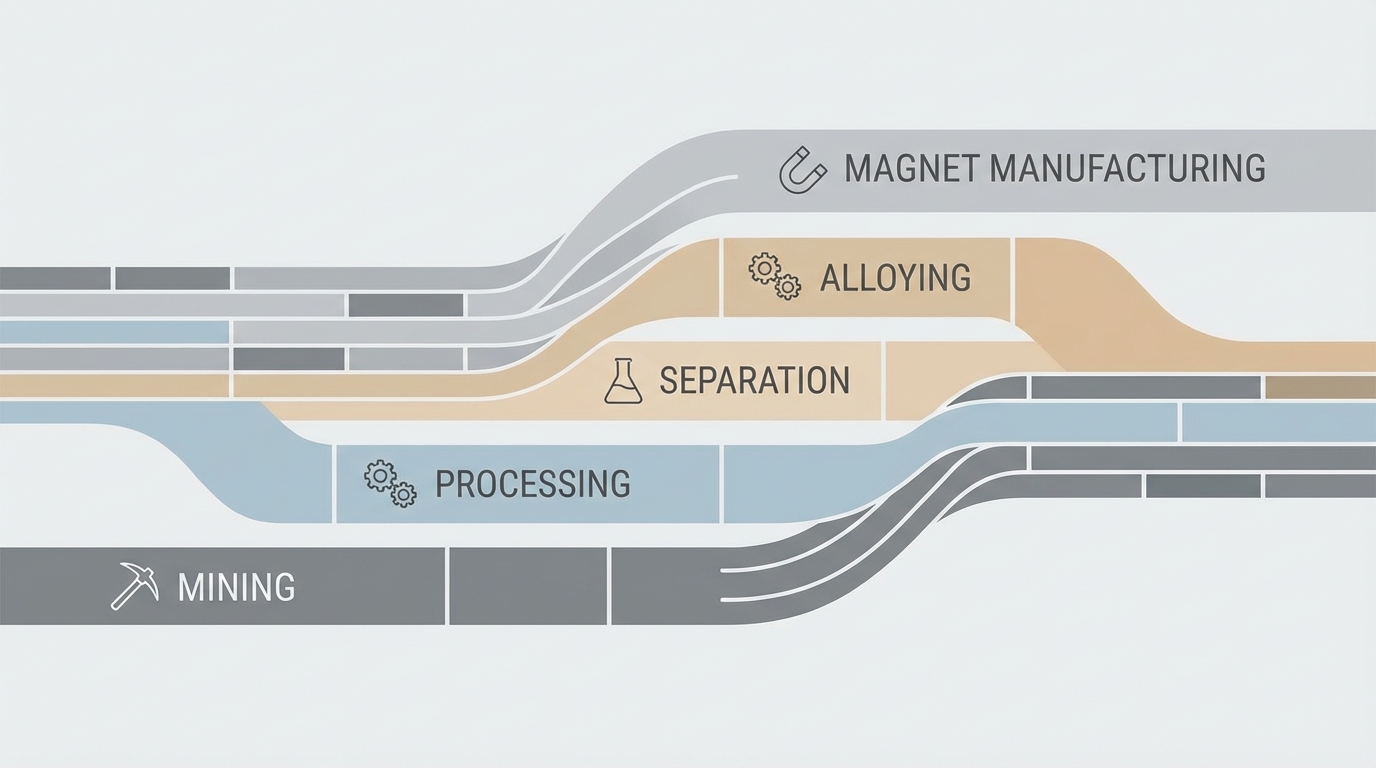

Lynas Rare Earths: Integrated Chain with Multi‑Jurisdictional Fragility

Lynas controls one of the highest‑grade rare earth deposits at Mt Weld in Western Australia and operates a complex downstream chain that, by 2026, spans mining and concentration in Australia, cracking and separation in Malaysia, and a DoD‑funded heavy rare earth facility in Texas.

Production Profile and Strategic Role

For 2026, Lynas projects total REO production of about 16,100 tonnes, a 53% year‑on‑year increase, including approximately 8,800 tonnes of NdPr oxide with 35% growth. Company reporting indicates that NdPr accounts for the majority of revenue, and external analysis estimates Lynas covers around 5–7% of global NdPr demand. In the first half of its 2026 financial year alone, production had already reached 7,609 tonnes of REO, underpinning the likelihood of the full‑year target being technically achievable if operations remain stable.

Lynas is also expanding into heavy rare earth separation. Following the first non‑Chinese commercial dysprosium (Dy) oxide production in May 2025, the company has highlighted an HRE program that begins with samarium (Sm) from April 2026 and is expected to scale to other elements including gadolinium (Gd), Dy, terbium (Tb), yttrium (Y) and lutetium (Lu) over the subsequent two years. Exact tonnages for each HRE stream have not been disclosed, but the presence of this capability outside China is structurally significant for high‑temperature magnet and defense applications.

Operational Continuity: Strengths and Failure Points

On the continuity side, Lynas benefits from several stabilizing factors:

- A mature mine at Mt Weld with disclosed reserves around 2 million tonnes REO, providing resource security beyond the current decade.

- An established separation facility in Malaysia with a track record of producing separated oxides at industrial scale.

- A customer base reportedly aligned to long‑term strategic contracts rather than spot sales, dampening some short‑term market volatility in offtake patterns.

- Flexibility to process third‑party feedstocks deemed ESG‑compliant, which can partially offset mine‑specific disruptions.

that said, the same configuration carries embedded fragilities. The Australian ore is shipped to Malaysia for cracking and separation, creating exposure to maritime chokepoints and freight disruptions. During periods of Red Sea instability, for example, diversions increase lead times and operational complexity, especially when synchronized with maintenance outages or ramp‑up work on new circuits.

Regulatory risk at the Malaysian plant is perhaps the most significant structural issue. The facility has been subject to ongoing scrutiny over the management of low‑level radioactive waste, particularly thorium‑bearing residues. Stricter environmental conditions and licensing reviews have already contributed to delays and limitations on HRE ramp‑up capacity. Any tightening in waste regulations, or political shifts around permitting, could constrain throughput or force reconfiguration of flows between Malaysia, Australia and the US.

To mitigate part of this concentration risk, Lynas is building additional processing capability at Kalgoorlie in Western Australia and an HRE separation plant in Texas backed by US DoD funding. While these assets enhance diversification, they also introduce a classic ramp‑up challenge: overlapping commissioning schedules, acute engineering labor needs, and the need to stabilize three major facilities (Kalgoorlie, Malaysia, Texas) around the same mid‑decade window.

Risk Inflection Points for Lynas

- Malaysian licensing and waste policy: Any non‑routine change in thorium disposal requirements, license renewals, or community consent processes is a direct lever on effective capacity and uptime.

- Shipping lane disruptions: Sustained instability in key trade routes linking Western Australia and Malaysia would increase lead times and inventory requirements, stressing working capital and scheduling.

- Texas HRE ramp‑up: The US facility is intended to diversify geopolitical risk, but early‑stage operations can be prone to mechanical and process instability. Delays here would leave HRE reliance skewed back toward Malaysia.

- Third‑party feedstock strategy: While processing external material adds resilience, it also brings variability in feed composition, which can challenge plant optimization if not carefully sequenced.

Overall, Lynas is structurally critical for both NdPr and HRE availability outside China, yet its integrated chain remains sensitive to regulatory outcomes in Malaysia and execution risk across multiple expansion fronts.

MP Materials: From Concentrate Exporter to Integrated US Magnet Supplier

MP Materials operates the Mountain Pass mine in California, historically one of the world’s major light rare earth sources. The company has been transitioning from a concentrate‑focused model with shipments to China toward a fully integrated US supply chain encompassing mining, separation, and magnet manufacturing.

Production Evolution and Strategic Significance

By 2024/25, Mountain Pass had achieved a record output of roughly 45,000 tonnes REO in concentrate form, representing around 15% of global demand according to sectoral analysis. In 2026, the strategic pivot is toward refined oxides and magnets:

- Stage II: High‑purity separated oxides, including announced heavy rare earth capability of around 200 tonnes per year of Dy/Tb once ramp‑up is complete.

- Stage III: NdFeB magnet manufacturing targeting an initial 1,000 tonnes per year and a longer‑term goal of up to 10,000 tonnes by around 2028, enabled in part through a magnet facility backed by the US DoD.

The company has also publicly stated that exports of concentrate to China ceased from the third quarter of 2025, with material retained for domestic processing. This move is strategically aligned with US policy priorities and positions MP as a cornerstone for domestic defense and EV motor supply chains.

Operational Continuity and Structural Constraints

Mountain Pass benefits from operating entirely within the US, removing cross‑border permitting and customs uncertainties that characterize multi‑jurisdictional chains. US regulatory frameworks are stringent but relatively predictable, and DoD participation adds stability around project funding horizons.

At the same time, several operational risk factors stand out:

- Ore profile: The deposit is heavily skewed to light rare earths, particularly cerium and lanthanum, with lower proportions of HREs. The announced 200 tonnes per year Dy/Tb capacity is strategically important but inherently limited by geology, which constrains how far MP can go in solving broader global HRE tightness on its own.

- Water and environmental constraints: Mountain Pass is in a water‑stressed desert environment. Process water management, tailings stewardship, and regulatory scrutiny under California and federal rules are ongoing operational considerations that can affect throughput and expansion plans.

- Stage II and III ramp‑up: Transitioning from concentrate to separated oxides and magnets introduces new technical and organizational complexity. Commissioning integrated chemical and metallurgical circuits has historically been a frequent stumbling block in the rare earth sector.

- Labor and technical skills: The combination of mining, chemical processing, and advanced magnet manufacturing requires a specialized workforce, at a time when engineering and skilled labor shortages have been widely reported across North American industrial projects.

DoD awards totalling over US$400 million since 2020, plus an additional heavy rare earth plant loan of around US$150 million, reduce financial uncertainty around Stage II and III development. Yet this same defense linkage exposes the project to US federal budget dynamics and policy shifts. Any future change in strategic priorities could alter the level of official support, which in turn would influence expansion pace and product mix.

Saudi JV and Global Positioning

In partnership with Saudi Arabia’s Maaden, MP Materials is advancing a joint venture intended to create a rare earth hub in the Kingdom, with HRE production targeted from around 2028. Current reporting places the project in pre‑construction following a 2025 final investment decision, with mine build activities expected to begin in the same period.

For operational continuity, this JV has a dual character. It offers diversification away from North America and East Asia, locating capacity in a country that is actively pursuing industrialization under its Vision 2030 strategy. At the same time, the asset is likely to be exposed to desalinated water supply, desert logistics, and broader regional geopolitical tensions, including those linked to conflicts in neighboring countries and the volatility of hydrocarbon‑driven fiscal cycles. These factors create potential for supply interruptions that are different in nature from those faced at Mountain Pass, but no less material.

Arafura Resources’ Nolans Project: High‑Impact Future Supply with Near‑Term Schedule Risk

Arafura’s Nolans project in Australia’s Northern Territory is designed as an integrated mine and on‑site refinery focused on NdPr oxide. Public plans point to commercial start around 2028, with a full ramp‑up to approximately 4,440 tonnes per year of NdPr oxide expected between 2030 and 2032.

From a supply‑chain risk perspective, Nolans’ main contribution is temporal: it aims to fill the mid‑to‑late‑decade NdPr deficit as demand from EVs, wind, and industrial motors continues to outpace present non‑Chinese capacity. Local refining is explicitly designed to bypass China for value‑added steps, strengthening supply assurance for customers requiring ex‑China compliance for sensitive applications.

However, the project also illustrates standard development‑phase fragility. External reporting points to delays relative to initial schedules, driven by the complexity of building a full hydrometallurgical and separation plant in a remote, arid region. Logistics for reagents, water, and product shipment are challenging, and cost inflation has been a recurrent theme across Australian resources projects in the mid‑2020s. There is also an overlay of indigenous land and permitting processes specific to the Northern Territory, which can extend timelines if not carefully managed.

If delivered broadly in line with current expectations, Nolans would become a key NdPr pillar for the early 2030s, partially relieving pressure on Lynas and MP, particularly if demand growth tracks higher‑end scenarios. Until construction is demonstrably de‑risked, though, its contribution remains more of a forward‑looking buffer than a secured component of the 2026–2030 baseline.

Supporting and Emerging Supply Nodes: Diversification with Limited Near‑Term Volume

Beyond the two main incumbents and Nolans, a range of smaller or earlier‑stage projects contribute to diversification, though often with modest tonnages or later start dates.

Lynas USA Texas Facility and Kalgoorlie Expansion

Lynas’ Texas heavy rare earth facility, constructed with substantial DoD support, is scheduled to ramp during 2026. It will be supplied by feedstock from Mt Weld, via Kalgoorlie and/or Malaysia. Strategically, this plant is designed to provide US‑based HRE separation for defense and critical industrial uses, reducing reliance on Malaysian processing for certain elements.

From an operational risk standpoint, the Texas facility is still in the construction and commissioning phase. That introduces typical greenfield uncertainties: contractor performance, supply availability for critical equipment, and potential changes in US environmental permitting expectations, particularly regarding handling of radioactive residues. Any delay here would preserve reliance on Malaysia for longer, although the existence of multiple Lynas processing sites does offer some flexibility in how feedstocks are routed.

Northern Minerals’ Browns Range and Other HRE‑Focused Assets

Northern Minerals’ Browns Range project in Western Australia is one of the few Western operations explicitly focused on HREs such as Dy and Tb. Pilot operations have produced an estimated 500 tonnes per year of Dy/Tb‑rich concentrate, highlighting its potential strategic value for high‑performance magnet applications. However, current volumes are small relative to global requirements, and the project has faced repeated financing challenges and the inherent complexity of moving from pilot to full‑scale production.

Iluka Resources’ Eneabba refinery, which processes monazite and other mineral sands‑derived feedstocks, is another important HRE‑capable asset. First REO output is targeted for 2026, with initial capacities in the hundreds of tonnes per year according to sector estimates, though detailed breakdowns remain limited. The key operational issue here lies in waste and by‑product management, given the presence of uranium and thorium in some monazite streams, and the need to integrate feed from multiple external mines that are optimized primarily for zircon and titanium minerals rather than rare earths.

North American and Brazilian Projects: Round Top, Bahia, and Magnet Makers

USA Rare Earth’s Round Top project in Texas is often cited for its HRE‑rich resource and its potential to supply both REOs and other critical materials. Current plans refer to an output around 2,000 tonnes REO from 2028 onwards, but the project remains subject to permitting, financing, and engineering milestones. Its location within the US is positive from a geopolitical standpoint, yet also subjects the project to the same environmental and community‑consultation structures that have elongated timelines for other mining developments.

Energy Fuels’ Bahia project in Brazil, focused on monazite‑bearing heavy mineral sands, is expected to contribute HRE‑containing feedstock from around 2026 at an initial scale reported to be in the low hundreds of tonnes REO equivalent per year. While this provides jurisdictional diversification, it introduces another set of environmental and legal dynamics. Brazilian litigation around mining, indigenous rights, and land use is an ongoing factor to watch, alongside the reliability of export logistics from Brazilian ports to processing facilities in the US.

On the magnet side, Noveon Magnetics in Texas represents an early example of domestic NdFeB magnet capacity in the US, with around 1,000 tonnes per year targeted for 2026 and DoD involvement to encourage recycling and closed‑loop supply. Noveon relies on upstream oxide availability from entities like Lynas and MP or recycled scrap, so its operational continuity is to some extent downstream of the mining and separation reliability discussed earlier.

Multi‑Metal Projects: Alkane Dubbo and Similar Assets

Alkane Resources’ Dubbo project in New South Wales is a multi‑metal venture, with a flow sheet designed to produce REOs alongside zirconium and niobium products. Plans call for around 4,000 tonnes REO from 2028, but final investment decision timing has been repeatedly pushed back. Multi‑commodity character can provide resilience once operational, since revenue is diversified across several critical materials, yet it complicates project financing and adds technical depth to commissioning and process optimization.

Systemic Supply Chain Risks Through 2030

When the ecosystem is viewed as a whole, a few structural realities become clear. First, non‑Chinese rare earth supply in 2026 remains highly concentrated in two incumbents, a structure made more fragile by China’s tightening export rules. Combined, Lynas and MP Materials are estimated to provide around 100,000 tonnes REO equivalent of non‑Chinese capacity (including concentrate), covering roughly a quarter to a third of global demand. Despite this, sector assessments point to a continuing NdPr shortfall on the order of 10,000 tonnes, and an even tighter environment for key HREs such as Dy and Tb.

Second, a significant portion of this volume relies on maritime transport between Australia, Malaysia, the US, and, prospectively, Saudi Arabia and Brazil. Disruptions in any of the major shipping arteries – whether through conflict, sanctions, piracy, or infrastructure accidents – would quickly manifest as delays in feedstock deliveries to separation plants and magnet facilities. The requirement to handle, store, and ship slightly radioactive material adds another layer of complexity to contingency planning.

Third, environmental and social regulation is emerging as a central gatekeeper of operational continuity. Thorium‑bearing waste streams in Malaysia, water stewardship in California and Saudi Arabia, indigenous land rights in Australia and Brazil, and US federal and state permitting all represent non‑geological constraints determining how quickly capacity can be brought online and sustained. In several cases, project schedules have already been adjusted materially due to these factors.

Fourth, policy‑driven funding – particularly from the US DoD – is now embedded in the business models of a number of key assets. This provides stability and demand assurance but introduces a policy‑cycle dependency: future administrations or budget environments may recalibrate priorities around domestic mining versus recycling, stockpiling, or allied‑nation sourcing.

Signals to Watch for Supply Chain Stability

Several observable developments over the coming few years will shape how robust the non‑Chinese rare earth supply chain becomes:

- Lynas regulatory milestones in Malaysia: License renewals, waste disposal agreements, and any changes in treatment of thorium‑bearing residues will directly influence HRE availability and total NdPr output.

- MP Stage II/III commissioning performance: Evidence of stable high‑purity oxide production and consistent magnet output at Mountain Pass and associated facilities will indicate that the integrated US pathway is functionally delivering on its design.

- Nolans and Eneabba construction progress: Movement from site preparation to mechanical completion at these projects will materially alter the mid‑decade NdPr and HRE balance if executed close to planned timelines.

- Geopolitical and maritime developments: Stability in the Red Sea, Straits of Malacca, and key Pacific routes will remain integral to the practical flow of ore and oxides between the main production hubs.

- Evolution of recycling and substitution technologies: While still emerging, any large‑scale deployment of NdFeB recycling or partial substitution in lower‑spec applications would reduce pressure on primary supply and alter the risk landscape.

After several years of monitoring this space, a consistent picture emerges: progress is real, with Lynas and MP Materials anchoring a gradually diversifying ecosystem, yet the system remains structurally exposed. Non‑Chinese rare earth supply in 2026–2030 is less a broad, redundant network and more a concentrated set of critical nodes, each carrying characteristic operational, regulatory, and geopolitical risks that require ongoing scrutiny.