Data Brief

Weekly dispatch #5: port congestion, sanctions, and insurance withdrawals: Latest Developments and

Weekly Dispatch #5: Port Congestion, Sanctions, and Insurance Withdrawals

A confluence of port congestion at major hubs, continuing Chinese export licensing controls on key rare earths and a pullback of insurance capacity from high‑risk maritime zones is materially tightening logistics and delivery windows for rare earth elements (REEs), platinum‑group metals (PGMs) and strategic battery metals in 2026. Market reporting and freight analysis show longer routings, elevated demurrage and sharper insurance premia that are already reshaping sourcing and routing decisions across defence, EV and electronics supply chains (S&P Global; Xeneta).

- New fact: Port congestion plus sanctions and insurer withdrawals are creating 10-120+ day shipment slowdowns for critical REE/PGM flows in 2026 (reported operational delays and license timing from recent industry dispatches).

- Why it matters: Heavy rare earth shortages (dysprosium, terbium, lutetium) and PGM routing constraints directly affect magnet production for defence/aviation and catalyst supply for EV/hydrogen tech, raising landed‑supply risk and qualification timelines.

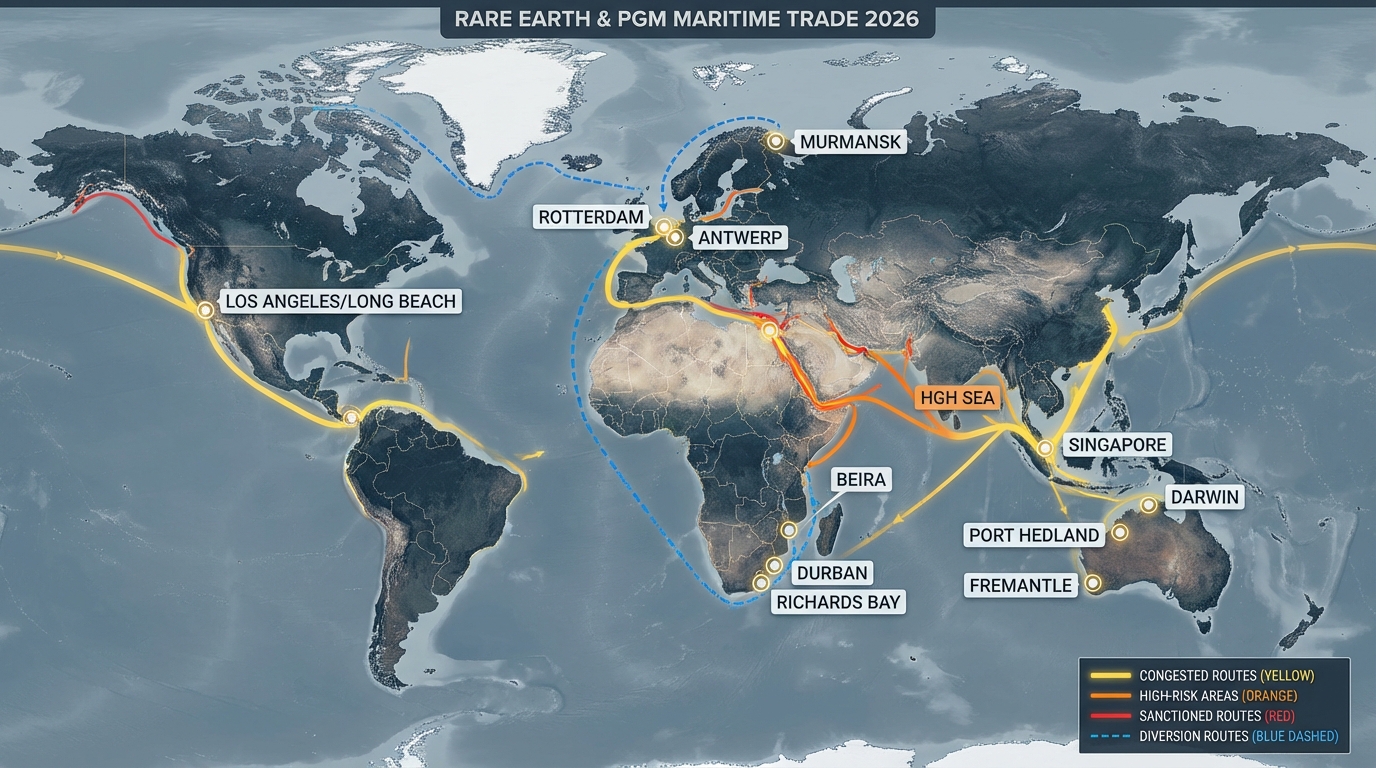

- Immediate risk: Longer Cape‑of‑Good‑Hope routings and Arctic/Murmansk congestion raise demurrage and insurance premiums; observable near‑term signals include vessel bunching in Rotterdam/Antwerp and insurer capacity cuts for Red Sea transit.

- Signals to watch: licence issuance rates for China’s April 2025 REE controls (pause through Nov 10, 2026 reported), Lloyd’s/major reinsurer capacity notices for the Red Sea and berth wait statistics at LA/Long Beach, Durban and Rotterdam.

Top affected facilities and route nodes (concise assessment)

Facilities and routes are ranked by strategic criticality-defence/aerospace exposure highest-using disclosed capacities and reported operational impacts where available.

- Mountain Pass, USA (Ca.) – Reported 40,000 MT/yr REE oxide capacity (ramp targets cited). Exports delayed by Long Beach/LA berth waits and inland trucking congestion; dysprosium flows cited as facing multi‑week delays (S&P Global).

- Mt Weld / Lynas (Australia) — Significant non‑Chinese HREE source feeding new Texas refinery; Fremantle/Rotterdam congestions and Indian Ocean insurance hikes reported to extend lead times via Cape routing.

- Mogalakwena (Anglo American, South Africa) — Major PGM output; Durban congestion and Houthi‑zone insurance withdrawals have driven Cape diversions and multi‑day export delays for PGM concentrates (Xeneta reporting).

- MP Materials separation (Fort Worth, TX) — U.S. separation capacity scaling; Houston/Galveston port bottlenecks and delayed Australian concentrate arrivals reported to affect trial dysprosium throughput.

- Iluka / Eneabba and other Australian processors — Monazite and HREE processing capacity expanding, but West Australian port crowding and insurance premia for Asia lanes are elevating landed timing variability.

- Norilsk / Russian Arctic routes — Large palladium volumes persist but face insurer capacity gaps on Arctic/Baltic legs and Murmansk congestion that have redistributed flows and increased delivery risk to EU/Asia buyers.

- Zimplats (Zimbabwe) and Sibanye‑Stillwater (South Africa) — Regional PGM suppliers absorbing spillover demand from Russia; Beira, Richards Bay and other southern African ports show elevated berth times associated with weather, labor and recovery operations.

- Arafura / Nolans, Greenland prospects — Development‑stage HREE projects noted as diversification levers; port constraints (Darwin, Nuuk) and permitting timelines still material to near‑term supply relief.

Logistics, sanctions and insurance: how the mechanics are changing

Port congestion at Rotterdam, Antwerp and U.S. gateways is causing vessel bunching and extended demurrage exposure; South African ports face compounded labor/weather risks. China’s April 2025 export licensing regime for several REEs—reported to remain constrained through a November 10, 2026 pause—continues to slow legal outbound flows for dual‑use HREEs. Concurrently, reinsurer capacity withdrawn from Red Sea/Houthi‑adjacent areas has driven war‑risk premia and rerouting to longer Cape or Arctic legs, with observable increases in quoted freight and insurance leads (S&P Global; Xeneta).

Operational impacts reported include shipment delays of 10-120+ days depending on route and sanction exposure, demurrage events at major hubs, and insurer re‑quoting that has disrupted scheduled rollings of separated oxides and PGM concentrates. These effects are concentrated where defence‑grade HREEs and high‑value PGM bars transit through single chokepoints.

Observed mitigation approaches and compliance considerations

Industry responses reported in the field include route diversification (Suez vs Cape trade‑off modeling), higher buffer inventories for defence‑critical magnet feedstocks, qualification of alternate non‑Chinese processors and tighter audit trails for dual‑use licence compliance. Insurer notices and regulator timelines (including Section 301 transshipment scrutiny and EU carbon rules affecting PGM smelters) are cited as drivers for supply‑chain redesign rather than short‑term tactical fixes.

Signals to monitor

- Licence issuance cadence for Chinese REE export controls and any MOFCOM guidance updates (key date referenced: Nov 10, 2026).

- Berth‑wait and demurrage statistics at Rotterdam, Antwerp, LA/Long Beach, Durban and Richards Bay.

- Public reinsurer/Lloyd’s capacity statements for Red Sea/Houthi and Arctic corridors.

- Regulatory actions on transshipment and CBAM enforcement impacting PGM origin certification.

Materials Dispatch Signal: The current alignment of port congestion, export controls and insurer retrenchment is catalyzing a structural re‑rating of logistical risk for HREEs and PGMs. Near‑term volatility and delivery uncertainty are likely to persist until routing patterns stabilize, insurer capacity normalizes or additional non‑Chinese separation capacity comes online. Market participants are shifting from single‑route dependency toward multi‑node sourcing, with implications for qualification lead times, compliance documentation and inventory strategy.