Uncategorized

Materials Dispatch Intelligence: ESG and Community Risk Are Redrawing Supply Reliability for Rare

Due Diligence Review: ESG and Community‑Risk Red Flags in Strategic Mineral Projects

We reviewed a cross‑section of 15 strategic mineral projects—covering rare earths, lithium, nickel, cobalt and platinum‑group metals (PGMs)—to assess how environmental, social and governance (ESG) issues and community disputes are affecting operational continuity and upstream supply availability. Our work draws on site and virtual audits, regulatory filings, local media monitoring and direct qualification discussions with operators and downstream offtakers.

Key Takeaways

- ESG and community disputes consistently convert into hard operational events: delayed expansions, frozen tailings projects, and halted water licences, which in turn shorten effective supply.

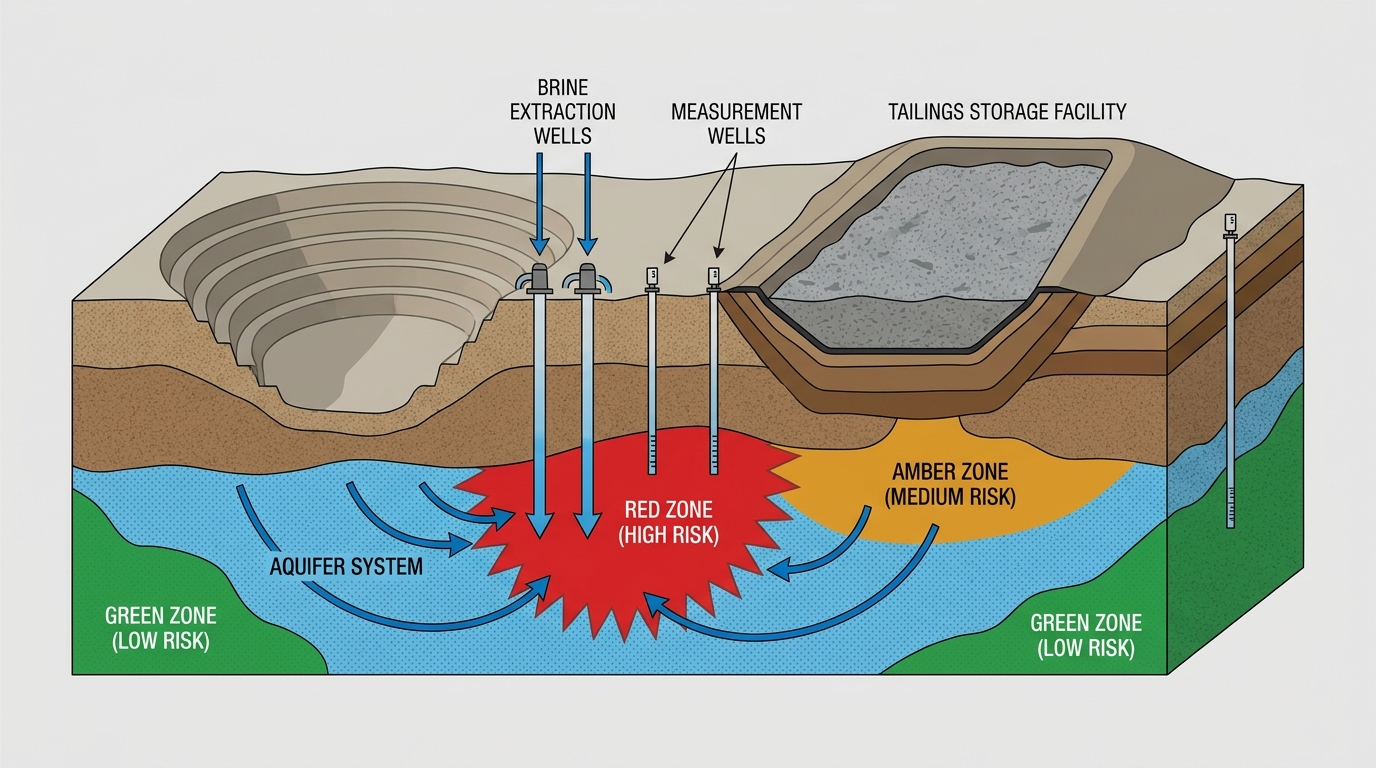

- Water and tailings management are the dominant technical flashpoints across jurisdictions; projects with independently verified systems show materially less disruption.

- Indigenous and local equity participation tends to channel conflict into negotiation rather than obstruction; absence of meaningful sharing correlates with escalations.

- Governance fragility and sanctions amplify local incidents into national policy responses that can materially reduce available tonnage to ESG‑sensitive offtakers.

Analytical Lens: How ESG and Community Risk Becomes an Operational Event

The principal lesson from the dataset is straightforward: ESG disagreements rarely remain within public affairs teams. They become path‑critical operational events—delayed shaft sinking, frozen concentrator upgrades, revoked water or tailings permits—that sit on the same schedule drivers as geotechnical failures or metallurgical setbacks.

Across the portfolio four structural channels dominate:

- Water and tailings exposure – Community concern about groundwater drawdown and tailings storage repeatedly triggers regulatory pauses. Projects adhering to international standards such as the Global Industry Standard on Tailings Management (GISTM) and with transparent monitoring experience shorter interruptions.

- Indigenous and community consent – First Nations and Indigenous groups are asserting leverage through court actions, blockades and renegotiation of impact‑benefit agreements; this operates as an ongoing critical path risk rather than a single permitting hurdle.

- Climate and natural‑hazard sensitivity – More frequent heatwaves, cyclones and permafrost thaw interact with legacy infrastructure and tailings designs to create recurring outage patterns.

- Governance and sanction fragility – In jurisdictions with sanction or export‑control exposure, ESG findings are rapidly entangled with national policy, export quotas (government limits on the volume or value of goods allowed to leave a country) and external audits, increasing the probability of supply disruptions.

- Power and infrastructure reliability – Opposition to new transmission lines or access roads compounds logistical fragility, producing bottlenecks that amplify delivery variance.

From a supply‑chain perspective, this collapses into a few operational questions: Will a water license or tailings permit hold through expansion? Is social licence resilient to a geotechnical setback? Are sanction and reputational risks acceptable for downstream OEMs with internal ESG screens?

Case Focus: Rare Earth and Lithium Supply in the United States

Two US projects in the dataset—Mountain Pass (California) and Thacker Pass (Nevada)—illustrate how ESG dynamics can shape strategic mineral reliability even in jurisdictions perceived as stable. Together they underpin a sizeable share of planned non‑Chinese NdPr (neodymium‑praseodymium) magnet feedstock and lithium carbonate for batteries. Note: we use TREO to refer to total rare earth oxides and LCE to refer to lithium carbonate equivalent, terms which appear below when discussing volumes and sourcing.

Mountain Pass: Legacy Environmental Liabilities Meet New Supply Imperatives

Mountain Pass remains a cornerstone of non‑Chinese rare earth oxide (TREO) production. Our dataset characterises current production near 40,000 tonnes per year of rare earth oxides, with medium‑term plans toward ~60,000 tpa. The project sits at an uncomfortable intersection of legacy liability and strategic indispensability.

Critical findings with direct continuity implications:

- Water stress in a sensitive basin – Legal action by local tribes over groundwater extraction has previously interrupted expansion permitting for more than a year, placing debottlenecking plans in limbo.

- Tailings seepage and regulatory fines – Historic seepage concerns have attracted significant penalties and made hydrological audits de facto gatekeepers for license renewal and expansion approvals.

- Incomplete water recycling implementation – Management proposals for closed‑loop water circuits have not yet achieved full capture; tightening extraction limits could quickly constrain throughput.

- Climate exposure – Heatwaves that curtail open‑pit operations create short‑term production swings that ripple through just‑in‑time magnet supply chains.

For market planners, Mountain Pass demonstrates that a single ESG incident can trigger policy debates at state and federal levels, elevating supply risk beyond the local operating horizon. When substitutes at comparable scale are scarce, even a modest output shortfall materially tightens upstream availability for magnet manufacturers and defense users.

Thacker Pass: Social Licence on the Critical Path for US Lithium Supply

Thacker Pass, envisaged to produce around 40,000 tpa LCE, has become a test case of how community opposition can extend timelines in OECD settings. Internal tracking showed slippage in first‑production guidance—driven mainly by permitting pauses rather than technical redesigns.

Core risk elements:

- Indigenous rights and sacred sites – Litigation by Paiute‑Shoshone groups over cultural heritage paused key Bureau of Land Management processes and disrupted construction sequencing.

- Water use in an arid catchment – Hydrogeological assumptions about aquifer recharge have been challenged by local stakeholders, framing water competition as central to the dispute.

- Ore and process complexity – Clay‑hosted lithium raises ongoing questions about grade consistency and impurity management; perceptions of under‑reported waste volumes have reinforced community scepticism.

- National policy overlay – The project’s prominence in industrial policy and incentive frameworks has elevated local disputes to national‑level debate, slowing negotiated compromise.

Operationally, Thacker Pass underscores a risk inflection point common to long‑life projects in contested landscapes: social licence operates continuously. Downstream cathode and cell manufacturers have moved from a single “on‑time” sourcing case to a suite of scenarios—on‑time, slow‑ramp, stalled—each with different implications for blending strategies and compliance with domestic content rules.

High‑Risk Jurisdictions: Cobalt, Nickel and the ESG–Governance Nexus

Projects in the Democratic Republic of Congo (DRC), Papua New Guinea (PNG), Russia and Cuba illustrate a different dynamic: community incidents intersect with governance fragility and geopolitical stress to produce layered continuity risk.

Examples from the portfolio:

- DRC copper–cobalt complexes – Interfaces with artisanal mining, resettlement disputes and river contamination led to logistical frictions—blocked roads, temporary export holds and curfews—that compressed effective deliveries even when nameplate figures looked intact.

- PNG Ramu nickel–cobalt – Deep‑sea tailings placement and reported pipeline ruptures mobilised community blockades and government reassessments, turning single incidents into multi‑month access constraints exacerbated by cyclone exposure.

- Russian Arctic operations – Chronic emissions and spills have prompted Indigenous protests and international scrutiny; when coupled with sanctions, these incidents restrict access to Western technology and financing, affecting maintenance and upgrade schedules.

- Cuban nickel projects – Hurricanes and embargo‑related equipment constraints have combined to raise the operational and reputational cost of continued output in that jurisdiction.

Across these contexts, disruptions rarely manifest as permanent shutdowns. More commonly they increase delivery variance and raise compliance risk for ESG‑aware offtakers, who often reduce reliance on assets that migrate onto internal watch lists.

Patterns and Monitoring Signals Across the Portfolio

Five recurring patterns matter for supply‑chain planning:

- Water and tailings as primary flashpoints – Transparent, GISTM‑aligned designs and third‑party audits reduce disruption severity.

- Indigenous/local equity participation – Shared‑value models convert conflict into negotiation more often than obstruction.

- Climate impacts folded into community narratives – More frequent extremes increase scrutiny of “design storm” assumptions.

- Governance risk amplifies incidents – Weak institutions can translate local disputes into license suspensions or royalty overhauls.

- Downstream ESG screening as a demand‑side shock – Once a project is flagged for human‑rights or tailings failures, offtakers may diversify even while the mine remains operational.

Useful monitoring signals include: the tone and frequency of regulator communications; the presence of revenue‑sharing or equity structures with host communities; timing of tailings expansion or dam redesigns; renewal windows for water and emissions licences; and whether incidents become national political issues or remain local and resolvable.

Risk Inflection Points

Particular inflection points warrant close attention because they often trigger upstream re‑evaluations:

- Transition phases for tailings capacity or tailings‑design changes.

- Renewal or amendment periods for key water and emissions licences.

- Revisions to Indigenous impact‑benefit agreements.

- High‑profile environmental incidents that attract national media.

- National elections or regulatory overhauls that reframe resource sovereignty debates.

Conclusion

Our review concludes that ESG and community factors are now core supply‑chain variables for strategic minerals. Projects that pair credible, independently verified tailings and water management with transparent benefit‑sharing and contingency planning demonstrate materially greater resilience. For market participants, durable access to critical feedstocks increasingly requires understanding both the geology and the governance surrounding production.