Uncategorized

China’s Gallium Leverage Cycle: How Licensing, Technology Controls, and Tactical Suspensions

Key Takeaways

- China commands roughly 98–99% of primary low-purity gallium production, creating a “by-product trap” for global supply response.

- Since July 2023, Beijing has sequenced licensing, embargoes, technology controls and tactical suspensions to toggle gallium exports on short notice.

- Allied initiatives to develop alternative recovery capacity face economic and technological hurdles absent long-term offtake assurances.

- Procurement, supply-chain and compliance teams must map indirect gallium exposure and plan for rapid policy reversals.

Executive Summary

China’s calibrated export and technology controls on gallium since mid-2023 reveal a deliberate playbook for exerting leverage over Western semiconductor, defense and clean-tech supply chains. Gallium is not scarce geologically—it is a minor by-product of bauxite and zinc refining—but China’s 98–99% share of primary low-purity gallium production and its proprietary extraction technologies empower Beijing to impose sudden restrictions. Even after the November 2025 suspension of the U.S. civilian export ban (extended through late 2026), the regulatory and technology choke points remain in place, posing persistent disruption risks for procurement and strategy teams.

Defining the “By-Product Trap”

The term “by-product trap” captures a structural constraint: non-Chinese producers cannot scale gallium output quickly because gallium is produced incidentally during large-scale aluminum and zinc operations. Re-establishing recovery circuits typically requires multi-year investments, qualified permitting, and process validation—meaning volumes cannot be toggled at the speed that policy can be toggled. In practice, this creates a reflexive market dynamic: when restrictions tighten, buyers face not only availability risk, but also the prospect that higher prices may be temporary if Chinese supply temporarily re-accelerates later, suppressing incentives to build outside capacity.

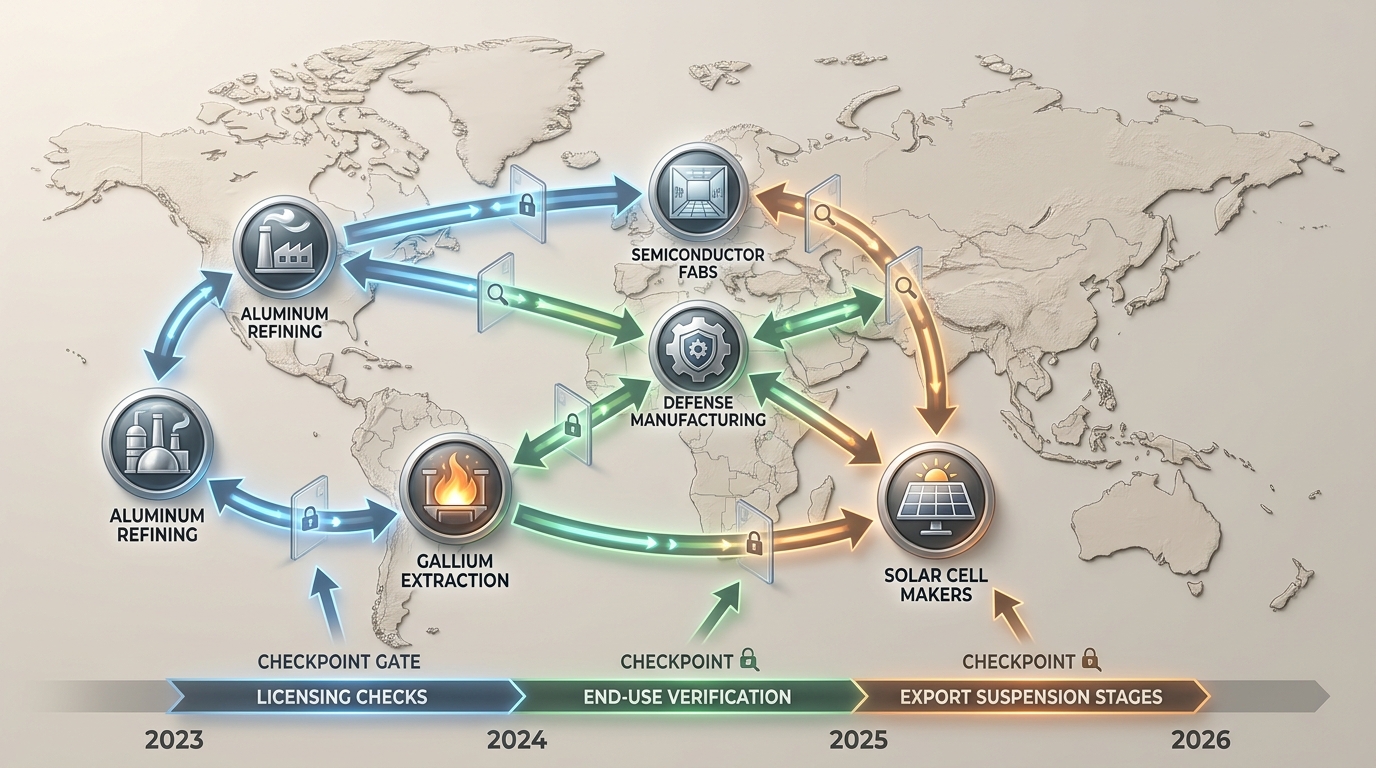

Export Control Timeline

- July 2023: MOFCOM introduces licensing requirements for gallium and germanium exports, quickly reshaping pricing and export flows as end-use scrutiny tightens.

- December 2024: Announcement No. 46 enacts a de facto embargo on U.S. gallium imports, halting civilian shipments and tightening the effective boundary for military end-use.

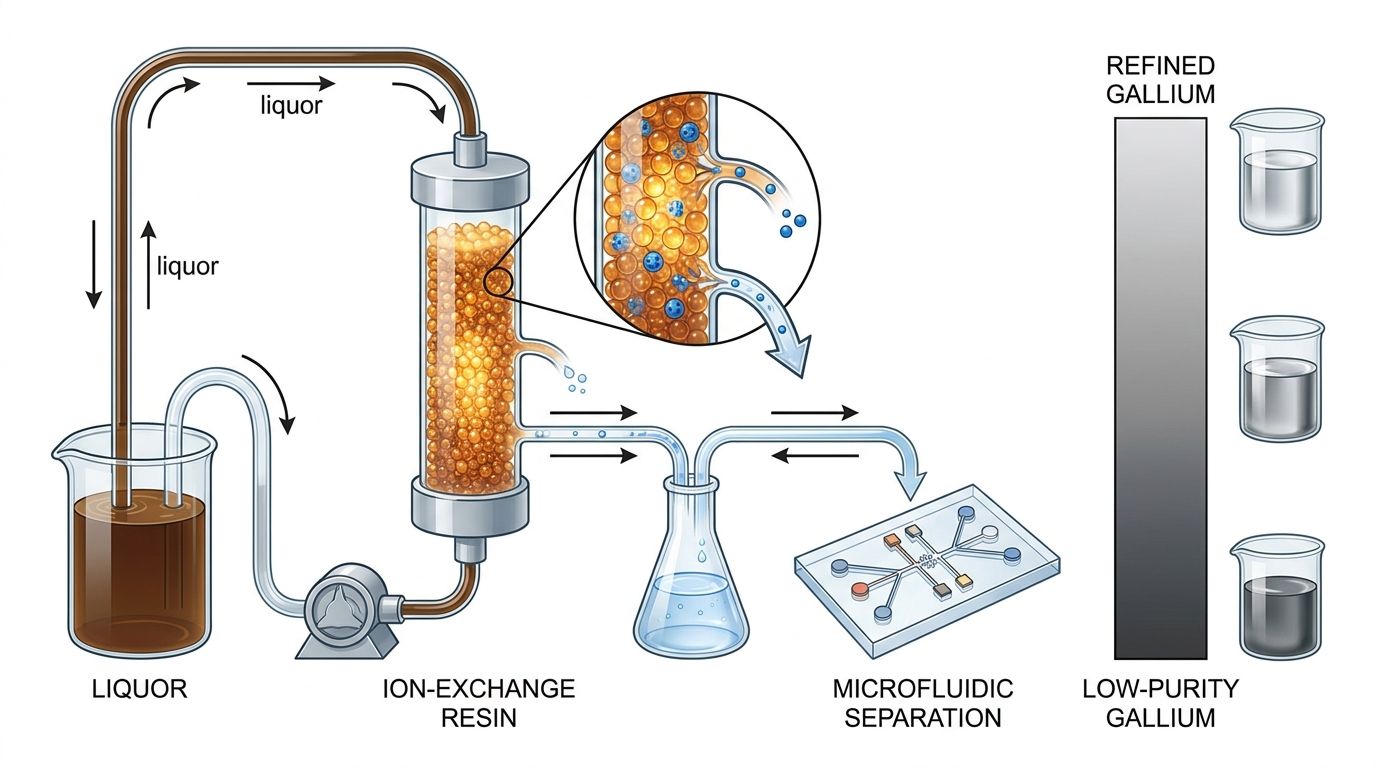

- January–May 2025: Technology controls on extraction processes—specifically purification approaches that rely on ion-exchange and resin methodologies—alongside coordinated anti-smuggling enforcement deepen China’s chokehold on both volumes and know-how.

- November 2025: Announcement No. 72 suspends the civilian embargo until late 2026 but preserves licensing authority, military restrictions and technology controls for rapid re-implementation.

Market and Price Dynamics

Gallium prices have behaved like a policy indicator rather than a pure supply-demand equilibrium. When licensing and enforcement tighten, buyers experience both immediate transactional friction (longer lead times, narrower sourcing channels, compliance overhead) and forward-looking uncertainty about whether volumes will be available in subsequent quarters. That uncertainty tends to flow through contracts, inventory strategies and safety-stock policies—raising effective demand even when end-user consumption has not changed.

USGS-based scenario analysis estimates that a sustained gallium and germanium cut-off could cost the U.S. economy $3.4 billion in GDP, with semiconductors bearing about half the impact. The key procurement implication is not merely “what happens if supply disappears,” but how quickly downstream plans can absorb upstream volatility when specifications, qualification testing and replacement approvals introduce friction.

For market participants, the most important nuance is that gallium’s by-product origin means that alternative supply is not elastic. Even where material exists in scrap or industrial streams, converting it into usable gallium requires recovery pathways and quality certification—so short-term price signals do not automatically translate into rapid, fungible supply.

Fragmented Coverage and Strategic Blind Spots

Specialist commodity analysts and policy think tanks meticulously track gallium export measures, production quotas and price effects. Mainstream tech and gaming-oriented outlets, however, often focus on downstream semiconductor shortages—GPUs, AI chips and lithography capacity—without naming gallium as an upstream bottleneck. This siloed coverage risks underestimating how quickly a “hardware story” can become a “critical minerals story” when Beijing activates its regulatory switch.

For institutional stakeholders, the practical problem is measurement: if gallium exposure is not mapped by end-application, then policy moves can be misread as isolated input disruptions rather than as repeatable sovereign-risk events. In turn, that misreading delays mitigation—such as qualification of alternative feedstocks, redesign of procurement specifications, and compliance controls that prevent sourcing from becoming a legal and operational liability.

Allied Responses and Alternative Supply Efforts

Governments and firms in the U.S., EU, Japan, South Korea and Australia have launched feasibility work aimed at recovering gallium from bauxite, zinc and industrial scrap. European refiners and industrial groups have explored recovery pathways, while Japanese and Korean players emphasize closed-loop recycling strategies to reduce reliance on fresh primary feedstock. Australia’s bauxite-linked pathways have also been examined, though many efforts remain constrained by pilot-stage scale-up and commercialization risk.

Across these initiatives, two challenges recur. First, by-product recovery is capital intensive: it requires additional processing steps, quality control and integration into existing refinery or waste-treatment workflows. Second, absent credible protection against future Chinese market surges, investment returns can remain uncertain—especially if policy can be tightened or relaxed faster than alternative capacity can qualify and deliver on consistent specifications.

Implications for Industry Stakeholders

Procurement and Category Management

- Map direct and indirect gallium exposure. Treat gallium as a cross-cutting input across RF and power electronics, LEDs/optics, and PV-linked bills of materials—then document where qualification and substitution are realistic versus where they are not.

- Scrutinize provenance, not just geography. Move beyond “country of last transformation” labels. For by-product metals, feedstock integrity and process history materially affect compliance posture and technical acceptance.

- Negotiate inventory buffers and contractual resilience. Build flexible delivery terms, and add contingency clauses that explicitly address export control events and compliance-driven shipment holds.

- Plan for recycled gallium as a structured supply lever. Integrate recycling streams from scrap and end-of-life devices where possible, and treat recovery yield variability as a managed risk rather than an assumption of steady-state output.

Supply-Chain Strategy and Operations

- Scenario-plan for rapid policy toggles. Treat licensing changes, enforcement campaigns and temporary suspensions as repeatable scenarios. Then assess the downstream ripple effects on production schedules and inventory consumption rates.

- Engage early with recovery projects, but anchor risk allocation. Use consortia or anchor offtake discussions to clarify who bears commercialization, yield and compliance certification risk.

- Coordinate with R&D on material substitutes where technically viable. Substitute materials—such as silicon carbide in power electronics contexts—should be evaluated as qualification programs, not as instantaneous substitutes.

- Embed regulatory monitoring into S&OP cycles. Incorporate signal monitoring across MOFCOM-linked developments and Western critical minerals/export control frameworks so forecasting assumptions are updated before procurement commitments become irreversible.

Trading Desks and Risk Management

- Anticipate policy-driven volatility. Calibrate hedging logic to scenario distributions shaped by regulatory timing, not only by observed spot price behavior.

- Monitor basis risk across venues. Track differences between Chinese domestic pricing signals, Rotterdam-linked market references, and end-user procurement pricing to avoid assuming uniform pass-through.

- Avoid overestimating “normalization” from downstream announcements. Materials constraints—especially for by-product metals—can remain binding even when consumer-facing production schedules appear stable.

Compliance and Legal Considerations

- Operate under dual-jurisdiction risk. Track both Chinese export control lists and Western critical minerals frameworks to prevent misalignment between sourcing decisions and compliance obligations.

- Strengthen due diligence on intermediaries. Enhanced screening is essential for intermediaries and re-export hubs, given the elevated risk of illicit diversion pathways during policy tightening.

- Prepare for evolving “trusted source” expectations. Expect procurement systems to increasingly favor documentation-intensive sourcing, especially where end-use verification and process provenance become gating factors.

Conclusion

China’s gallium playbook demonstrates how targeted export and technology controls on a by-product metal can deliver outsized leverage over critical supply chains. The November 2025 civilian suspension does not remove the underlying choke points; it only changes the timing and the conditions under which restrictions may be activated. Decision-makers should treat gallium as an enduring vulnerability—using this window to diversify sourcing, reinforce recycling, and institutionalize policy-risk scenarios into strategic planning.