Data Brief

Weekly dispatch #2: policy moves, new mines, and logistics chokepoints: Latest Developments and

Weekly Dispatch #2: Policy Shifts, New Mines, and Logistics Chokepoints

This week’s market pivot is driven by converging policy actions and targeted capacity builds that re‑route rare earth and strategic metal supply lines through 2026-27. The White House Executive Order of 15 January 2026 tightening imports of processed critical minerals, together with Beijing’s 9 January 2026 export restrictions to Japan, materially raise compliance burdens and compress available processed HREE/NdPr volumes outside China.

- New fact: The US EO (15 Jan 2026) creates mandatory due‑diligence and negotiating timelines for non‑Chinese processing agreements; China restricted civilian rare earth shipments to Japan on 9 Jan 2026.

- Why it matters: Processed critical minerals (PCMDPs) face routing and licensing scrutiny; shortfalls in HREEs (dysprosium/terbium) and NdPr will persist until new refineries scale.

- Immediate risk: Logistics delays (ports, seasonal routes, export licences) add multi‑week lead times and concentrate pressure on a handful of non‑Chinese processors.

- Signals to watch: EO negotiation outcomes Q1 2026, G7 coordination on price floors, ramp rates at Mountain Pass, Yangibana, Nechalacho, and reported China licence approvals for export to third countries.

Policy moves: from import controls to trade counter‑measures

The White House’s 15 January Executive Order explicitly links trade tools to national security by pushing the Commerce Secretary to secure processing agreements with allied partners and to consider trade remedies (tariffs, import restrictions) on PCMDPs if diversification targets are not met. Implementation is front‑loaded into Q1-Q2 2026 and carries exemptions for allies that can demonstrate verifiable processing origin. Parallel actions include EU export restrictions on rare earth waste and expanded recycling targets in the UK and India.

China’s export licensing changes – applied most recently against Japan on 9 January 2026 following diplomatic tensions – reintroduce dual‑use scrutiny into civilian shipments and extend delays seen after the April 2025 licence regime. These measures concentrate processing demand outside China while elevating the strategic value of accessible HREE separation capacity.

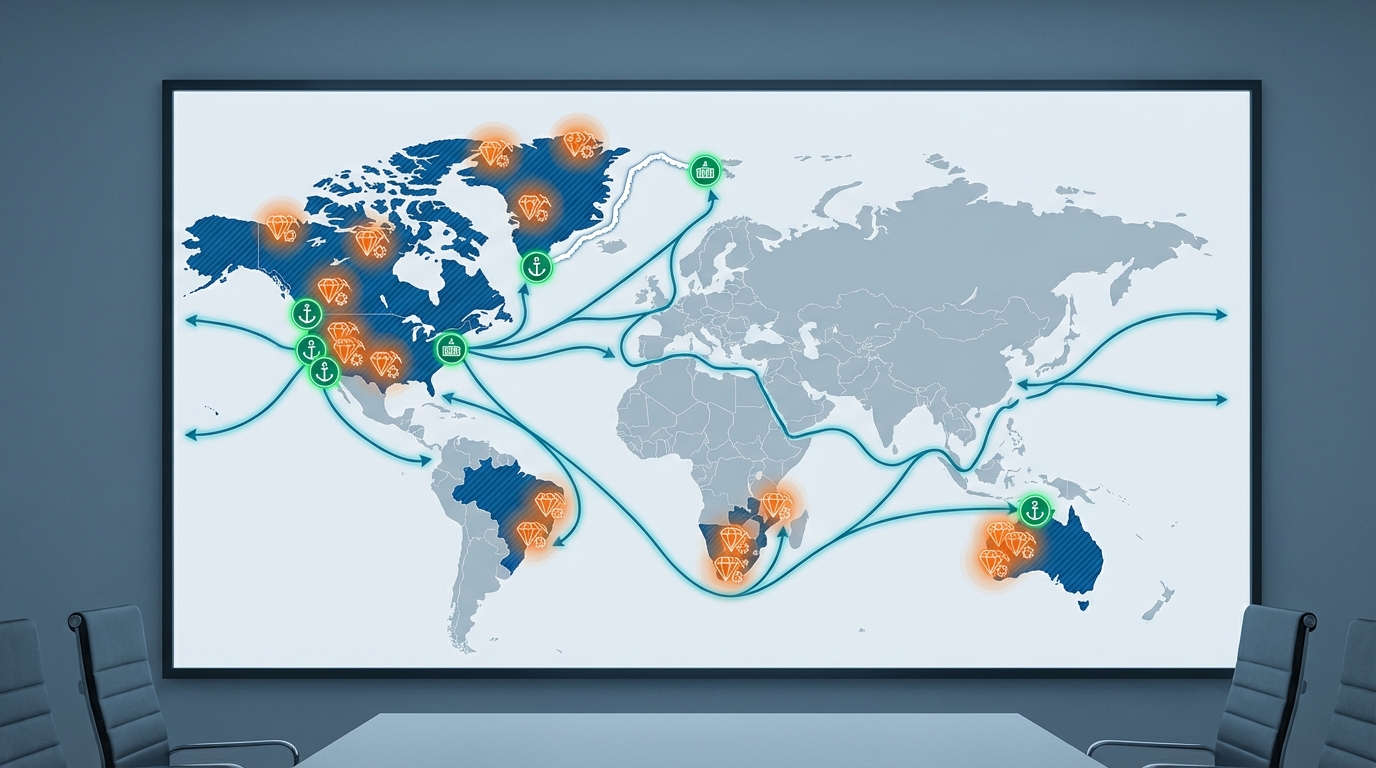

New mines and processing ramps: partial offset for an acute HREE squeeze

Several non‑Chinese projects are moving to operational or near‑operational status in 2026-27 and will be focal points for supply diversification. Notable examples with capacities cited in recent reporting include Mountain Pass (MP Materials – domestic separation and Stage II processing online in Q1 2026), Yangibana (Hastings — NdPr output targeted in mid‑2026), Nechalacho (Northwest Territories — HREE‑rich concentrate), and Wicheeda and Eldor in Canada/Quebec pursuing magnet‑ready oxides.

These projects reduce single‑point dependence but will not fully replace China’s processing depth in the near term. Reported constraints include logistics (port and seasonal access), labour and permitting challenges, and the capital intensity of downstream refining; several projects enjoy political prioritization or finance commitments from US, EU, or allied frameworks, which accelerates timelines but does not eliminate scale‑up risk.

Logistics chokepoints amplifying policy risk

Operational bottlenecks materially deepen the policy shock. Long Beach and other US West Coast ports handle a large share of rare earth flows and reported labour/tariff frictions add 2–4 weeks to lead times. Arctic road and seasonal shipping constraints limit throughput from northern Canadian projects. Australian monsoon season constrains exports via Darwin. EU bans on scrap exports reroute secondary feedstocks and tighten recycled supply into 2026.

Risks, trade‑offs, and compliance implications

Immediate risks include compressed availability of processed HREEs and NdPr, heightened regulatory documentation for PCMDPs, and short‑term price volatility already reported in dysprosium and NdPr premia. Trade‑offs are visible: accelerated permitting in some allied jurisdictions shortens development lead times, while EU procedural delays extend others. The interplay of export licensing, port congestion, and project ramp rates will determine whether non‑Chinese capacity fills near‑term gaps or simply cushions the transition.

Signals to watch

- Q1–Q2 2026 outcomes of the US Commerce negotiations and allied exemptions under the EO;

- G7 coordination on price‑management or offtake guarantees that would shift demand to junior developers;

- Ramp‑up reports from Mountain Pass, Yangibana, Nechalacho and other non‑Chinese processors; shipment manifests showing processing origin;

- Chinese licence issuance patterns for exports to third countries and any extensions of dual‑use coverage;

- Port strike or labour developments at Long Beach, Darwin, and Durban that would add multi‑week delays.

Materials Dispatch Signal: Policy is now the principal driver of near‑term rare earth routing. Reported project ramps create a credible diversification trajectory into 2027, but constrained refinery scale, export licensing and chokepoints preserve an elevated premium on HREE/NdPr supply and sustain compliance complexity. Quarterly tracking of EO implementation, project ramp metrics, and licence approvals will reveal whether the transition becomes structural or remains a policy‑driven premium cycle.