Data Brief

Weekly dispatch #7: licensing backlogs, customs seizures, and court rulings

Executive summary

- Licensing backlogs and regulatory reopenings are reshaping supply timelines: Mexico inherited 176 stalled projects, resolved 110, with 66 remaining; Ecuador reopens a seven-year registry with 3-8% royalties-both actions shift commissioning windows into mid‑2026 and beyond.

- Customs enforcement is intensifying in West Africa, Argentina and transshipment hubs, lengthening lead times and increasing provenance requirements; Mali restructuring followed a 23% drop in industrial gold output in 2025.

- Court rulings and litigation are altering project trajectories: a US judicial outcome affecting Twin Metals alters domestic nickel/copper prospects (500,000+ MT/year potential stated), while remediation and legal challenges delay Grasberg and Red Dog outputs into 2026-2027.

- Immediate risks include 6-18 month sourcing delays, compressed refined availability for battery/defense metals, and heightened customs seizure exposure tied to provenance and permit clarity; signals to watch include permit clearances mid‑2026, customs seizure reports, and appellate timelines.

Legal-administrative developments are materially tightening physical flows of strategic and precious metals ahead of mid‑2026. Licensing backlogs, an uptick in customs seizures and decisive court rulings are converging to create multi‑quarter sourcing delays for nickel, copper, cobalt, lithium, gold and silver, with governance and compliance becoming primary determinants of near‑term availability.

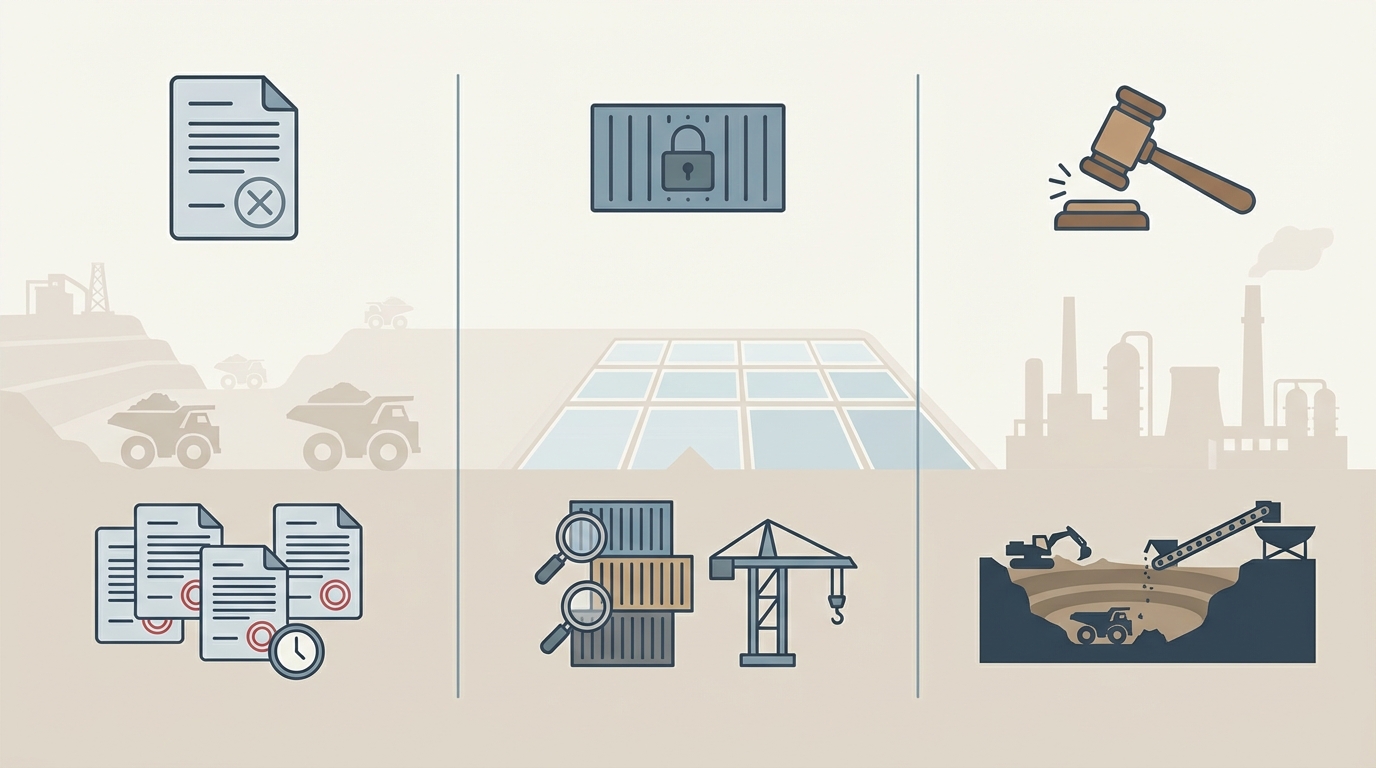

Permitting backlogs: project timing and supply risk

Licensing remains the primary chokepoint for new supply. Mexico’s transition left 176 stalled projects; authorities have resolved 110 via accelerated environmental and water approvals while 66 remain targeted for mid‑2026 clearance, unlocking an estimated US$11 billion pipeline for metallic minerals. Ecuador’s full registry reopening after seven years, together with 3–8% royalties for medium/large metallic operations and stricter tailings/emissions scrutiny, pushes first outputs toward Q3 2026. Canada’s feasibility‑stage critical minerals projects face financing and infrastructure gaps that extend delivery horizons into 2028 for some nickel and cobalt prospects.

Operationally, market analysis shows brownfield and restart pathways gain priority over greenfield developments because they compress lead times; however, interim concentrate shortages are triggering rerouted logistics and elevated freight exposure as processors and smelters chase limited material.

Customs seizures and trade enforcement: provenance as a supply constraint

Enforcement actions are emerging as a de facto supply control. Mali’s institutional restructuring and prior fiscal recoveries correlate with heightened customs scrutiny and seizure activity on gold exports, a dynamic that trimmed industrial gold output in 2025 and extended lead times for West African flows into Europe. Argentina’s brine sector is operating under hyperinflationary cost pressure-reported AISC of $7,223/t LCE-and customs friction has increased transactional risk for lithium concentrates and associated precursors.

In parallel, US agency moves to streamline reviews for deep‑sea nodule activities create mixed signals: faster administrative processing for exploration does not equate to safe import pathways, and gaps between domestic fast‑tracking and International Seabed Authority governance raise seizure or detention risk for unaligned cargoes.

Court rulings: legal outcomes that reshape supply curves

Judicial decisions are reshaping availability by either unlocking or delaying large projects. A US ruling altering prior restrictions on the Duluth Complex (Twin Metals) shifts the domestic nickel/copper narrative with cited development potential above 500,000 MT/year post‑ramp, yet environmental re‑approvals and appeals extend practical restart timelines into 2027. Indonesia’s Grasberg mine and Alaska’s Red Dog operations face court‑mandated remediation and indigenous claims that reduce near‑term copper, zinc and byproduct silver output, keeping secondary supply thin while fixed costs are absorbed over lower production.

Market implications and operational tradeoffs

The intersecting legal signals reframe sourcing tradeoffs for defense, battery and industrial users. Jurisdictions that clear backlogs (Mexico, Ecuador) present nearer‑term supply restoration but carry royalty and compliance layers. Regions with heightened seizure risk (parts of West Africa, complex transshipment hubs) are generating longer lead times and heavier documentation requirements. Deep‑sea nodules and restarts in the Americas are visible hedges in market narratives, though governance mismatches leave legal exposure.

Signals to watch

- Permit clearance progress and water/tailings approvals in Mexico and Ecuador through mid‑2026.

- Customs seizure and provenance enforcement reports from Mali, Argentina and major European ports.

- Court docket updates and appellate timelines for Twin Metals, Grasberg remediation and indigenous land claims affecting Red Dog.

- NOAA and ISA alignment on deep‑sea governance and any port detention cases involving polymetallic cargoes.

Materials Dispatch Signal

Regulatory and judicial processes are now primary drivers of short‑term metal availability. The calendar through mid‑2026 will determine whether supply gaps widen into sustained structural tightness or whether administrative clearances alleviate pressure. Market participants are increasingly treating permit and customs clarity as equivalent to physical tonnage when assessing operational resilience and allocation of processing capacity.