Data Brief

Weekly dispatch #6: elections, coups, and policy volatility in key jurisdictions

Executive summary

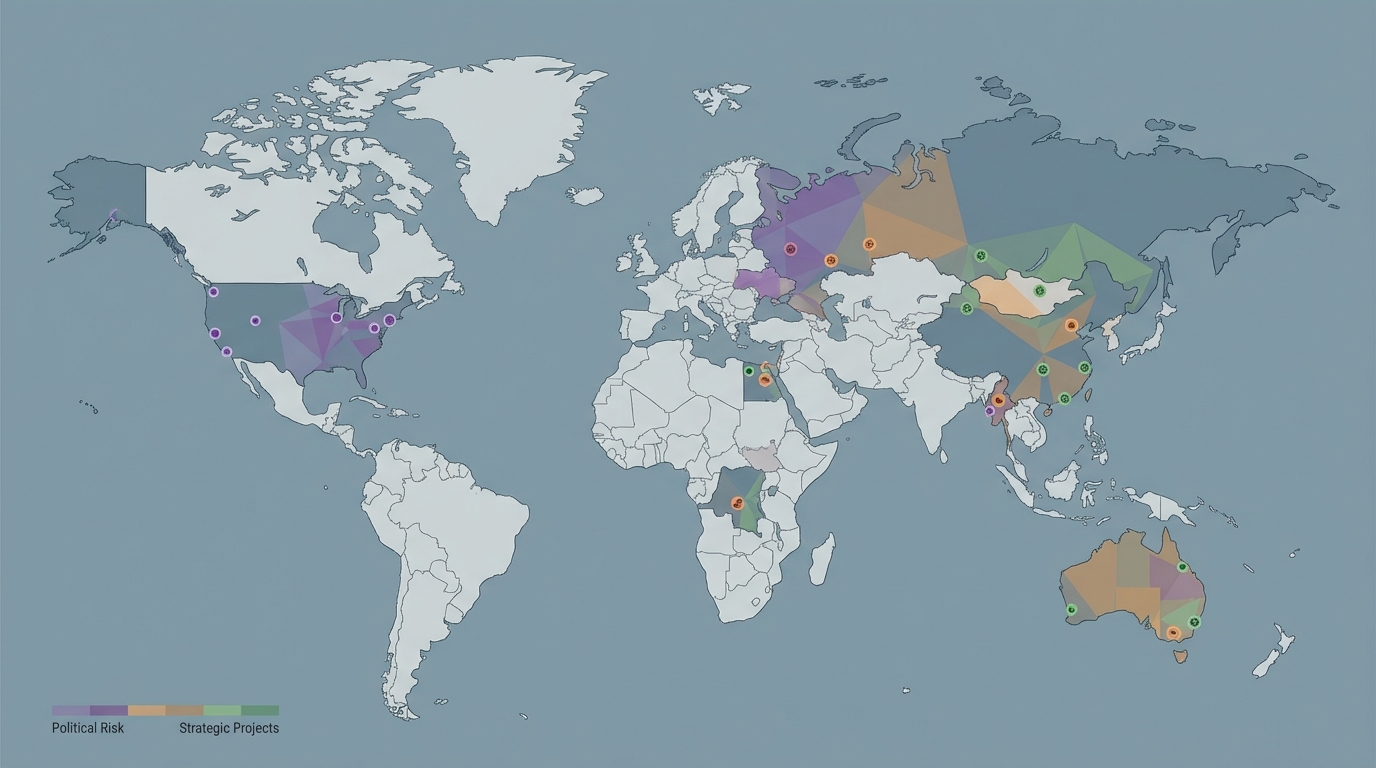

Political events in early 2026 are materially altering risk profiles across rare earth and strategic metal supply chains. U.S. election-driven industrial policy, renewed Chinese export controls, and localized coups in Myanmar and the DRC have elevated heavy rare earth (HREE) disruption risk while accelerating onshoring efforts. The market impact is concentrated on a handful of high‑criticality assets: Mountain Pass (MP Materials), Kachin HREE projects, Lynas Kalgoorlie, Chinese GanZhou clusters and emerging U.S. separation capacity in Fort Worth.

- Immediate change: Political volatility has converted a structural HREE tightness (20-30% shortfall outside China) into episodic supply shocks for dysprosium/terbium‑heavy supply chains.

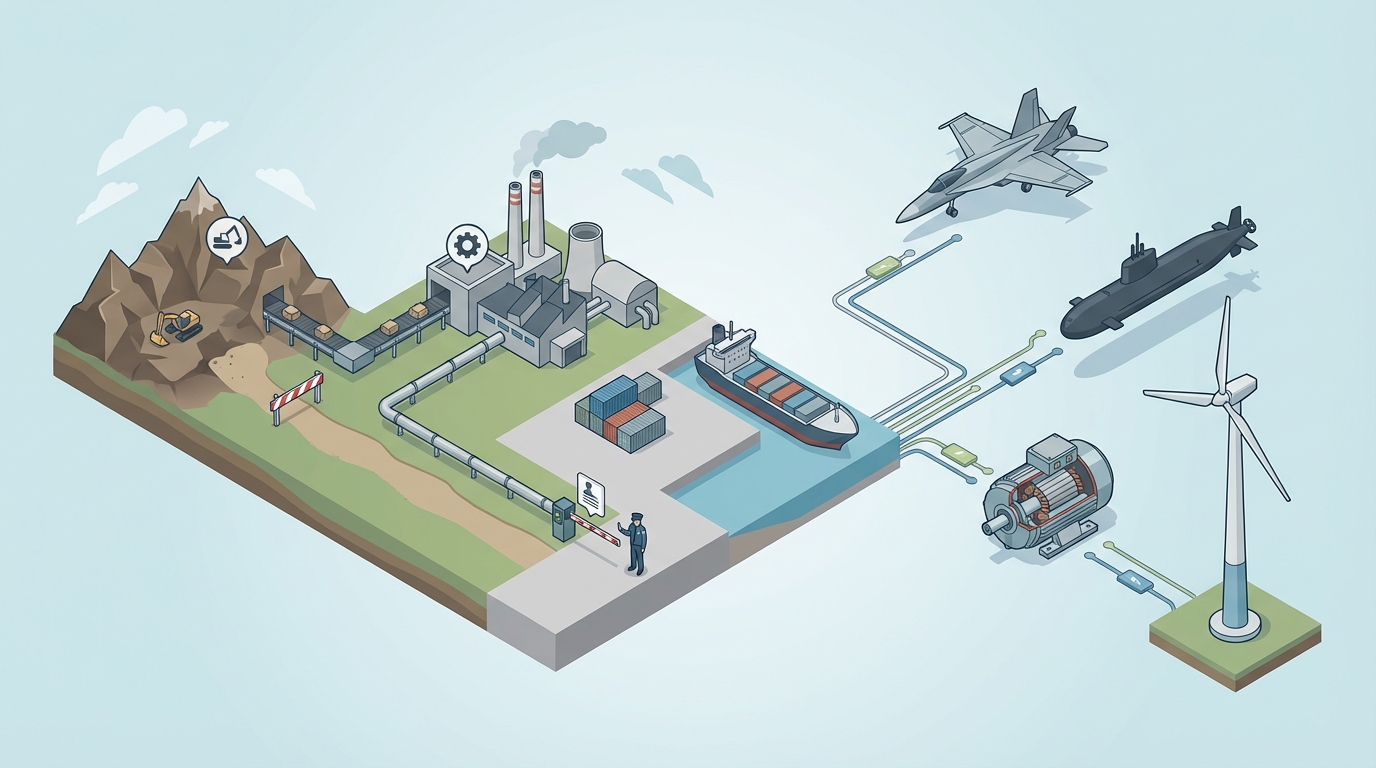

- Why it matters: Defense applications (permanent magnets, optics) and high‑temperature industrial uses face substitution limits; sourcing shifts create compliance and logistics complexity.

- Near‑term risk: Coup‑related shutdowns (Kachin, parts of DRC) create acute 0% output scenarios; Chinese licensing windows (30-60 days) and export list expansions amplify just‑in‑time fragility.

- Signals to watch: Feb 2026 China‑U.S. truce decisions, U.S. midterm outcome (Q3 2026 policy continuity), MOFCOM license turnaround times, and physical stockpile movements.

What changed and why it matters

Three political vectors converged in early 2026 to raise execution risk across strategic metals chains. First, U.S. domestic policy acceleration after the 2024/2025 election cycle has underwritten onshore capacity (Mountain Pass expansions; a Fort Worth separation plant) and direct Department of War (DoW) support for offtake and reserves. Second, Beijing expanded export controls in 2026 to include additional HREEs, and license processing remains a multi‑week bottleneck for international buyers. Third, regional coups and separatist actions (notably in Kachin State, Myanmar, and political turmoil in parts of the DRC) have halted high‑grade HREE production and disrupted logistics corridors to Chinese processors.

Top exposures and operational notes

MP Materials’ Mountain Pass (California) and Lynas’ Kalgoorlie (Western Australia) surface as the most resilient sources from an uptime and compliance standpoint. Mountain Pass reports 40,000 MT/year REE oxide capacity (ramping plans to 60,000 MT by late 2026) and a DoW equity/offtake framework that secures output at a premium; this reduces reliance on Chinese processing but raises procurement cost and lock‑in considerations.

Kachin HREE projects (Myanmar) represent outsized supply risk: pre‑coup development claimed ore grades above 5% HREE and potential to be the largest non‑Chinese dysprosium source, but access and output have fallen to zero after January 2026 disruptions. Chinese processors and exporters (Shenghe and border operations) remain pivotal nodes, yet trucking route closures and MOFCOM re‑export controls have cut logistics flows by an estimated half in affected corridors.

China’s GanZhou cluster continues to supply the majority of HREE volume and has moved more elements into an export‑controlled list, lengthening approval times and squeezing just‑in‑time magnet and aero supply chains. New U.S. separation capacity in Fort Worth and planned Australian expansions (Kalgoorlie, Nolans, Eneabba) offer alternative sourcing with higher operating costs and longer ramp timelines.

Operational tradeoffs and supply‑chain impacts

Three tradeoffs dominate current modelling: 1) supply security versus unit cost-U.S./Australian sources provide policy‑backed availability but at reported premium multiples versus Chinese processing; 2) grade versus stability-high‑grade Myanmar/DRC deposits offer material concentration advantages but carry near‑term blackout risk; 3) scale versus approval latency-Chinese refiners provide scale and efficiency but create exposure to licensing delays (30-60 days) and export list changes.

Signals to monitor

- Feb 2026: outcome of the China‑U.S. truce window and any extension of export relief.

- Q3 2026: U.S. midterm political control and continuation of DoW offtake/subsidy programs.

- MOFCOM license processing times and any further expansion of restricted HREE lists.

- Physical restoration of access to Kachin sites and port/trucking corridor reopenings in Myanmar and eastern DRC.

Operational metrics to watch quantitatively where available include facility uptime, reported output (MT/month) from Mountain Pass and Lynas, MOFCOM turnaround days, and any public DoD reserve procurement notices. These metrics will clarify whether onshore capacity offsets the deficit created by coup‑affected projects.

Materials Dispatch Signal

Political shocks in 2026 have converted structural HREE tightness into episodic supply risk. The practical response observed across supply chains is bifurcation: increased allocation to U.S./Allied suppliers with policy backing, and continued tactical dependency on Chinese processing where scale and grade remain unavailable elsewhere. The result is higher complexity in compliance, logistics and inventory planning, with near‑term concentrated risk around Myanmar and DRC access and medium‑term sensitivity to U.S. political continuity and Chinese export policy decisions.